The Treasury Department will soon release its recommendations for regulating stablecoins, digital currencies whose value is pegged to “stable” reserve assets, such as the dollar. Reportedly, Treasury is also going to recommend that the Financial Stability Oversight Council (FSOC) formally review whether stablecoins pose a threat to financial stability.1 Instead of making these recommendations, the Biden administration should help provide the regulatory clarity that the blockchain industry badly needs. More broadly, the spectacle of proposing an FSOC review for stablecoins while sanctioning the systemic risk posed by the housing finance giants Fannie Mae and Freddie Mac only strengthens the case for Congress to eliminate the FSOC.

Overview of Stablecoins

Stablecoins are special cryptocurrencies designed to maintain a stable value rather than display the volatile price movements seen with other digital currencies, such as Bitcoin and Ethereum. Although the details can differ widely, all stablecoins aim to achieve this price stability by tying their value to some other asset. Some of the most popular stablecoins tie their price to national fiat currencies, such as the dollar, but others anchor their price to precious metals, short-term corporate debt, or even other cryptocurrencies.2

Typically, the issuer of the stablecoins sets up a reserve account in a traditional bank, where it holds the reserve assets (collateral) for the coins. One of the oldest stablecoins is Tether, a stablecoin fully backed by reserves that, according to its website, include “traditional currency and cash equivalents and, from time to time … other assets and receivables from loans made by Tether to third parties.”3 Tether is also the largest stablecoin, with a market value of $68 billion.4

The general idea behind stablecoins is that their stable value will help promote their use as a widespread medium of exchange, but they have not yet achieved that status. As of now, it appears that the most common use for stablecoins is transferring money between crypto exchanges, and the biggest financial risk from most stablecoins is whether the issuing entity has the reserves that it claims to have. Unsurprisingly, multiple countries increased their regulatory scrutiny of stablecoins when Facebook, with its network of several billion people, announced its Libra stablecoin project (this is yet to launch, but it is now referred to as Diem). Several members of Congress, for instance, expressed concerns that digital currencies might undermine the dollar and potentially have an “unprecedented impact on the global financial system.”5

The Financial Stability Oversight Council and Systemic Risk

The 2010 Dodd-Frank Act created the FSOC based on the view that regulators needed to focus on systemic risk rather than the safety and soundness of individual financial institutions. The FSOC is a 15-member council that includes 10 voting seats and 5 nonvoting positions. The 10 voting seats are filled by the heads of nine federal financial regulatory agencies, including the Treasury Secretary (serving as the chair of the FSOC); chairs of the Federal Reserve, the Securities and Exchange Commission (SEC), and the Commodity Futures Trading Commission (CFTC); and the director of the Federal Housing Finance Agency (FHFA).

Congress gave the FSOC the authority to single out systemically important financial institutions, as well as nonbank firms engaged in activities that threaten the financial stability of the United States, for heightened regulations.6 One reason to view this approach skeptically is that federal regulators had, in fact, concentrated on systemic risk for decades prior to the 2008 financial crisis.7 Regulating financial markets in this manner also suggests that government officials have superior knowledge regarding which risks people should take, and it implies that the federal government should prevent people from losing money. Inevitably, this approach impedes the functioning of markets and leads to government bailouts that socialize private losses. Another problem is that Congress gave regulators enormous discretion to identify threats to “financial stability” without clearly defining the concept.8 The following section demonstrates just how much power Congress has delegated to the agencies.

Dodd-Frank and the 2019 FSOC Guidance

Section 113 of the Dodd-Frank act9 gives the FSOC the authority to determine “that a U.S. nonbank financial company shall be supervised by the Board of Governors and shall be subject to prudential standards” if the FSOC determines “that material financial distress at the U.S. nonbank financial company, or the nature, scope, size, scale, concentration, interconnectedness, or mix of the activities of the U.S. nonbank financial company, could pose a threat to the financial stability of the United States.”10 As mentioned, the U.S. Code does not define the term “financial stability.”

Separately, Section 120 of Dodd-Frank authorizes the FSOC to make recommendations to the appropriate financial regulators, most of which are on the FSOC, to apply heightened regulations. The FSOC can make such recommendations “for a financial activity or practice conducted by bank holding companies or nonbank financial companies” if the FSOC determines that “the conduct, scope, nature, size, scale, concentration, or interconnectedness of such activity or practice could create or increase the risk of significant liquidity, credit, or other problems [emphasis added] spreading among bank holding companies and nonbank financial companies, financial markets of the United States, or low-income, minority, or underserved communities.”11

Given the uncertainty surrounding how it might review financial firms and activities, the FSOC has issued rules and guidance to clarify how it might fulfill its statutory duties. Based on interpretative guidance it issued in 2019, the FSOC now generally pursues an activities-based approach for Section 113 recommendations rather than singling out specific companies.12 This guidance states that the FSOC will “pursue entity specific determinations under Section 113 of the Dodd-Frank Act only [emphasis added] if a potential risk or threat cannot be adequately addressed through an activities-based approach.”13 Still, no statutory requirement binds the FSOC to using the activities-based approach, and any future FSOC can issue new guidance that outlines an alternative method.

The 2019 guidance explains that, to implement the activities-based approach for nonbank financial firms, the FSOC will “examine a diverse range of financial products, activities, and practices that could pose risks to U.S. financial stability.”14 The guidance also states that “When monitoring potential risks to financial stability, the Council intends to consider the linkages across products, activities, and practices, and their interconnectedness across firms and markets,” and that its monitoring may include, among other items, “information such as historical data, research regarding the behavior of financial market participants, and new developments that arise in evolving marketplaces.”15

Separately, the guidance notes that the FSOC will assess the extent to which several characteristics “could amplify potential risks to U.S. financial stability arising from products, activities, or practices,” where these characteristics include credit risk, leverage, liquidity risk, counterparty risk, operational risks, growth in nonregulated financial sectors, and the risk to stability from essentially any financial instrument.16 Partly because it is difficult to objectively evaluate even these specific characteristics, the FSOC’s guidance explains that it will generally focus on four framing questions:

- How could the potential risk be triggered?

- How could the adverse effects of the potential risk be transmitted to financial markets or market participants?

- What impact could the potential risk have on the financial system?

- Could the adverse effects of the potential risk impair the financial system in a manner that could harm the nonfinancial sector of the U.S. economy?17

Arguably, this framework does provide more transparency and certainty than previously issued FSOC guidance. Still, Congress gave the council enormous discretion to issue new rules and regulations, and even to restrict the ability of firms to offer a product or service.

Simply put, the Dodd-Frank Act gave federal regulators the authority to selectively define financial stability, and to impose new regulations based on subjectively determined potential threats to their own concept of financial stability. Giving federal regulators the power to designate firms for special regulations and to outlaw or curtail specific economic activities based on ill-defined concepts is inconsistent with a system of free enterprise or of limited government. A brief comparison of the current risks in the housing market versus the theoretical risks in stablecoin markets helps demonstrate why Congress should not have delegated this sort of authority to federal regulators.

Housing Finance Risks versus Stablecoin Risks

Measured by its total market value, stablecoins are currently very small relative to other segments of U.S. financial markets. According to CoinMarketCap, the market capitalization of all stablecoins is $129.4 billion as of October 4, 2021, and the largest 10 stablecoins account for most of that total. Tether, the oldest and largest stablecoin, represents 53 percent ($68 billion) of the total market value.

For reference, the total market value of stablecoins pales in comparison to the total value of dollars in circulation ($2 trillion),18 the total Treasuries outstanding ($5.4 trillion),19 the total assets in money market funds ($4.5 trillion),20 and the total market capitalization of equities ($40.7 trillion).21 Of course, the size of any single stablecoin—or the total market—could rapidly increase, a concern that some Treasury officials have expressed.22 The possibility of a tech firm such as Facebook launching its own stablecoin lends plausibility to this idea, but even this rapid scaling-up scenario says nothing specific about the systemic risks created by issuing digital tokens tied to safe assets held in reserve.

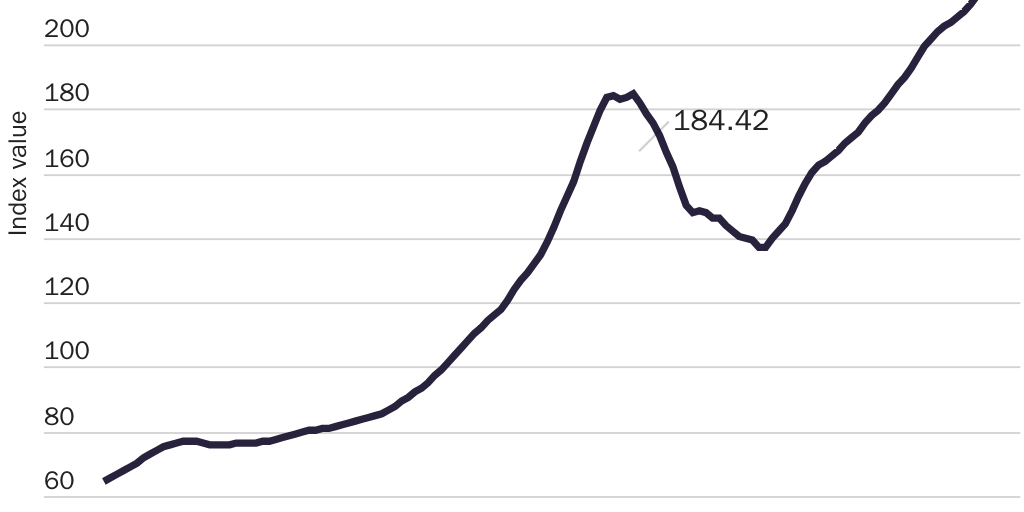

In contrast, the housing finance market has a long history of causing financial crises, and the most recent crash provides the FSOC with concrete answers to each of the four framing questions in its 2019 guidance.23 Notably, home prices have now risen to 43 percent more than where they peaked prior to their 2007 crash (see Figure 1),24 and empirical evidence links large increases in housing prices to banking crises.25 Other research, when examining asset price booms and busts in the Organisation for Economic Co-operation and Development countries from 1970 to 2001, estimates that the probability of a real estate boom ending in a bust is 53 percent, whereas stock market booms have just a 13 percent probability of ending in a crash.26

Moreover, the role of housing prices in American financial crises is linked to high-leverage lending, where those policies ensure that both borrowers and those who fund mortgages can do so with relatively little loss-absorbing equity.27 For decades, U.S. housing finance policy has helped increase the number of mortgages requiring low down payments for financing homes, even though evidence clearly indicates that the risk of loan default increases (particularly among first-time home buyers) as the loan-to-value ratio increases.28 On the funding side, the Basel capital requirements have always provided financial institutions with capital relief for holding mortgage-backed-securities rather than whole loans, while Fannie Mae and Freddie Mac have long enjoyed lower equity requirements than banks.29

As of December 31, 2020, Fannie and Freddie had combined total assets of $6.6 trillion, representing approximately 42 percent of the nation’s outstanding mortgage debt.30 The combined total asset figure for Fannie and Freddie exceeds the combined total assets of the two largest U.S. banks (JP Morgan Chase reports $3.21 trillion, while Bank of America reports $2.32 trillion), and their respective sizes exceed that of all the other large American banks.31 One reason that Fannie and Freddie are so much larger than competing financial institutions is that they have been allowed to operate with higher leverage than their competitors throughout virtually their entire existence.

Objectively, it makes little sense for the Biden administration to recommend an FSOC review for issuing stablecoins while condoning the systemic risk posed by Fannie and Freddie. Even more bizarre, though, is the recent announcement by the Federal Housing Finance Agency that it wants to lower the companies’ future capital requirements and make it easier for them to acquire more single-family mortgages that have high risk characteristics.32 These decisions could result in federal regulators making it all but impossible to economically issue stablecoins, while literally fueling another financial crisis with higher-risk loans funded by Fannie and Freddie. Ultimately, of course, Congress would be responsible for such an outcome.

Congress created this regulatory framework—implemented by a council consisting of multiple regulators headed by executive branch appointees—that can easily impose new regulations on any segment of the financial sector for virtually any reason. This sort of regulatory environment is incompatible with a free-enterprise system based on limited government principles because it protects incumbent firms, punishes innovative companies, breeds cronyism and capture, and fails to provide the regulatory certainty that financial entrepreneurs need. It will reduce competitiveness and financial diversification, thus shrinking economic opportunities and financial security for millions of Americans.

Conclusion

Financial companies do not require rules and regulations that replace the judgment of owners, employees, and investors with those of government bureaucrats. Financial markets are still markets, and the same economic principles that apply to other segments of the economy apply to the financial sector. Just as in other areas of the economy, excessive government regulation prevents financial firms from best serving the needs of their customers and, therefore, society. Federal officials have no special knowledge regarding the best way to serve financial-market participants.

The Biden administration is missing an opportunity to provide the much-needed clarity that the blockchain industry has been seeking for close to a decade. Worrying about the systemic risk associated with stablecoins does nothing to fix the existing regulatory problems that matter, and the spectacle of proposing an FSOC review for stablecoins while condoning the systemic risk posed by Fannie Mae and Freddie Mac only strengthens the case for Congress to eliminate the FSOC.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.