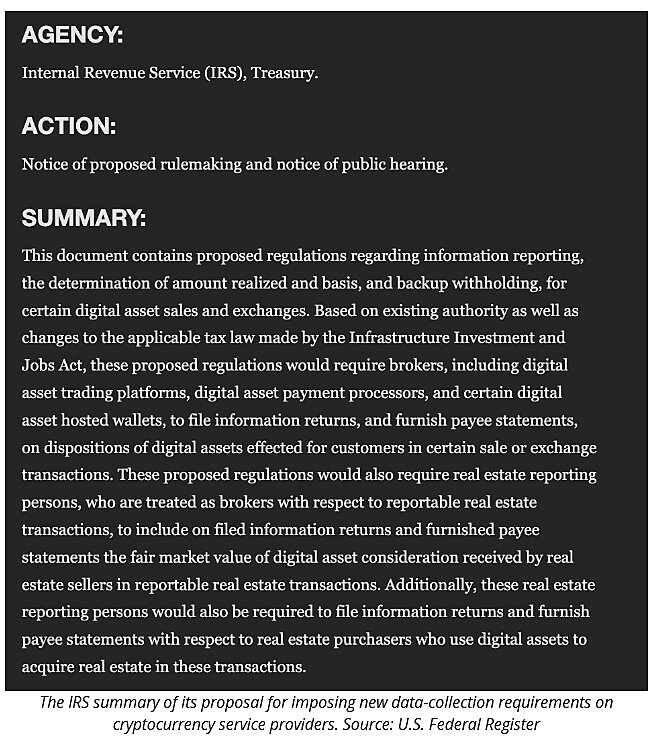

For two years, the cryptocurrency world has been waiting to see how the Internal Revenue Service (IRS) would implement the Infrastructure Investment and Jobs Act. Put simply, this law established new reporting requirements that risked setting a de facto ban on cryptocurrency mining and exposing millions of Americans to new felony crimes. The good news is that the IRS’s nearly 300-page proposal is not quite as bad as it could have been under the law. However, that is far from saying it is good policy.

As citizens, companies, and consultants finish crafting their comment letters ahead of the October 30 response deadline, it’s important to take a step back and recognize why businesses should not be required to report customers to the government by default.

Recalling back to 2021, the Infrastructure Investment and Jobs Act was about building roads, bridges, and the like — it was not about cryptocurrency or financial reporting. It wasn’t until funding was desperately needed to offset spending that members of Congress slipped in two provisions to increase financial surveillance over cryptocurrency users. Their argument was that increasing surveillance would increase tax revenue, effectively accusing cryptocurrency users of tax evasion.

At the time, the Joint Committee on Taxation estimated that the provisions would yield around $28 billion in tax revenue over 10 years. Without a way to replace the funding, attempts to remove the controversial reporting requirements were ultimately rejected.

The $28 billion figure was questionable at the time. And less than a year later, the Biden administration released its budget, which contained a vastly different estimate. In contrast to the $28 billion estimated by the Joint Committee on Taxation, the Biden administration estimated that only $2 billion would be received over the next 10 years. And now, even that number might be an overestimation as Treasury officials acknowledged that the estimates were based on a very different market.

With cost-offsetting out the window, what is left appears to be little more than another brick in the wall of U.S. financial surveillance.

The IRS’s proposal, again, doesn’t seem as bad as it could have been since the proposal does exclude miners and some software developers for now. Still, the proposal chooses a concerning path for deciding who should be required to report customers.

The premise seems to be partly based on “whether a person is in a position to know information about the identity of a customer, rather than whether a person ordinarily would know such information.” The proposal states that this distinction is made because some platforms “have a policy of not requesting customer information or requesting only limited information [but] have the ability to obtain information about their customers by updating their protocols.” For this reason, the proposal states that the IRS expects some decentralized exchanges and selfhosted wallets may be forced to report their customers’ private information.

The IRS reports 1,726 comments received so far.

— CryptoTaxGuy.ETH ⌐◨-◨ 🦇🔊🛡️ (@CryptoTaxGuyETH) October 17, 2023

Those are rookie numbers.

Unless you want:

- Every crypto site and wallet to have your SSN, and

- Nodes, devs, governance, & LPs to be brokers in technical noncompliance,

Take 2 mins to use @LeXpunK_Army ‘s comment tool NOW https://t.co/USYAHKdxic pic.twitter.com/1d8ijWbjVG

🚨RAID ALERT🚨

— LeXpunK_Army (@LeXpunK_Army) October 14, 2023

LeXpunK Army troops are hereby MOBILIZED to OPPOSE the IRS’s new draconian anti-crypto tax rules

Make your voice heard by sending your complaints to the IRS through our convenient AI-powered drafting tool: https://t.co/evZk08EyWO pic.twitter.com/lRdEvDJrCT

Yet rather than continue to expand the range and depth of financial surveillance, now should be the time to question the premise as a whole. In a country where Americans are supposed to be protected by the Fourth Amendment, businesses should not be forced to report their customers to the government by default. Activities like using cryptocurrency for payments, receiving over $600 on PayPal after a garage sale, or getting a paycheck from a job should not put you on a government database.

Steering away from this surveillance status quo might require fundamental changes to U.S. law, but that’s not to say doing so is a radical idea. When surveyed by the Cato Institute, 79 percent of Americans said that it is unreasonable for banks to share financial information with the government and 83 percent said that the government should need a warrant to obtain financial information.

It is those principles that should guide the discussion forward. So, while the October 30 response deadline is just around the corner, commenters should weigh both what the proposal does and doesn’t say.

Furthermore, although the present focus is very much on the IRS, let’s not forget that the responsibility to fix both the current situation and the larger financial surveillance status quo lies in the halls of Congress. At the end of the day, the IRS is doing what Congress told it to do. So, it’s Congress that needs to step in to reform the system as a whole.

About the Author