Congress should

-

cut the federal corporate income tax rate to 15 percent; and

-

withdraw from international agreements that limit competition, raise taxes, and increase compliance costs.

The flow of capital across international borders has soared since the 1980s. Corporations and individuals are moving their investments to countries with lower taxes and better growth opportunities. Governments have responded by cutting their tax rates to attract business activity and spur economic growth.

The average corporate income tax rate in the high-income nations of the Organisation for Economic Co-operation and Development (OECD) declined from 47 percent in 1980 to 23 percent in 2021. Many countries have also cut their tax rates on dividends, capital gains, and estates, and most countries that had annual wealth taxes have abolished them.

In a globalized economy, it makes sense for countries to cut taxes on capital because taxes on mobile bases are more distortionary than taxes on less mobile bases, such as labor. Because of international capital flows, the burden of capital taxes likely lands mainly on labor anyway, so it is simpler and more transparent to tax labor directly.

Before the Tax Cuts and Jobs Act (TCJA) of 2017, the United States deterred investment because it had one of the highest corporate tax rates among OECD countries. America also had an aggressive worldwide approach to taxing corporate foreign income. That approach encouraged U.S. companies to keep their earnings offshore, put them at a disadvantage in foreign markets compared with foreign-based companies, and induced some of them to restructure and move their headquarters abroad.

The TCJA addressed these problems. The law cut the federal corporate tax rate from 35 percent to 21 percent, which brought down our average federal-state rate to 26 percent. The TCJA also moved toward territorial treatment of foreign earnings, which generally allows corporations to repatriate earnings without an additional layer of tax. Finally, the law imposed rules to reduce profit shifting to low-tax countries, including what is called the global intangible low-taxed income (GILTI) rules, which impose a surtax on foreign subsidiary profits deemed excessive.

The foreign income provisions of the TCJA are very complex, but the law was generally a step in the right direction. Computer modeling by the Tax Foundation found that the TCJA mainly eliminated incentives for U.S. corporations to shift profits abroad. Similarly, an analysis using the Penn-Wharton budget model found that corporations repatriated an additional $140 billion from foreign subsidiaries in the three years after the TCJA was passed.

Corporate Tax Rates and Revenues

The Biden administration has a different view of corporate taxes than did the Trump administration. It favors higher taxes on corporations, more punitive treatment of foreign earnings, and the imposition of a global minimum tax. Treasury Secretary Janet Yellen has complained about a “30‐year race to the bottom” in global corporate tax rates. She is right that corporate tax rates have fallen, but she does not appear to appreciate that these reforms have contributed to economic growth around the world.

Tax economists generally agree that the corporate income tax is a highly distortionary tax, and they warn against high rates. In a 2008 study comparing major taxes, OECD economists concluded, “Corporate taxes are found to be most harmful for growth.” That is why it makes sense for countries to focus on corporate tax rate cuts. Cutting rates supports capital investment, which over time raises productivity and worker wages. Corporate tax rate cuts have been positive for the global economy, not the zero-sum game that Yellen seems to think.

Yellen and other critics of corporate tax cuts promote the false narrative that the reforms have starved governments of revenues. Yellen is pushing to limit tax competition and impose a global minimum corporate tax so that “governments have stable tax systems that raise sufficient revenue.” Similarly, the OECD worries that tax “base erosion constitutes a serious risk to tax revenues” and that multinational corporations (MNCs) are “not paying their fair share of tax.”

However, as corporate tax rates have fallen around the world, corporate tax revenues have risen. When rates fall, corporations reduce tax avoidance and increase investment, which boosts growth and expands the tax base. Over the years, many countries have also tightened tax regulations to broaden their corporate tax bases.

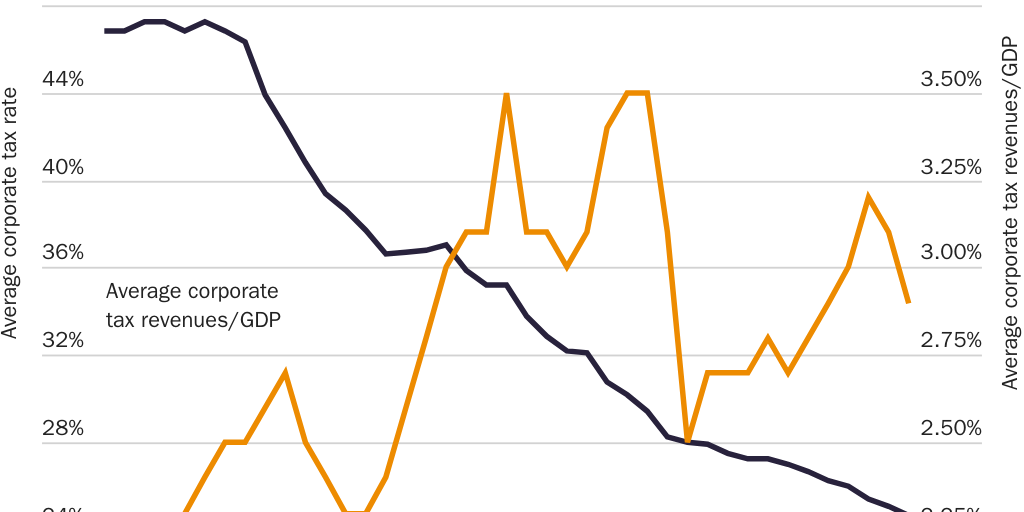

For 22 OECD countries that have good data back to 1980, I calculated average corporate tax revenues as a percentage of gross domestic product (GDP) and also average corporate tax rates including federal and state or provincial rates. For the 22 countries, the corporate tax rate averaged 46.2 percent in the 1980s, 37.5 percent in the 1990s, 31.3 percent in the 2000s, and 26.6 percent in the 2010s.

As rates fell, revenues trended upward, as shown in Figure 1. Corporate tax revenues for the 22 countries averaged 2.4 percent of GDP in the 1980s, 2.7 percent in the 1990s, 3.2 percent in the 2000s, and 2.9 percent in the 2010s. Revenues were down a bit in the 2010s from the 2000s, but they were up from the 1980s and 1990s.

A 2021 OECD report looks at corporate taxes in more than 100 countries. From 2000 to 2018, the average corporate tax rate fell from 28.3 percent to 20.0 percent, but corporate tax revenues as a percentage of GDP rose from 2.7 percent to 3.2 percent. Despite all the news stories decrying big corporations for not paying taxes, corporate tax revenues around the globe are at quite high levels even though rates are down. OECD studies often complain about “base erosion,” but the data reveal that tax bases must have expanded because tax revenues are so buoyant.

Ignoring these realities, the Biden administration has proposed raising the federal corporate tax rate. It has also proposed increasing taxes on the foreign subsidiaries of U.S. corporations, which would hurt the U.S. economy because those subsidiaries often complement U.S. production. Corporations frequently establish subsidiaries to penetrate foreign markets, which helps boost U.S. exports. But Biden’s approach would put U.S. companies operating abroad at a disadvantage compared with companies headquartered elsewhere. Tax Foundation modeling finds that Biden’s proposed tax rate hike and foreign income proposals would increase the shifting of profits abroad, on net, not reduce it as the administration claims.

Creating a Global Tax Cartel

Multinational corporations are hugely important to the U.S. economy. They are responsible for three-quarters of all business research and development and more than half of U.S. exports. Taxing MNC profits is complex because determining where profits are actually earned can be difficult. Corporations can shift profits on paper from high-tax to low-tax jurisdictions in many ways. Today’s MNCs are highly reliant on intellectual property, for which it is especially difficult to determine the proper location of profits.

As a result, an enormous amount of accounting and legal brainpower goes into tax planning, compliance, and administration for MNCs. Governments have layered ever more anti-avoidance tax rules onto MNCs, including rules for transfer pricing, interest deductibility, passive foreign income, and GILTI. Corporations have responded to the rules by engineering new ways of minimizing tax, which in turn has prompted governments to add more rules in a never-ending and wasteful cycle.

Given that the corporate income tax ultimately lands on individuals, the best solution to the increasingly complex corporate tax would be to fully repeal it and for governments to rely on simpler taxes, such as payroll taxes and consumption taxes. But a compromise is for governments to slash corporate tax rates to perhaps 15 percent or less, which would reduce incentives for tax avoidance and the need for such complex anti-avoidance rules.

Unfortunately, when news stories highlight a few famous corporations that have not paid taxes in some years, political leaders respond by layering on more regulations. As an example, the Inflation Reduction Act passed in August 2022 included a new 15 percent corporate minimum tax that will substantially increase business tax compliance costs because it is based on a different accounting system than the normal corporate income tax.

Another response has been for governments to support the OECD’s push for global rules to limit the ability of countries to cut taxes and attract investment and profits. Since 2013, the OECD effort has gone under the name Inclusive Framework on Base Erosion and Profit Shifting (BEPS).

When the Democrats gained control of the White House in 2021, the OECD’s BEPS effort moved into high gear. More than 100 countries agreed last year to the OECD’s “Two-Pillar Solution to Address the Tax Challenges Arising from the Digitalisation of the Economy.” To implement the proposals, countries will generally need to pass bills in their legislatures, and the European Union will need the unanimous support of its members. In the United States, a two-thirds vote in the Senate would be needed to approve the agreement as a treaty. But political leaders are pushing hard to make it happen in 2023, and the deal would affect countries even if they do not sign on.

This is the basic structure of the agreement:

- Pillar 1. For the 100 or so largest global corporations, 25 percent of profits above a 10 percent return on revenues would be reallocated for taxing purposes to governments around the world based on each company’s sales in each country. The OECD estimates that about $125 billion a year in profits would be reallocated from governments of countries that are homes to large MNCs, such as the United States, to governments of countries where MNCs sell their products.

- Pillar 2. The agreement creates a global minimum tax of 15 percent on subsidiaries in each foreign country of each MNC that has annual revenues of more than €750 million. The pillar will be operationalized through three separate mechanisms. A carve-out is created for estimated earnings related to real activities based on tangible assets and payroll. The OECD estimates that this pillar would raise global taxes by $150 billion a year.

The workings of these mechanisms would be exceedingly complex. There are exceptions for certain industries and certain types of tax breaks; the rules mix tax and financial statement accounting, there are dispute mechanisms, and the whole structure would be layered on top of existing tax systems. Companies and tax authorities would need to make many complex calculations with rules that would be gray, not black and white.

If this global tax structure is created, corporations would likely respond with new tax avoidance efforts. Politicians would then push to add more rules and to increase the 15 percent minimum tax rate. Indeed, the OECD Two-Pillar document discusses ways to “expand the scope” of the rules over time, including increasing the number of companies in Pillar 1. If governments move ahead, the OECD structure could ultimately become something like an Internal Revenue Service for the world.

Supporters of the agreement use language that is vague and emotional, not scientific. Yellen mimics the OECD in saying that a global deal is needed for “ensuring corporations pay their fair share.” But “fair share” is never defined, and corporate tax revenues as a percentage of GDP are up, not down. Besides, the corporate tax burden ultimately falls on individuals as shareholders, workers, or consumers. As such, it is meaningless to talk about the corporate “fair” share.

Also, the Two-Pillar report mixes up governments and countries. The report says, “All types of economies … will benefit from extra tax revenues” under the global tax deal. Governments may gain, but overall economies will not gain as more taxes are extracted from the private sector. The report says that corporate tax avoidance “costs countries” in lost tax revenues. Avoidance may cost governments, but it represents savings to businesses, and thus savings to shareholders, workers, and consumers. With regard to the overall economy, the Two-Pillar deal itself would impose costs because higher corporate taxes and more tax regulations would reduce investment and increase wasteful compliance burdens.

Finally, the OECD Two-Pillar deal may not even generate added revenues for the U.S. government. First, with the TCJA in place, the United States already has strong incentives for MNCs to invest at home, to repatriate profits, and not to shift paper profits abroad. Second, the purpose of Pillar 1 is to transfer tax revenues from countries that are home to MNCs to other countries where products are consumed. The United States is home to many MNCs and thus may be a revenue loser from Pillar 1. Third, low-tax nations will likely respond to the Pillar 2 global minimum tax by raising their income tax rates, which through the foreign tax credit mechanism would reduce U.S. tax revenues. Tax Foundation modeling finds that if low-tax nations raised their tax rates to the new global minimum, the U.S. government would lose revenue overall.

Advantages of Tax Competition

Monopolies in business usually generate bloated costs and higher prices. As such, economists favor subjecting industries to competition to reduce prices and improve efficiencies. Governments are monopolies, and they also get bloated, so we should look for ways to subject them to competition.

International competition for investment dollars is one way to do it. Taxes are an important driver of investment flows, so political leaders wishing to spur economic growth are under some pressure to restrain them. Cutting tax rates on capital would be beneficial even without globalization, but international competition has helped nudge policymakers in the right direction on reforms.

Yellen and the OECD are aiming to create an international cartel to protect government as a high-cost monopoly, just as the Organization of the Petroleum Exporting Countries (OPEC) cartel limits competition to keep oil prices high. In backing the OECD effort in May 2021, the Yellen Treasury said it wanted to “end the pressures of corporate tax competition.” But many economists disagree with that direction. In a 2001 letter, 200 economists—including Nobel Prize winners Milton Friedman and James Buchanan—advised President George W. Bush that the United States should not support the OECD’s “tax cartel” efforts because “tax competition is a liberalizing force in the world economy, something that should be celebrated rather than persecuted.”

The OECD’s efforts are based on the false theory that governments left alone will always act in the public interest and produce optimal tax policy. But Nobel Prize–winning economist Gary Becker once observed that “competition among nations tends to produce a race to the top rather than to the bottom by limiting the ability of powerful and voracious groups and politicians in each nation to impose their will at the expense of the interests of the vast majority of their populations.” Becker recognized that policymakers don’t always act in the public interest, and so external competition is a useful constraint. Globalization puts beneficial pressure on policymakers to raise taxes only when really necessary.

The OECD does not see it that way. It calls tax competition that it does not favor “harmful” and “unhealthy.” It worries that when tax rates are not harmonized across countries, investment flows are distorted. But the OECD could seek harmonization by asking high-tax countries to slash their tax rates to equalize them with low-tax countries. It could push for a global maximum tax rate of 15 percent, rather than a minimum. Or it could call for countries to abolish corporate income taxes altogether, since those are highly inefficient taxes in today’s global economy. Instead, the OECD effort is one-sided in favoring more taxing power and bigger government.

Consider that many policy differences between countries drive investment flows across international borders, including differences in education, infrastructure, and the rule of law. For instance, one could say that America engages in “harmful education competition” because our top universities attract many foreign students. If the OECD applied its anti-competition reasoning, it would demand that we end this “unfair” advantage and reduce our university quality to match the lower standards abroad.

The OECD’s tax cartel effort can be contrasted with the efforts of the World Trade Organization (WTO) to liberalize trade. Trade barriers are like taxes that reduce cross-border activity. Part of the WTO’s role is to be a facilitator in reducing these taxes and expanding global trade to every country’s benefit. If a country cuts its trade barriers and generates more trade, the effort is not criticized by economists as “harmful trade competition,” and the country is not ostracized as a “trade haven.” With its tax cartel efforts, the OECD is like an anti-WTO.

Why the difference in tax and trade politics? Trade theorists properly focus on the benefits to the private sector of less government and more trade. But the OECD’s tax advocacy defends governments at the expense of the private sector. In a study on the OECD, Andrew Morriss and Lotta Moberg describe how the organization previously advocated for competition, labor market flexibility, fiscal discipline, and open markets. But on tax policy, it changed direction in the 1990s and began calling to restrict competition. Morriss and Moberg note that the “OECD evolved from a forum focused on lowering transactions costs to increase private sector competition across borders into a cartel aimed at restricting competition among states.”

The authors attribute the change partly to the influence of some large and high-tax OECD countries. The governments of France and Germany, for example, have not appreciated rising tax competition from smaller, lower-tax nations. Ireland, for instance, has generated stiff competition in Europe with its 12.5 percent corporate tax rate. Just a few decades ago, Ireland was much poorer than the largest economies in Europe, but its enactment of a low corporate tax rate and other reforms has attracted booming inward investment, which has helped the Celtic Tiger grow strongly and surpass the living standards of nearly all other countries in Europe.

The OECD global tax deal would limit the ability of other nations to adopt Ireland’s successful growth strategy. Estonia is another small country that has enacted a low and efficient corporate tax system. Such reform successes should be emulated, not condemned. Although Yellen and the OECD often talk about “fairness” in taxation, their push to impose a global tax cartel can be viewed as an arrogant move by the governments of big and powerful countries to limit the growth opportunities of smaller and poorer nations.

Policy Options

America’s role in the world economy should be to foster competition, not to join monopolistic cartels aimed at punishing countries that adopt pro-growth tax reforms. The United States should pull out of the OECD Two-Pillar effort and other initiatives that would limit tax competition and undermine national sovereignty. Taxation is a core power of government and a lever of citizen control over government in a democracy. We should not outsource that power to an international bureaucracy.

At the same time, Congress should work on tax reforms here at home. The Tax Foundation’s International Tax Competitiveness Index places the United States just 21st out of 37 countries. Policymakers should build on the TCJA and cut the federal corporate tax rate from 21 percent to 15 percent, which would spur growth and further reduce incentives to shift profits abroad. Policymakers should strive to make America the best place in the world for investment, business creation, and worker opportunities.

Suggested Readings

Arnon, Alexander, Zheli He, and Xiaoyue Sun. “Profit Shifting and the Global Minimum Tax.” Penn-Wharton Budget Model, July 21, 2021.

Bunn, Daniel. “U.S. Cross-Border Tax Reform and the Cautionary Tale of GILTI.” Tax Foundation, February 17, 2021.

Bunn, Daniel, and Elke Asen. “International Tax Competitiveness Index 2021.” Tax Foundation, October 18, 2021.

Center for Freedom and Prosperity. https://freedomandprosperity.org/tag/oecd.

Desai, Mihir A., C. Fritz Foley, and James R. Hines. “Economic Effects of Regional Tax Havens.” National Bureau of Economic Research Working Paper no. 10806, October 2004.

Edwards, Chris, and Daniel J. Mitchell. Global Tax Revolution: The Rise of Tax Competition and the Battle to Defend It. Washington: Cato Institute, 2008.

Kallen, Cody. “Options for Reforming the Taxation of U.S. Multinationals.” Tax Foundation, August 12, 2021.

Morriss, Andrew P., and Lotta Moberg. “Cartelizing Taxes: Understanding the OECD’s Campaign against ‘Harmful Tax Competition.’” Columbia Journal of Tax Law 4, no. 1 (2013): 1–64.

Organisation for Economic Co-operation and Development. Corporate Tax Statistics. 3rd ed. Paris: OECD, 2021.

———. “Taxation and Economic Growth.” Economics Department Working Paper no. 620, July 3, 2008.

———. Two-Pillar Solution to Address the Tax Challenges Arising from the Digitalisation of the Economy. Paris: OECD, October 2021.

Roberts, James, David Burton, Nicolas Loris, and Adam Michel. “Organization for Economic Co-operation and Development (OECD): What America Should Do.” Heritage Foundation Backgrounder no. 3593, March 16, 2021.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.