Back in March, President Trump issued an executive order targeting, among other things, the Treasury’s Community Development Financial Institutions (CDFI) Fund, calling for its elimination “to the maximum extent consistent with applicable law.”1 The CDFI Fund, founded in 1994, provides tax credits, grants, and bonds to eligible institutions, including banks and nonprofits. The administration has received bipartisan pushback for issuing the executive order, with CDFI Fund proponents claiming that small businesses and low-income communities would suffer a blow in the CDFI Fund’s absence.2

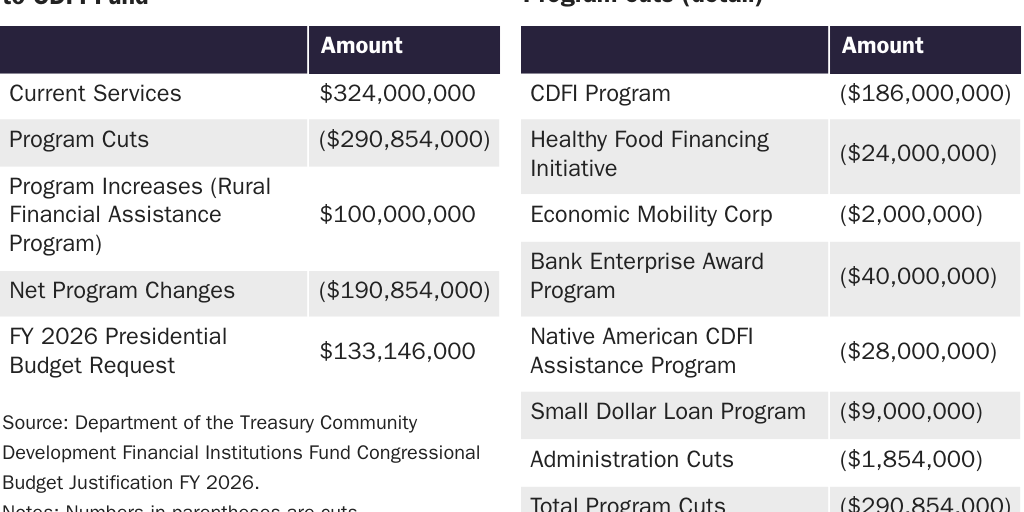

More recently, the White House’s discretionary budget request outlined a net $191 million cut to the discretionary funding for the CDFI Fund (Table 1).3 In 2023, the CDFI Fund represented a budget cost of $2.1 billion per year. Of this total, 81 percent of funding ($1.7 billion) can be attributed to a tax credit program, while the remaining $391 million consists of various discretionary grant programs.4 Essentially, the CDFI Fund is a corporate welfare program for real estate developers, and it should be eliminated.

Basics of the CDFI Fund

The Riegle Community Development and Regulatory Improvement Act of 1994 established the legal definition of CDFIs and created the CDFI Fund, an independent government corporation.5 The CDFI Fund was then reorganized as part of the US Treasury in a 1995 budget reconciliation bill, though it retained its original name.6

As of September 2024, there were 1,426 CDFIs, including both for-profit depository institutions and nonprofit institutions.7 In short, the CDFI Fund provides tax credits, grants, and bonds to various types of eligible entities. These entities, in turn, act as intermediaries for funds to be disbursed to pay for services (including general business expenses) and to subsidize development projects through grants and loans. According to the US Department of the Treasury, the mission of the CDFI Fund is to “expand economic opportunity for underserved people and communities by supporting the growth and capacity of a national network of community development lenders, investors, and financial service providers.”8

By far, the largest component of the CDFI Fund is the New Markets Tax Credit (NMTC), which, in recent years, has totaled over $1.5 billion annually.9 The NMTC was established by the Community Renewal Tax Relief Act of 2000 and provides tax credits to Community Development Entities (CDEs), which serve as tax credit intermediaries to investors.10 CDEs are very similar to CDFIs, and many organizations are cross-certified; strictly speaking, however, they are not the same thing, because the CDE designation specifically refers to NMTC intermediaries, while the CDFI designation refers to financial institutions that are eligible for other CDFI Fund programs (primarily grants).11 The NMTC was set to expire at the end of 2025, but Congress has permanently extended it.12

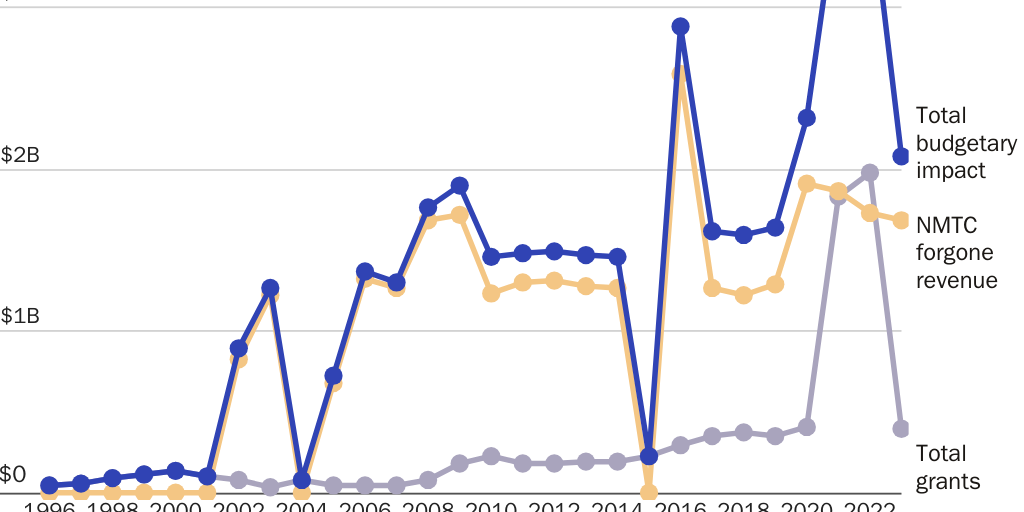

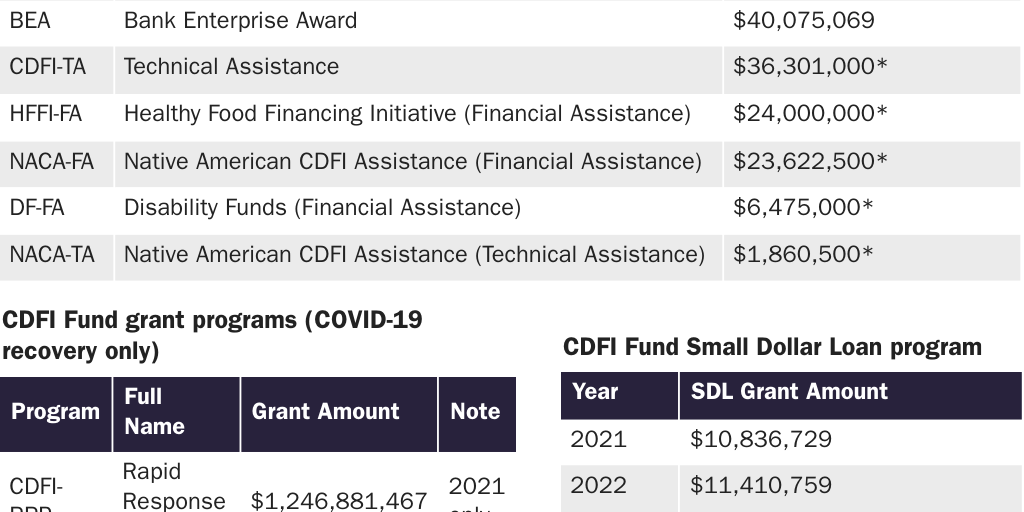

The CDFI Fund issues several types of grants. In recent years, the typical annual grant cost to the budget was around $400 million, with costs in 2021 and 2022 being noticeable exceptions because of COVID-19 relief funds. In 2021, a total of $1.25 billion’s worth of grants was issued to 859 CDFIs as part of the CDFI Rapid Response Program (RRP).13 In 2022, the CDFI Equitable Response Program (ERP) disbursed $1.74 billion in grants to 601 CDFIs.14 In total, 988 CDFIs received funding from at least one of these two COVID-era programs, and 472 CDFIs received funding from both RRP and ERP. As Figure 1 demonstrates, aside from these two years, the grants generally make up less than 25 percent of the total CDFI Fund budget impact.

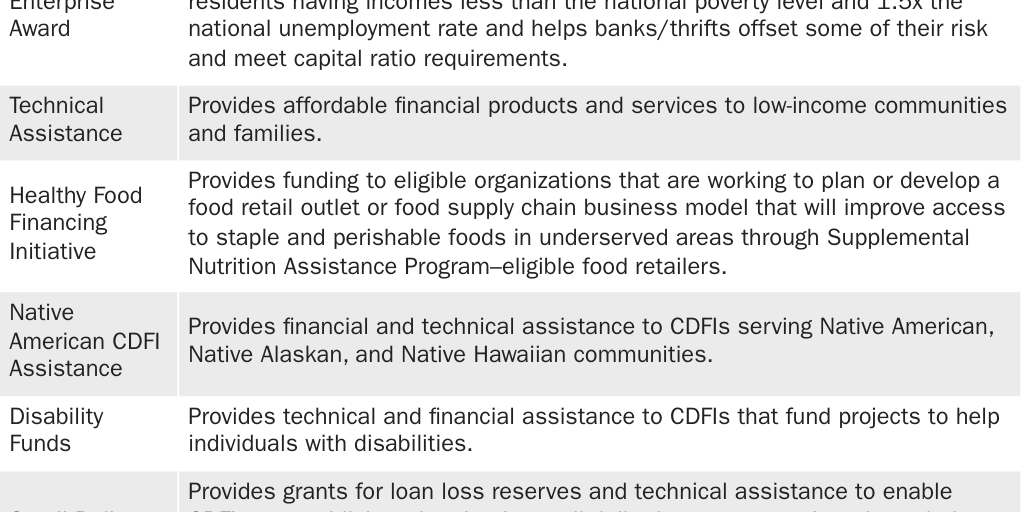

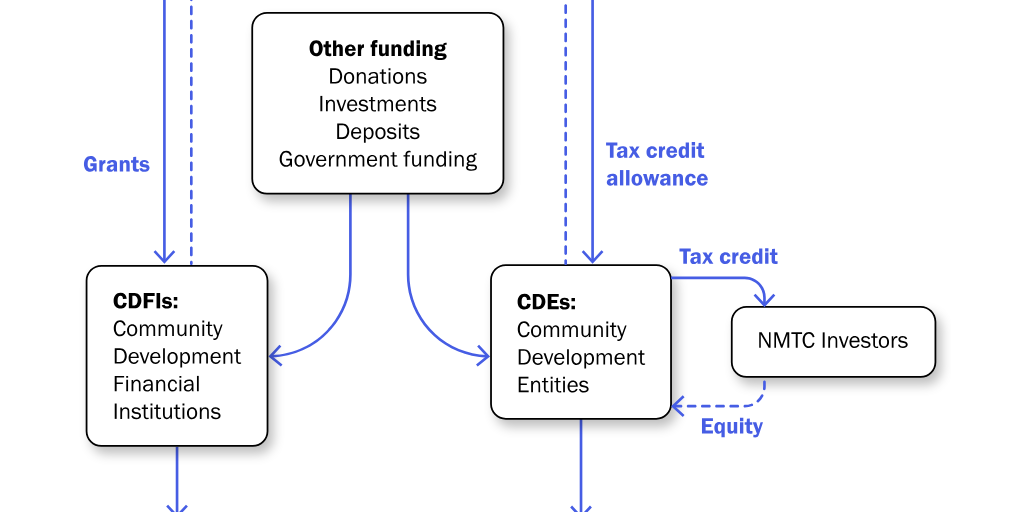

Aside from these two large, one-time programs, most of the grants to CDFIs are smaller and are awarded through the Capital Magnet Fund (CMF) program and the Financial Assistance (FA) program. In 2024, $246 million was disbursed through the CMF program, primarily for affordable housing developments, while $150 million was disbursed through the FA program, primarily to enhance CDFI balance sheets. Separately, various other CDFI Fund grant programs disbursed a total of $150 million to CDFIs in 2024. The CDFI Fund grant program generally has less impact on the budget than the NMTC, but during the COVID-19 pandemic, grant spending ballooned into the billions. Table 2 provides recent budget data on CDFI Fund grant programs; Table 3 provides descriptions of those programs; and Figure 2 provides a graphic depiction of the CDFI Fund’s grant and tax credit mechanisms.15

Overlapping Missions

Research shows that the CDFIs do lend primarily to underserved markets, including low-income and minority borrowers in distressed areas.16 However, research demonstrating a direct link between the CDFI Fund (or CDFIs) and expanded economic opportunity for underserved people and communities is extremely limited—if it exists at all. Critics further charge that many projects for “community development” encourage developer rent-seeking for projects that evidence suggests would have been undertaken anyway.17 Critics also point out that most geographic locations, not just low-income areas, are eligible for CDFI Fund dollars or tax credits and that a wide range of government programs already exist to bolster low-income borrowing and community development.18

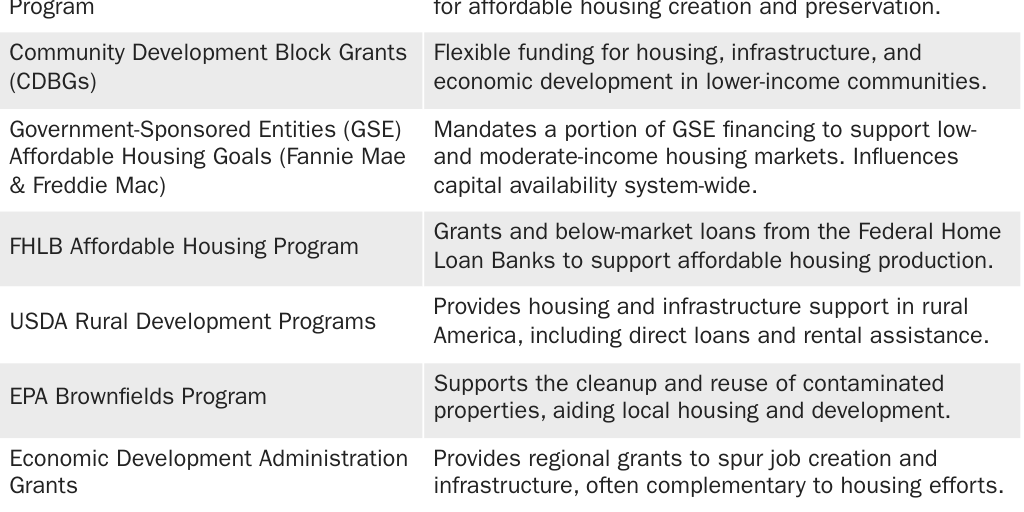

Supporters claim that tax credits and grants are necessary to enhance the financial sector’s ability to spur community development. However, even the CDFI Fund’s own research has not demonstrated any improvement in neighborhood conditions as a result of “concentrated and sustained” CDFI lending.19 Furthermore, as Table 4 shows, many other government programs exist with the same type of mission as the CDFI Fund, resulting in many redundant programs, all designed to improve low-income neighborhoods.

One example of a government program intended for similar purposes as the CDFI Fund is the Opportunity Zones initiative, which, incidentally, Congress made permanent in 2025.20 Like many similar programs, the primary beneficiaries of Opportunity Zones are wealthy households, and the jobs related to these projects typically flow to people from outside the community.21 Moreover, according to a 2014 Government Accountability Office report, 62 percent of NMTC projects between 2010 and 2012 received additional federal, state, or local government assistance, while 33 percent received additional federal funding (tax credits, tax-exempt bonds, grants, or loans).22

Separately, the Community Reinvestment Act (CRA) of 1977 requires federal banking regulators to encourage banks to “help meet the credit needs of the local communities in which they are chartered consistent with the safe and sound operation of such institutions.”23 The CRA forces depository institutions to engage in low- and moderate-income household and area lending, pushing many banks to invest in CDFIs for the express purpose of satisfying their obligations under the CRA. Thus, the CRA overlaps with the CDFI Fund’s agenda in a way that leads to more banks investing in CDFIs than likely would otherwise. Therefore, even if Congress eliminated the CDFI Fund, other legislative mandates would still require lending in low-income/underserved areas. In either case, it is a mistake to strong-arm investment into preferred markets or areas, regardless of whether the government is using carrots (i.e., the CDFI Fund) or sticks (i.e., the CRA).

Who Benefits?

Despite claiming to help fund projects in low-income areas, the CDFI Fund has mainly benefited financial institutions, which are able to stack tax credits or grants from the CDFI Fund on top of other sources of public funding for the same projects. Furthermore, projects in virtually all congressional districts have census tracts that are eligible for CDFI Fund money. Indeed, nearly half of US census tracts are eligible for NMTC alone.24 CDFI Fund grants are politically popular on both sides of the aisle, since they can be used to divert federal funds to local constituencies, whether urban or rural. While the White House’s budget proposal suggests cutting the CDFI Fund grant program as it currently exists and diverting funds to primarily rural recipients, Congress seems unlikely to eliminate the CDFI Fund. On one hand, it is very easy to expand the grant program for any “emergency” needs, as was seen during the COVID-19 pandemic. On the other hand, grant programs can be used to effectively bolster the support of institutions and beneficiaries, as well as reward political allies and preferred groups.

CDFI Fund grant programs benefit entire institutions rather than specific project recipients, so it can be difficult to analyze their impact. However, since the NMTC program directly funds individual projects, it can be more informative to investigate NMTC-backed projects.25 As a 2014 report from the late Senator Tom Coburn documented, many of these projects would be best described as corporate welfare.26

One example from the report is the NMTC allocation to help fund an expansion of the Atlanta Aquarium’s now-closed AT&T Dolphin Tales exhibit. A total of $40 million in NMTC allotments was secured by Imagine Downtown, Inc. (now Atlanta Emerging Markets, Inc.), a CDE fully owned by Invest Atlanta, the official economic development authority for the City of Atlanta. According to the president of Imagine Downtown, the tax credit was unnecessary as this development would have happened anyway. The tax credit was subsequently sold to Wells Fargo and SunTrust banks.27

Another questionable funding choice was the NMTC-financed St. Louis Trolley, which received $43 million in federal funding, including $15 million from the NMTC. The projected total cost of the project was $43 million, almost fully covered by federal funding.28 However, the total escalated to $51 million, putting area taxpayers on the hook for the remainder.29 The project has turned out to be a boondoggle, falling far short of expected revenue and costing $160.58 per passenger, making it much cheaper to hire Uber Black rides for passengers rather than continue the service.30

In 2018, Vidalia Denim received $18.5 million from the NMTC for the construction of a manufacturing facility in Vidalia, Louisiana, with Chase Bank as the NMTC investor.31 The company also received an $8 million grant from the City of Vidalia, a $25 million US Department of Agriculture Business and Industry Guaranteed loan from Jefferson Financial Federal Credit Union to purchase, renovate, and equip the textile facility, and a $5 million Small Business Administration loan from Greater Nevada Credit Union.32 As of February 2025, the company faces public auction as it owes $32.5 million in principal, interest, and late charges to the previously mentioned credit unions.33

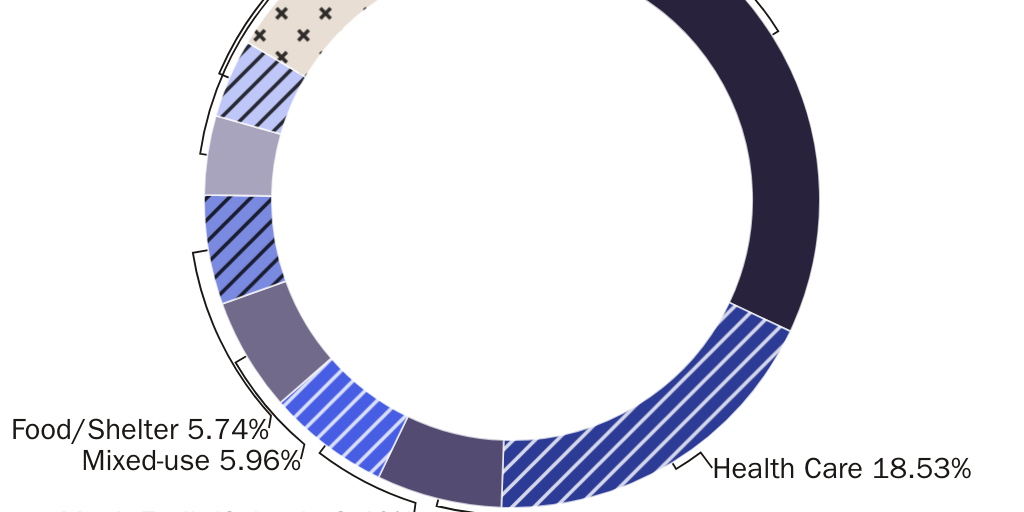

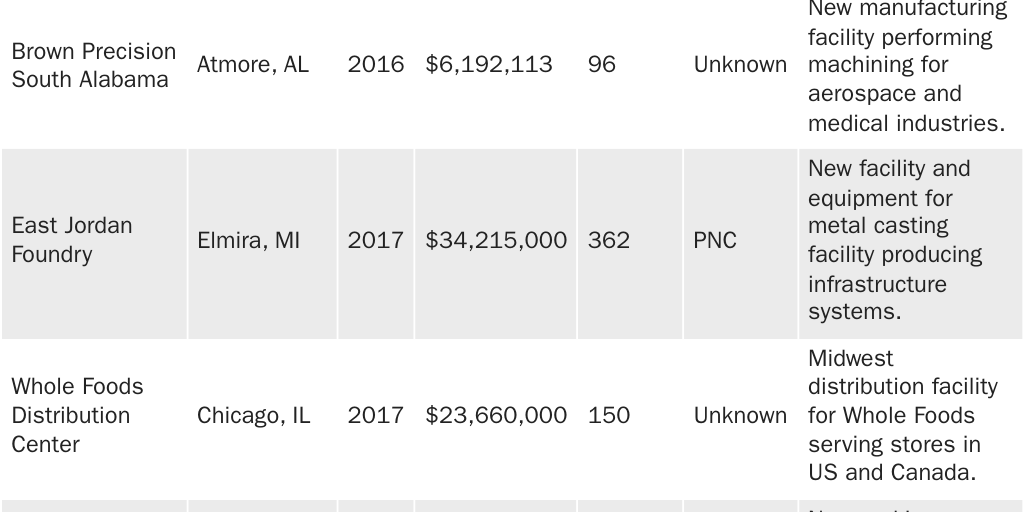

These stories represent just a few examples; the NMTC Coalition, a lobbying organization, lists NMTC-funded projects and provides information about program costs, NMTC allocations, and “impact” metrics, such as construction and full-time-equivalent jobs arising from the projects.34 In recent years, the largest single project type has been manufacturing, representing nearly one-third of all NMTC allocation funds between 2022 and 2024. The second largest category is health care, representing nearly 19 percent of NMTC funding. The remaining half consists of nonprofit hubs, municipal facilities, schools, mixed-use developments, food and shelter, arts and culture, and other categories. Figure 3 contains a breakdown of NMTC allocations by project type, and Table 5 shows more project examples.

As our Cato colleagues have stated, tax credit programs receive support from Republicans by virtue of their status as tax cuts, and they receive support from Democrats because they act as welfare.35 In much the same way, the NMTC, the largest budgetary component of the CDFI Fund, receives minimal pushback from legislators of either political party. Tax credits such as these have diverse coalitions of beneficiary supporters, ranging from political action groups to financial institutions, developers, and other for-profit firms. However, they also often subsidize projects that would have been undertaken anyway.

Some proponents claim that NMTC-financed projects increase tax revenues more than the NMTC incurs forgone revenue, packaging the claim as the NMTC delivering a strong “return on investment” to taxpayer dollars.36 But this line of thinking falls flat when considering the two possible situations that can arise from an NMTC-financed project: If the project was going to be undertaken anyway (such as in the case of the Atlanta Aquarium), the tax credit produces a net reduction in tax revenue. On the flip side, if the project appears unprofitable to unsubsidized investors, it is likely to be unprofitable and could become a net drain on public funds (potentially on local coffers, such as in the case of the St. Louis Trolley).

Conclusion

With a litany of existing government programs intended specifically for community development purposes, the CDFI Fund is unnecessary by virtue of its redundancy. Moreover, many of the development projects funded through the CDFI Fund would occur even in the absence of government support. While it would be wise to cut CDFI Fund grant programs and let the NMTC expire, it would be even better to eliminate the CDFI Fund entirely, such that it cannot be massively expanded under guise of emergency. Private investors are better stewards of their own money than Treasury bureaucrats, and fiscal responsibility should be sought by cutting spending, not gambling on developments with public funds. Finally, if Congress views taxes as a hindrance to investment, then it should lower taxes in general.

The authors would like to thank Christian Kruse and Grace Beatty for their assistance on this project.

About the Authors

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.