Congress should

-

reverse wide-scale loan forgiveness;

-

end the singular focus on for-profit colleges for censure;

-

reject proposals to incentivize more state spending on colleges; and

-

ultimately phase out student aid programs, including grants, loans, and tax incentives.

There is a tendency to think that education is good, so more must be better. But decades of huge federal spending on higher education, driven by this simplistic conviction, have produced numerous outcomes that are anything but good. This chapter explores these harmful effects, which deliver an unmistakable lesson when coupled with the Tenth Amendment dictum that “the powers not delegated to the United States by the Constitution … are reserved to the States respectively, or to the people”: Washington should withdraw from higher education.

Student Debt and Financial Aid

The Great Recession of 2008 and 2009 brought with it a new focus on student debt and the price of college, issues made especially visible by three things: (1) in 2010, total student loan debt surpassed total credit card debt for the first time; (2) the 2011 Occupy Wall Street protests focused to a significant extent on college costs; and (3) in 2012, total student debt broke the psychologically huge $1 trillion mark. The COVID-19 pandemic brought additional attention, with a freeze on debt repayment instituted soon after the pandemic struck that was maintained for nearly three years and a push by progressive lawmakers to forgive tens-of-thousands of dollars for a wide swath of borrowers, which President Joseph Biden instituted by executive action in August 2022.

This attention came after significant expansions and reforms of student aid. For several decades, the federal government has been the primary provider of aid to students, through grants, loans, work study, and tax incentives for higher education expenditures. Since 2007, that role has grown significantly. The Bush and Obama administrations and Congress raised the maximum Pell Grant and expanded the percentage of students eligible for it; increased the maximum amounts available through loans; offered loan forgiveness for people who work for government or eligible nonprofit entities; introduced income-based repayment that caps payments at 10 or 15 percent of adjusted gross income and forgives remaining debt after 20 or 25 years; and cut interest rates on student loans.

Washington also changed loan financing, eliminating the “guaranteed” program in which borrowers obtained loans from ostensibly private lenders, but the federal government essentially guaranteed lenders a profit with the backing of federal dollars. That was replaced with lending directly from the federal treasury.

Federal Aid: Seems Good, Is Bad

The first major negative effect of federal intervention, in particular student aid, has been rampant price inflation. It was not hard to anticipate: In 1987, Secretary of Education William Bennett famously surmised that federal aid was encouraging tuition inflation. In a New York Times op-ed titled “Our Greedy Colleges,” he wrote that “federal student aid policies do not cause college price inflation, but there is little doubt that they help make it possible.” Essentially, when we give people money to pay for something, we incentivize providers to raise their prices.

Colleges are revenue maximizers, and they are always thinking of things they could do with more money: start new programs, pay employees more, avoid cost-saving changes such as eliminating underused programs, or build new fitness facilities or even water parks. Even economists Robert Archibald and David Feldman, who largely disagree with the “Bennett Hypothesis,” tacitly concede this in their book Why Does College Cost So Much? They argue that anything that might constrain colleges would at least appear to compromise “quality,” which they seem to define as supplying everything someone might say is good, including small classes, “research or public service,” and limited adjunct professors.

Top Five College Water Parks

- University of Missouri “Tiger Grotto”: According to the Mizzou website, “The Grotto will transform your dullest day into a vacation, with our resort quality facilities and atmosphere that will unwind you, even with the most stressful of schedules. The Grotto features a zero-depth pool entry with a high-powered vortex, lazy river and waterfall. Our hot tub, sauna and steam room will help you loosen up after a hard workout.”

- Texas Tech “Student Leisure Pool”: According to Texas Tech’s website, this is “the largest leisure pool on a college campus in the United States.” It features, among other things, a 645-foot-long lazy river and a 25-person hot tub.

- University of Alabama: According to the school’s “University Recreation” webpage, the outdoor pool facility features a “current channel,” “spray features,” a “tanning shelf,” a “water slide,” and a “bubble bench.”

- Missouri State: The school’s pool features LED lights that change color at night, a 16-seat spa and sauna near the pool, and a 20-yard zipline.

- Louisiana State University: The aquatics facility features a 536-foot lighted lazy river in the shape of “LSU,” two “bubbler lounges,” and a 21,000-square-foot sun deck made of “broom finished concrete with sand blasted etching of tiger stripes.”

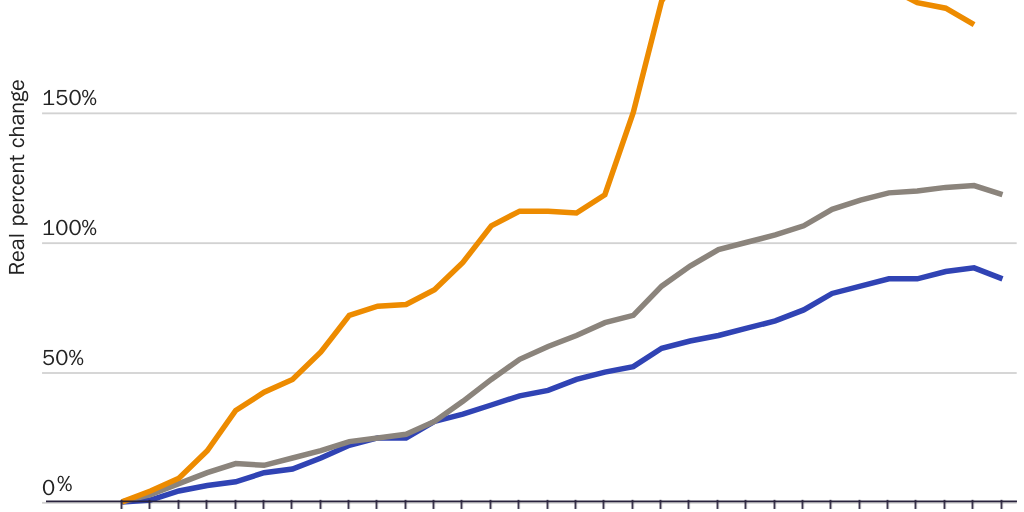

Figure 1 illustrates that for the past three decades, inflation-adjusted aid per full-time-equivalent student has tended to increase at a remarkable rate, more than tripling by 2010–2011. That increase almost certainly provided the fuel for the more than doubling of inflation-adjusted tuition, fees, and room and board charges at public four-year institutions and the roughly 90 percent increase in prices at four-year private schools. Of course, aid is not the only factor in college pricing. Skeptics of the Bennett Hypothesis often blame cuts in state and local subsidies to colleges as the primary culprit behind rising prices. But those cuts do not meaningfully affect private institutions, which receive little such subsidization. Plus, public institutions have seen an increase in total state and local funding since 1990. Where there has been an appreciable reduction is on a per-pupil basis, but that is primarily a consequence not of tight-fisted states but of enrollment increases—from 7.8 million to 10.6 million full-time-equivalent students between 1990 and 2021.

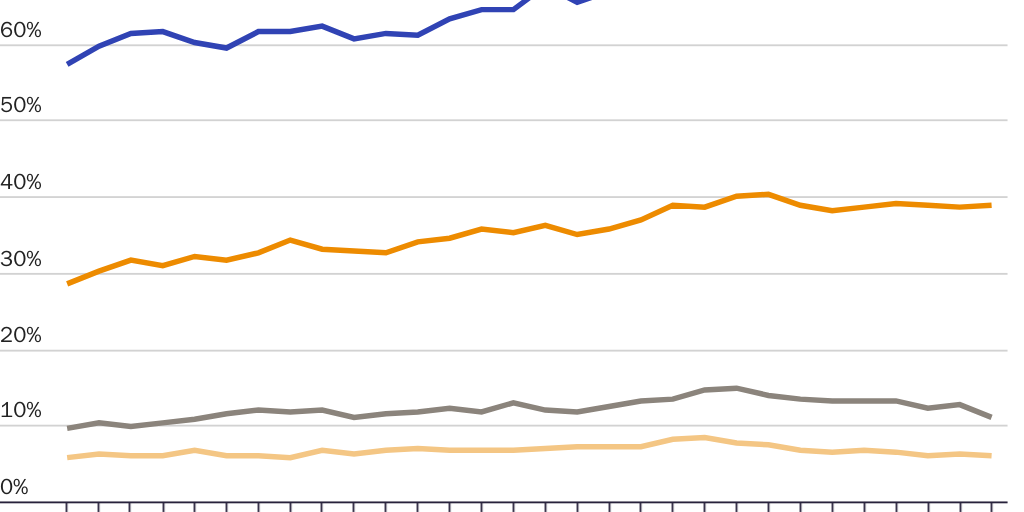

As problematic as subsidizing students is, a welcome consequence of higher education being structured more like a free market than K–12 education—attendance is not compulsory and subsidies are much more attached to students—is that the system can somewhat self-correct. With sticker prices hitting sometimes astronomical levels and debt rising, fewer people have been attending college and are using less aid. As Figure 1 shows, aid per full-time-equivalent undergraduates starts decreasing after peaking during the 2009–2010 academic year. Similarly, total enrollment in postsecondary education dropped from 20.3 million in 2009 to 19 million in 2020, and the share of people ages 18 to 34 overall and for several subgroups (Figure 2) dropped between roughly 2011 and 2019.

While in the past it was necessary to make a detailed case that student aid fuels rampant price inflation, it no longer is. It seems to be well accepted. Unfortunately, instead of focusing on fixing the problem by reducing aid, some prominent policymakers and activists have keyed in on treating a symptom: debt—specifically, forgiveness of debt in the range of $10,000 to $50,000 per debtor, often without regard to a borrower’s income.

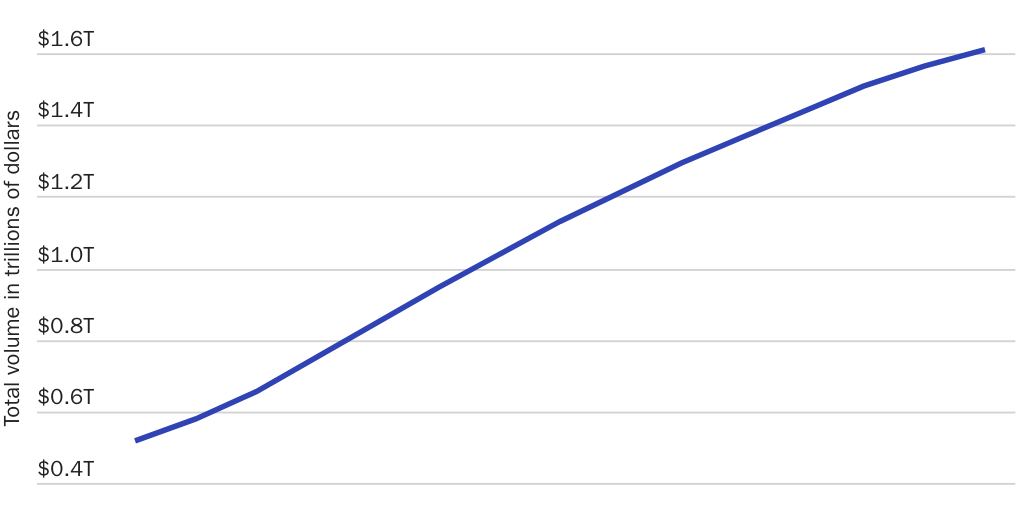

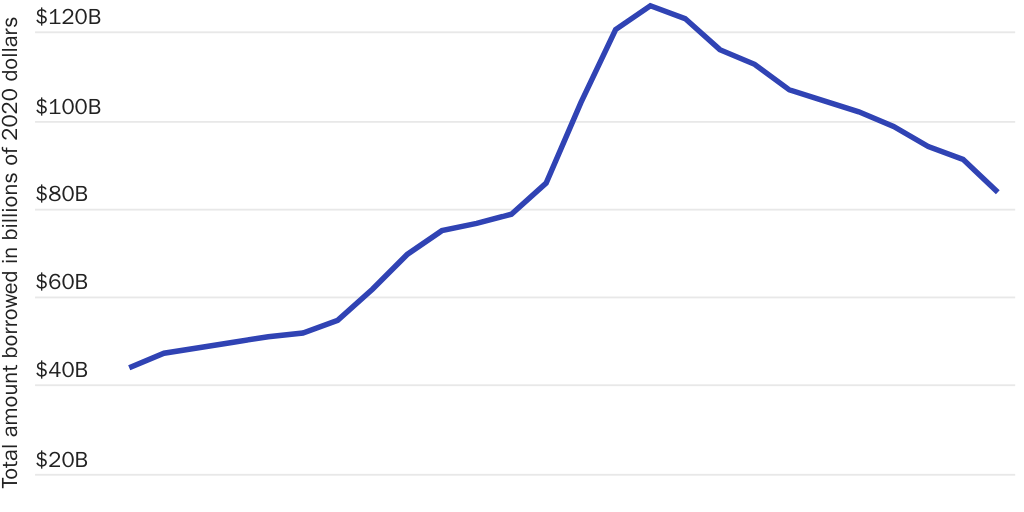

The debt situation does look scary, especially in the aggregate. As Figure 3 shows, total federal student debt rose from about $516 billion in 2007 to $1.6 trillion in 2021. But again, people seem to be wising up. As seen in Figure 4, the total amount of debt taken on each year rose until 2011 but then plunged, again as people reevaluated going to college and how much to spend.

It appears that the debt situation may indeed be correcting itself; although debt levels rose substantially, most federal borrowers owe less than $20,000. Finally, while prices are artificially high, the payoff for a bachelor’s degree is around $1 million more in earnings over one’s lifetime than just having a high school diploma. A graduate degree confers from $1.6 million to $3.1 million more, depending on the type of degree. For degree completers, debt is not only manageable but is a wise investment.

Given the big college payoff, there is no justification for mass student debt cancellation. Taxpayers should be repaid. Unfortunately, after several years of prodding by progressive activists and politicians such as Senators Elizabeth Warren (D‑MA) and Chuck Schumer (D‑NY), President Biden declared that the U.S. Department of Education would cancel $10,000 of student debt for any federal borrower with an income less than $125,000 individually, or in a household with an income below $250,000. He also promised to cancel up to $20,000 for any Pell Grant recipient with federal student debt, subject to the same income caps. The caps include all but essentially the top five percent of earners, and estimates put the cost of the cancellation in the $400 billion range. Also, the executive action clearly violates the constitutional separation of powers, which gives Congress the power of the purse.

Again, the solution is to reduce federal student aid, not cancel repayment.

But is not reducing consumption of higher education—which would presumably come with large aid cuts—a bad thing? Should we not want greater human capital even if there are some negative effects of producing it?

This is an understandable position, but funding something called “education” does not mean that we are getting more learning—or learning in areas of need.

First, about a third of all students who enter college, frequently enabled by aid, never finish, often because they are unprepared for college-level work. Thus, they have debt but no degree with which to greatly increase their earnings and repay what they owe. Indeed, small debtors compose the biggest chunk of loan defaulters, whereas students with heftier debt levels have often gotten undergraduate and graduate degrees. In 2015, researchers found that 34 percent of those who borrowed between $1,000 and $5,000 had defaulted on repayment, versus only 18 percent who borrowed more than $100,000.

That said, many who finish college have difficulty finding work requiring their degree. According to the Federal Reserve Bank of New York, approximately one out of every three bachelor’s degree holders is in a job not requiring the credential. Meanwhile, the surfeit of degree holders is leading to “credential inflation.” According to the human resources firm Burning Glass Technologies and Harvard Business School, many job advertisements call for a degree even though the people currently occupying those positions typically do not have one, and the desired skills are not college level. For instance, researchers found 67 percent of postings for supervisors of production workers calling for a bachelor’s degree but only 16 percent of current occupants possessing one. Finally, while the wage premium for a degree is large, earnings for people with at least an undergraduate credential dropped between 2000 and 2019.

What about learning?

We do not have great measures of learning, but the National Assessment of Adult Literacy revealed that in 1992, about 40 percent of adults whose highest degree was a bachelor’s were proficient in reading prose, but by 2003—the only other year the assessment was administered—only 31 percent were proficient. Among people with advanced degrees, prose proficiency dropped from 51 percent to 41 percent. More recently, the Program for the International Assessment of Adult Competencies found in 2012 and 2014 that U.S. households with members ages 16 to 65 had 68 percent of people with more than a high school education score in the third literacy level or above. In 2017, only 64 percent did. In numeracy, the drop was 57 to 53 percent.

This outcome is consistent with something that has been observed for many decades: college students are spending less time on academics. Authors Richard Arum and Josipa Roksa have noted that college students reported spending 40 hours per week on academic pursuits in the early 1960s but only 27 hours in 2011. Time spent studying declined from 25 hours per week in 1961 to 20 hours in 1980 and 13 hours in 2003.

The U.S. System: Don’t Make It Worse

As problematic as American higher education is, it works much better than either our elementary and secondary systems or most other countries’ postsecondary systems. American universities dominate world rankings; the United States is the top destination for students pursuing studies outside their home countries; and we have by far the greatest number of top scholars, including Nobel Prize winners. Why? Because as wasteful and distorting as student aid is, it is much better to attach money to students and give institutions autonomy than to have the government operate schools and fund them directly. We want a system that can supply diverse education and that allows students and schools to respond quickly to changing needs.

Of course, American higher education is far from perfect in that regard. Public colleges and universities receive heavy direct subsidies from state and local governments that render them significantly insulated from the pressures of student demands. And private, nonprofit schools often have big endowments or other sources of funds accumulated through tax-favored donations. For-profit colleges and, to a lesser extent, community colleges have often been more responsive to changing workforce demands.

That tells us, first, that Congress should not enact legislation that would offer federal funding to states in exchange for greatly increased subsidies to public colleges and lower or zero tuition, as has been proposed. Such legislation would reduce sticker prices and debt but would also render higher education even less efficient than the current system while ballooning the taxpayer burden.

Second, Congress should reverse widespread loan forgiveness if it survives court challenges. Mass cancellation would encourage much more borrowing in the future and enable even worse price inflation, with potential borrowers assuming that their loans would eventually be forgiven. It should also do this because President Biden’s executive action is an egregious breach of the separation of powers.

Third, Congress should not singularly focus punishments for poor outcomes on for-profit institutions. Students who attend for-profit schools tend to have relatively high loan default levels and tend not to earn as much as graduates of four-year public schools and private, nonprofit schools. But for-profits work with students with the greatest challenges—older, poorer, more likely to have families and full-time jobs—even compared with community colleges. Meanwhile, for-profits tend to be relatively quick to expand or create new programs when demand for specific skills arises and to scale down or end programs when demand subsides. Of course, they tend to try to maximize their revenue, but that makes them no different from putatively not-for-profit colleges. Any punishments for poor performance should apply equally to schools regardless of tax status.

Removing the Federal Government from Higher Education

James Madison wrote in Federalist no. 45, “The powers delegated by the proposed Constitution to the federal government are few and defined.… [They] will be exercised principally on external objects, as war, peace, negotiation, and foreign commerce.” Since the Constitution grants the federal government no role in higher education, Washington may only be involved in ways that support legitimate federal concerns. Ultimately, that means maintaining the Senior Reserve Officers’ Training Corps, the service academies, and national defense–related research, and perhaps assisting institutions in federal jurisdictions, such as the District of Columbia.

Washington cannot, however, withdraw immediately. Abruptly ending federal student aid would leave millions of students scrambling for funds and would overwhelm private lenders, schools, and charitable organizations that have made plans based on expected levels of federal involvement. What follows is an overview of a six-year plan to withdraw the federal government from higher education:

Two years: End direct federal aid to institutions, with the possible exceptions of Howard University and Gallaudet University, both of which are in the District of Columbia and receive significant federal dollars. If schools are to be directly subsidized, state or local governments should do it. Also, federal tax incentives, which are heavily skewed to the well-to-do—529 plans, Coverdell education savings accounts, and Lifetime Learning Credits—should end, though existing savings should receive the tax treatment promised when the money was deposited.Four years: Phase out “unsubsidized” federal loans, including parent and grad PLUS, which are available without regard to financial need. There is little justification for supplying loans to people who could otherwise afford to pay for college. The maximum available loan should be reduced in equal increments over four years, to a complete phaseout.Six years: Eliminate all remaining aid programs. Each year after the enactment of the federal phaseout, the maximum Pell Grant should be reduced in equal increments. Similarly, maximum “subsidized” loan sizes should be reduced in equal increments.

Conclusion

The federal presence in higher education is ultimately self-defeating, fueling huge price inflation and overconsumption. The solution is to avoid the superficial thinking that all “education” is good and to let people freely decide what education they need and how they will pay for it.

Suggested Readings

Amselem, Mary Clare, et al. “Rightsizing Fed Ed: Principles for Reform and Practical Steps to Move in the Right Direction.” Cato Institute Policy Analysis no. 891, May 4, 2020.

Arum, Richard, and Josipa Roksa. Academically Adrift: Limited Learning on College Campuses. Chicago: University of Chicago Press, 2011.

Caplan, Bryan. The Case against Education: Why the Education System Is a Waste of Time and Money. Princeton, NJ: Princeton University Press, 2018.

Fuller, Joseph B., and Manjari Raman, “Dismissed by Degrees: How Degree Inflation Is Undermining U.S. Competitiveness and Hurting America’s Middle Class,” Harvard Business School, December 13, 2017.

McCluskey, Neal. “Point: Canceling Student Debt by Presidential Decree Is Wrong on Many Levels.” Tribune Democrat, January 1, 2021.

Mitchell, Josh. The Debt Trap: How Student Loans Became a National Catastrophe. New York: Simon and Schuster, 2021.

Pierce, Kate. “College, Country Club or Prison?” Forbes, July 29, 2014.

Robinson, Jenna A. “The Bennett Hypothesis Turns 30.” James G. Martin Center for Academic Renewal, December 26, 2017.

Zywicki, Todd J., and Neal P. McCluskey, eds. Unprofitable Schooling: Examining Causes of, and Fixes for, America’s Broken Ivory Tower. Washington: Cato Institute, 2019.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.