The 118th Congress has an opportunity to adopt responsible fiscal policy that controls the growth in spending and takes credible steps to stabilize the U.S. debt in the medium and long term. American public debt is at economically damaging levels and growing at an unsustainable rate. Congress should stabilize federal debt to reduce the possibility of a fiscal crisis. Members of the 118th Congress should act fiscally responsibly by cutting spending to enable economic growth and complement the Federal Reserve’s actions to reduce inflation. Legislators should further commit to a credible fiscal stabilization path, reduce and cap discretionary spending, restore the earmark ban, and reform social and entitlement programs. These actions will be effective in sustainably reducing federal deficits and stabilizing the debt.

Introduction

Excessive spending and high debt threaten the ability of the federal government to provide essential public goods, such as national defense, and to respond effectively to unexpected crises, such as wars and pandemics. Excessive government spending also reallocates scarce economic resources toward lower-value politically inspired projects, imposes large economic burdens on American taxpayers, and undermines economic growth. Debt that grows persistently relative to gross domestic product (GDP) will eventually cause a fiscal crisis, during which investors would lose confidence in U.S. Treasury bonds.

In fiscal year (FY) 2022, the federal budget deficit-the gap between annual spending and revenues-totaled $1.4 trillion, or 5.5 percent of U.S. GDP.1 Meanwhile, the total or gross federal debt approached $31 trillion, of which $24.3 trillion was federal debt held by the public-that is, the debt the federal government has borrowed in credit markets.2 Third-quarter 2022 GDP is $25.7 trillion. Thus, the gross federal debt, which includes borrowing in federal government trust funds (i.e., Social Security), stood at 120 percent of GDP at the end of FY 22, of which federal debt held by the public made up 95 percent of GDP.3

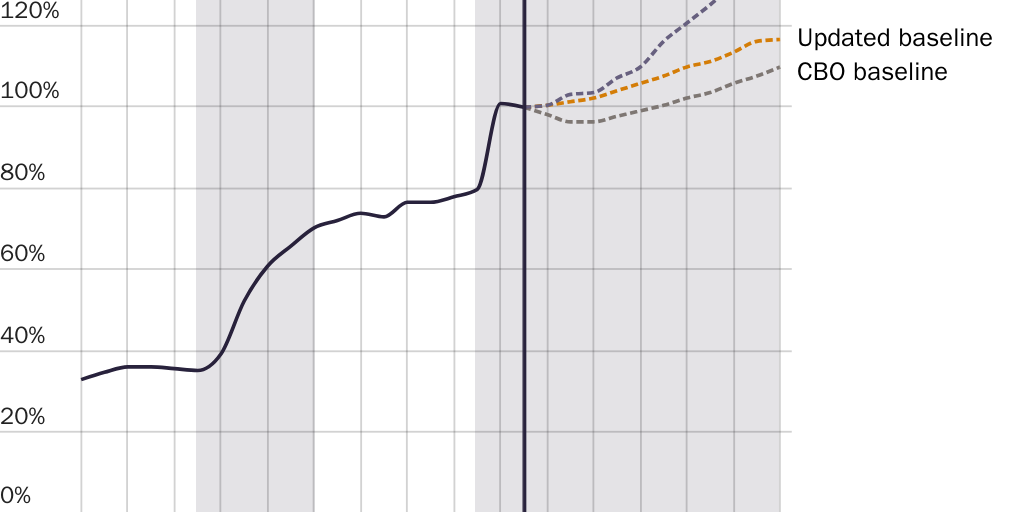

The Congressional Budget Office (CBO) projected a bleak outlook for federal finances when it last issued baseline figures in May 2022, and this outlook has worsened since.4 The CBO projected that federal debt held by the public would reach 110 percent of GDP by 2032—the highest level ever, exceeding the debt following World War II. The Committee for a Responsible Federal Budget (CRFB) produced its own version of the CBO’s baseline in November 2022 to include the effects of higher inflation, higher interest rates, slower economic growth, and more deficit spending. Under this updated baseline, the CRFB projects that debt will reach 116 percent of GDP by 2032. Using more realistic assumptions than the CBO, the CRFB produced an alternative baseline estimate that projects that debt will reach 138 percent of GDP by 2032.5

Assuming Congress allows middle-class tax cuts for individuals and families to expire as scheduled in 2025, which is unlikely, publicly held debt would reach 185 percent of GDP at the end of the CBO’s long-run 30‐year projection period. Under more realistic assumptions, where Congress extends those tax cuts and revenues return to their 50‐year average, publicly held debt would exceed 260 percent of GDP by 2052.6

Both the CBO and the CRFB projections may be too optimistic, as they do not include the potential of significant and unpredictable crises during their respective projection periods, such as a banking crisis or another pandemic, that Congress would likely respond to with additional deficit spending.

Figure 1 shows historical and projected debt, using similar assumptions as the CRFB for the updated and alternative baseline.

Members of Congress must first stop excessive spending. The Biden administration added about $5 trillion in new deficits in just the past two years.7 The new Congress should refrain from adding to deficits and adopt the following fiscal policies:

- Stabilize the growth in federal debt.

- Commit to a credible fiscal stabilization path.

- Establish a bipartisan commission to reform major entitlement programs such as Social Security and Medicare.

- Reduce and cap discretionary spending.

- Return discretionary spending to pre-pandemic (FY 2019) levels.

- Restore discretionary spending caps.

- Limit the growth in top-line discretionary spending to no more than 2 percent annually.

- Restore the earmark ban.

- Avoid new stimulus spending.

Avoid a Possible Future Fiscal Crisis

The 118th Congress will confront the federal debt limit this year. The Bipartisan Policy Center estimates that the Treasury will reach the current debt limit of $31.38 trillion in late summer or early fall of 2023.8 This is a key opportunity to pursue a fiscal stabilization package that pairs the inevitable increase in the debt limit with policies that stabilize the growth in the debt over the medium and long term.

Reaching the debt limit is an important wake-up call to legislators to correct unsustainable spending. Effective spending reforms should keep the government from increasing its debt as a share of GDP. It’s especially critical to control growth of the federal debt now because such high and rising government debt-significantly exceeding 90 percent of GDP-is associated with lower economic growth.9 The debt subject to the limit exceeds 120 percent of GDP and, as Figure 2 illustrates, is accelerating.

Leveraging the debt limit to reform federal spending is particularly relevant because two-thirds of the federal budget grows on autopilot. Entitlement or mandatory spending increases are based on statutes and formulas that, in some cases, were adopted decades ago and that Congress rarely reviews. The most prominent examples are spending on old-age entitlement programs, especially Medicare and Social Security, which are set to grow dramatically as more baby boomers approach program eligibility ages, while also living longer.

Lawmakers should not wait until a fiscal crisis forces austerity upon the government. At that point, it could be too late to make gradual policy changes that would allow Americans time to adjust to new fiscal realities of potentially relying more on personal savings, later retirement ages, and reduced entitlement benefits. The longer lawmakers wait to reform spending, the more dramatic and sudden the eventual impact of reforms and adjustments will be.

A self-inflicted fiscal crisis would erupt if investors lost confidence in the federal government’s willingness or ability to service its debt. Such a crisis is impossible to predict, but they have happened suddenly in other countries with unsustainable government debt and large persistent deficits.10

A fiscal crisis could also cause:

- a sudden and excessive rise in interest rates that disrupts investment;

- hyperinflation (rapid, accelerating, uncontrollable inflation) that disrupts employment and other markets; and

- unforeseeable ramifications affecting the relative global standing of the United States as an economic powerhouse, American foreign policy, and the desirability of the United States as a destination for immigrants and foreign direct investment.

Approaching the debt limit confronts Congress and the administration with the consequences of unsustainable budget decisions of the past. It also provides legislators with political coverage and leverage to change current policies to stabilize the debt. Constituents care about deficits and debt. Pairing an increase in the debt limit with measures to reduce future deficits and debt is the responsible choice. It could also be the politically prudent choice for legislators. Public and legislative pressure surrounding the debt limit has worked in the past to persuade Congress to reduce future debt. Most importantly, it’s much easier for Congress to avoid a potential future fiscal crisis by reforming spending today than dealing with such a crisis when it does come.

Lessons from the Budget Control Act of 2011

Brian Riedl, a senior fellow at the Manhattan Institute, examined 14 major deficit-reduction negotiations since 1980 and identified that “The debt limit had been tied to every major deficit deal between 1985 and 2011.” In some cases, the debt limit prompted a deficit reduction deal. In others, Congress tacked a debt limit increase onto a deficit reduction deal already in the works.11

The last major deficit reduction deal negotiated over a debt limit standoff was in 2011. Then Republican House Speaker John Boehner and then Democratic president Barack Obama agreed to the Budget Control Act within days of the Treasury reaching the debt limit. The resulting Budget Control Act of 2011 had several components. It increased the debt limit, required Congress to vote on a constitutional balanced budget amendment (the amendment failed), and imposed spending caps on defense and non-defense discretionary appropriations that limited spending on the one-third of the budget that Congress votes on each year.

The Budget Control Act also set up a bipartisan fiscal commission-the Joint Select Committee on Deficit Reduction, also known as the Super Committee. Congress tasked the committee with identifying spending cuts to mandatory or entitlement spending. In the event the committee process failed, automatic spending cuts, called sequestration in budget‐speak, would kick in. The committee did fail, and some sequestration ended up taking place. The Budget Control Act was not as effective as it could have been. Congress renegotiated it several times to avoid more substantive cuts to government programs. Nevertheless, the caps helped to limit the growth in discretionary spending for several years.

Congress Should Commit to a Credible Fiscal Stabilization Plan

Congress should learn from past deficit reduction deals and adopt a credible fiscal stabilization package that cuts spending immediately, reduces future spending growth, and reforms entitlement programs.12

The CRFB identified that stabilizing the publicly held debt at current levels of about 100 percent of GDP would require $7 trillion in savings over the first decade.13 They provide a mix of revenue raisers (40 percent) and spending cuts (60 percent) to illustrate one possible means to achieving this goal. Kurt Couchman with Americans for Prosperity emphasizes adopting a path to primary (non-interest) balance because credible fiscal plans benefit from having public support.14 A familiar goal, such as balancing the budget, is more likely to garner popular support than an arbitrary numeric goal, such as stabilizing the debt at a certain percentage of GDP or achieving $7 trillion in savings.15 Couchman argues that achieving full balance (including interest costs) would require $14.6 trillion in 10-year savings. The CRFB estimates that reaching primary balance (budget balance excluding spending on interest) in a decade would require $8.3 trillion in savings.

Achieving primary balance is a good first target. So is stabilizing the growth in the debt over 10 years. The important part is for Congress to agree to a credible and achievable fiscal target backed by specific policies that allow lawmakers to realize their target. Such a package would reassure holders of Treasury bonds that the U.S. government is committed to fiscal sustainability.

The specific budget reforms matter. A Heritage Foundation report distilling lessons from European austerity measures argues that increasing taxes was less effective in reducing deficits than spending cuts and also damaged the economy. The most successful fiscal adjustments, judged by their impact on deficits and the economy, reformed social programs and reduced the size and compensation of the government workforce.16

Andrew Biggs, a senior fellow at the American Enterprise Institute (AEI); Kevin Hassett, formerly a scholar at AEI; and Matthew Jensen, then the founding director of the Open Source Policy Center, drew similar conclusions, writing that:

Spending-based fiscal adjustment accompanied by supply-side reforms-such as liberalization of the markets for labor, goods, and services; readjustments of public-sector size and pay; public pension reform; and other structural changes-tend to be less recessionary or even lead to positive economic growth.17

Congress should establish a commission to consider reforms to entitlements. Entitlement spending growth will be responsible for the bulk of the increase in budget deficits over the next 10 years. Of the $21.1 trillion deficit projected from FY 2022 to FY 2032, nearly $12 trillion is due to deficit spending on Medicare and Social Security.18 As a percentage of GDP, the CBO projects that Social Security spending will increase from 4.9 percent of GDP in 2022 to 5.9 percent in 2032, reaching 6.4 percent of GDP by 2052. In the meantime, Medicare is projected to increase from 2.9 percent of GDP to 4.3 percent of GDP by 2032 and to 5.9 percent of GDP by 2052.19 It’s impossible to stabilize federal debt without reducing the growth in major entitlement spending.

The Government Accountability Office (GAO) surveyed entitlement reform efforts by developed, high-income Organisation for Economic Co-operation and Development (OECD) countries to distill lessons for U.S. policy consideration. One of the main lessons is that the process matters for enacting reforms. Successful entitlement reform is more likely to occur when several factors are present, including a broad consensus across parties and groups and the development of proposals in commissions that insulate policymakers from political risk. The GAO also pointed out that successful commissions were unlikely to adopt sweeping entitlement reform packages that sufficed on their own. Processes that allow for iterative reforms are helpful, such as standing commissions and mechanisms to automatically adjust benefits if adopted reforms prove insufficient to make programs sustainable.20

Congress Should Reduce and Cap Discretionary Spending

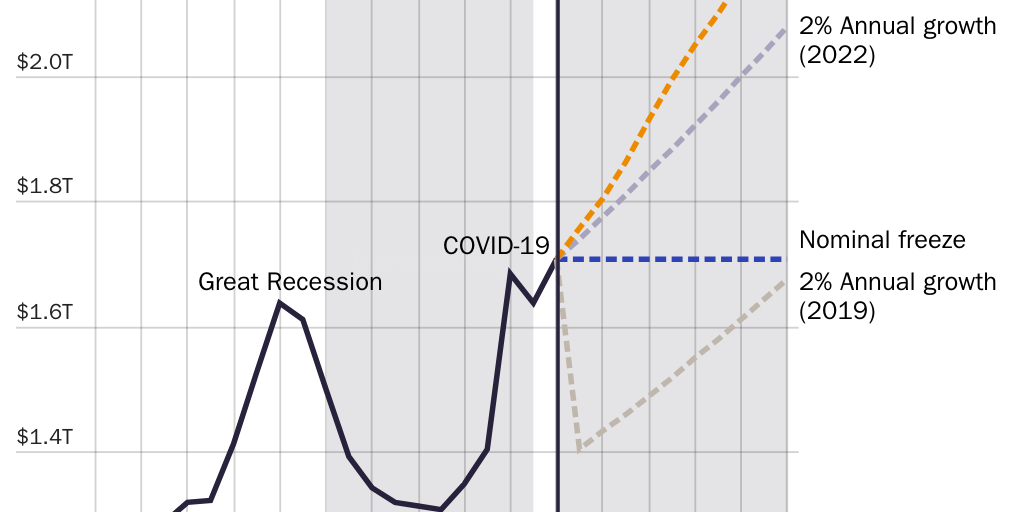

As mentioned above, the Budget Control Act of 2011 capped discretionary spending between FY 2012 and FY 2021 based on top-line levels established in law.21 Although lawmakers renegotiated these levels multiple times, the caps generally limited discretionary spending growth.22 Discretionary spending declined in real terms from 2011 to 2015, then remained flat for another two years before growing by 3 percent and 4 percent, respectively, in 2018 and 2019 (see Figure 3). In 2020, discretionary spending grew sharply in response to the COVID-19 pandemic, increasing by 20 percent from 2019.

Now that the pandemic has ended, members of Congress should return discretionary spending to pre‐pandemic (FY 2019) levels and cap discretionary spending growth at no more than 2 percent annually. Lawmakers running up emergency deficit spending at the height of the COVID-19 pandemic must not establish a higher spending baseline for years to come. Government spending should wind down along with the pandemic.

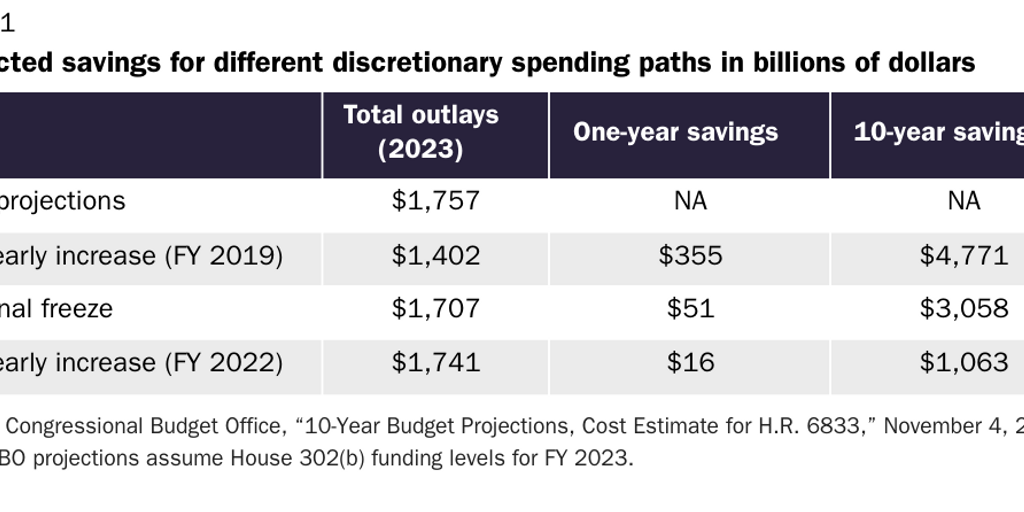

Compared to assumptions by the CBO, a return to real pre‐pandemic discretionary spending and capping discretionary spending at 2 percent from there would save American taxpayers $4.8 trillion over the next 10 years. A more modest proposal to freeze discretionary spending at current levels would save $3 trillion over 10 years. Additionally, a more modest limitation on the growth of discretionary spending to no more than 2 percent based on current levels would save $1 trillion over the same period (Table 1).

Spending limits are critical fiscal tools to encourage budgetary discipline. Imposing transparent resource constraints can urge Congress to prioritize by examining the tradeoffs involved in spending decisions more carefully. Even when lawmakers decide to increase discretionary spending, caps establish the expectation of finding alternative spending offsets. Congress’ desire to increase discretionary spending above the Budget Control Act of 2011 caps was a motivating force behind small reductions in mandatory spending.23

Congress should restore discretionary spending caps and limit discretionary spending growth to no more than 2 percent annually. But first, Congress should cut discretionary spending back to pre-pandemic FY 2019 levels now that the worst of the pandemic and its most serious economic distortions have passed. Congress can achieve the necessary savings by:

- cutting programs like Community Development Block Grants, and reducing federal funding for public schools and local transportation to their pre-pandemic levels, at minimum;24

- eliminating spending that is unnecessary, wasteful, ineffective, or outside the scope of federal government power. Congress can draw on ideas from outside groups, such as the Cato Institute, the Heritage Foundation, the Committee for a Responsible Federal Budget, Citizens Against Government Waste, and the National Taxpayers Union Foundation, as well as the nonpartisan Congressional Budget Office;25 and

- ending unauthorized appropriations.26 Congress should reauthorize those expired programs that continue to serve an essential federal purpose and eliminate all other unauthorized spending.

Congress Should Restore the Earmark Ban

Following a decade-long earmark ban, a Democrat-led Congress brought back earmarks under a new name, “congressionally directed spending,” in 2021. Legislators then stocked up on pork-barrel spending in FY 2022 appropriations bills. According to the GAO, the Consolidated Appropriations Act of 2022 included 4,963 earmarks that spent a total of $9.1 billion.27 From feral swine management to aquarium subsidies to museum and theatre funding to local bike paths, earmarks span the gamut of parochial interests.28

Earmarks are specific spending requested by a member of Congress or a senator on behalf of an entity, state, locality, or congressional district. Earmarks generally bypass statutory or administrative formulas or competitive award processes. Therefore, earmarks more often result in a greater misallocation of resources, with funding going toward projects that are lower priority or that federal taxpayers shouldn’t fund. Well-organized interest and advocacy groups that build strong relationships with congressional offices stand a greater chance of having their earmarks included in appropriations bills. Earmarks encourage rent seeking and the expenditure of scarce resources that could have otherwise gone toward more productive uses in the broader economy.

Earmarking also costs much of congressional staffs’ and legislators’ time. Their time would be better spent learning more about the key drivers of America’s deteriorating fiscal situation and identifying policy proposals to achieve sustainable fiscal balance. Legislators could also spend this time reviewing government programs whose authorizations have expired and work toward passing appropriations bills on time by September 30.

Earmarking distracts from more fundamental governing responsibilities, such as reining in deficit spending and engaging in program oversight. For example, if every member of Congress took full advantage of their allowance for 10 earmarks in a given fiscal year, legislative staff would need to review more than 5,300 earmark requests per year instead of getting the federal government on sustainable fiscal footing.

Proponents of earmarking argue that it helps build bipartisan coalitions that can pass legislation. Kevin Kosar, a senior fellow at the American Enterprise Institute, and Zachary Courser, a visiting assistant professor of government at Claremont McKenna College, make the case that “the earmark moratorium weakened the House of Representatives’ capacity to coalesce majorities to enact legislation.“29 That may be true, but not all legislation that secures majority support is good. Congressional leadership has leveraged earmarks to coalesce majorities for more spending, not less.

Other proponents argue that banning earmarks does not work but merely moves the practice behind closed doors. John Hudak, deputy director of the Center for Effective Public Management and a senior fellow in governance studies at the Brookings Institute, writes that “earmarks did not disappear with the so‐called ‘earmarks ban’ in 2011; it simply transferred the behavior to the executive branch or made them more secretive within the legislative branch.“30 Hudak is referring to letter marking or phone marking, whereby legislators submit specific funding requests directly to agency personnel. Naturally, bureaucrats are often eager to comply, especially when receiving such requests from members of appropriations committees who determine their agency’s funding levels.

Whether earmarks are allowed in congressional spending bills does not impede lawmakers’ ability to submit spending requests over the phone or in emails. In the Yale Journal of Regulation, James Dawson and Sam Kleiner further argue that letter and phone marking violate several legal rules.31 The practice also directly contradicts executive guidance, such as Executive Order 13457, which states:

For appropriations laws and other legislation enacted after the date of this order, executive agencies should not commit, obligate, or expend funds on the basis of earmarks included in any non-statutory source, including requests in reports of committees of the Congress or other congressional documents, or communications from or on behalf of Members of Congress, or any other non-statutory source, except when required by law or when an agency has itself determined a project, program, activity, grant, or other transaction to have merit under statutory criteria or other merit-based decisionmaking.32

Rather than formalizing the process through which Congress may move parochial concerns by allowing earmarking, Congress should find more effective ways of enforcing spending guidelines in current law and by executive order.

Earmark proponents are correct about one thing: state and local constituents have a better understanding of where project funding will best help. That’s one reason Congress should devolve more responsibilities back to states and localities to address their own needs and priorities without Washington as their intermediary. Earmarking is the wrong way to ensure that government spending reflects local priorities.

Congress Should Avoid New Stimulus Spending

The United States could confront a recession this year as Federal Reserve interest rate increases to reduce inflation may cause a temporary downturn in economic growth. Should growth turn significantly negative for two or more quarters in a row, members of Congress may be tempted to resort to fiscal stimulus to boost demand.

Additional fiscal stimulus would be misguided for at least two reasons. First, fiscal stimulus would undermine the Federal Reserve’s efforts to fight inflation, especially if fiscal stimulus would take the form of new cash payments or enhanced unemployment benefits. Those are the same demand-boosting subsidies the federal government pursued during the COVID-19 pandemic that have contributed to higher inflation today. Second, the government cannot spend its way into national prosperity. Higher government spending today comes with future costs from the likely displacement of private economic activities by government-directed projects, a misallocation of capital, greater debt, reduced incentives to work and invest, and the likelihood of higher future taxes.33

Conclusion

The 118th Congress should commit to a credible fiscal stabilization path that controls the growth in the debt as a percentage of GDP. It should focus on reforming entitlement programs, reducing and capping discretionary spending, and banning earmarks. Following excessive spending during the COVID-19 pandemic that contributed to inflation reaching a 40‐year high, the 118th Congress should shift gears by pursuing deficit reduction that enables economic growth and complements the deflationary actions of the Federal Reserve. Spending-based deficit reduction, especially targeted at social and entitlement programs, is most effective at sustainably reducing deficits and the growth in the debt as a percentage of GDP.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.