Pictured left to right: Romina Boccia, Adam Michel, Dominik Lett, and Michael Cannon.

On December 11, the Cato Institute hosted a Hill briefing on affordability. I was joined by my colleagues Romina Boccia, Adam Michel, and Michael Cannon to discuss a reality that most politicians in Washington would prefer to ignore: deficit spending drives up prices and reduces earnings.

The root of today’s “affordability crisis” is the fiscal crisis.

The same massive deficits driven by automatic entitlement spending that politicians on both sides of the aisle refuse to address actively make your life more unaffordable.

In the short run, federal deficit spending increases aggregate demand and alters inflation expectations, thereby raising prices for goods and services. At the same time, high levels of federal debt reduce incomes and productivity by crowding out private capital and placing upward pressure on interest rates.

The result is a triple whammy for Americans: higher prices at the store, higher borrowing costs for a home, car, or business, and reduced long-term income expectations.

Americans’ inflation frustrations are part and parcel with the pandemic spending spree.

Between 2020 and 2021, Congress authorized more than $6 trillion in stimulus spending. This unprecedentedly large federal response was both ineffective and completely divorced from economic reality.

By early 2021, the Congressional Budget Office estimated that the annual “output gap”—the difference between actual economic activity and potential output—was approximately $380 billion. Despite having already injected $4 trillion into the US economy, Congress chose to pursue an additional $2 trillion in stimulus through the American Rescue Plan Act (ARPA).

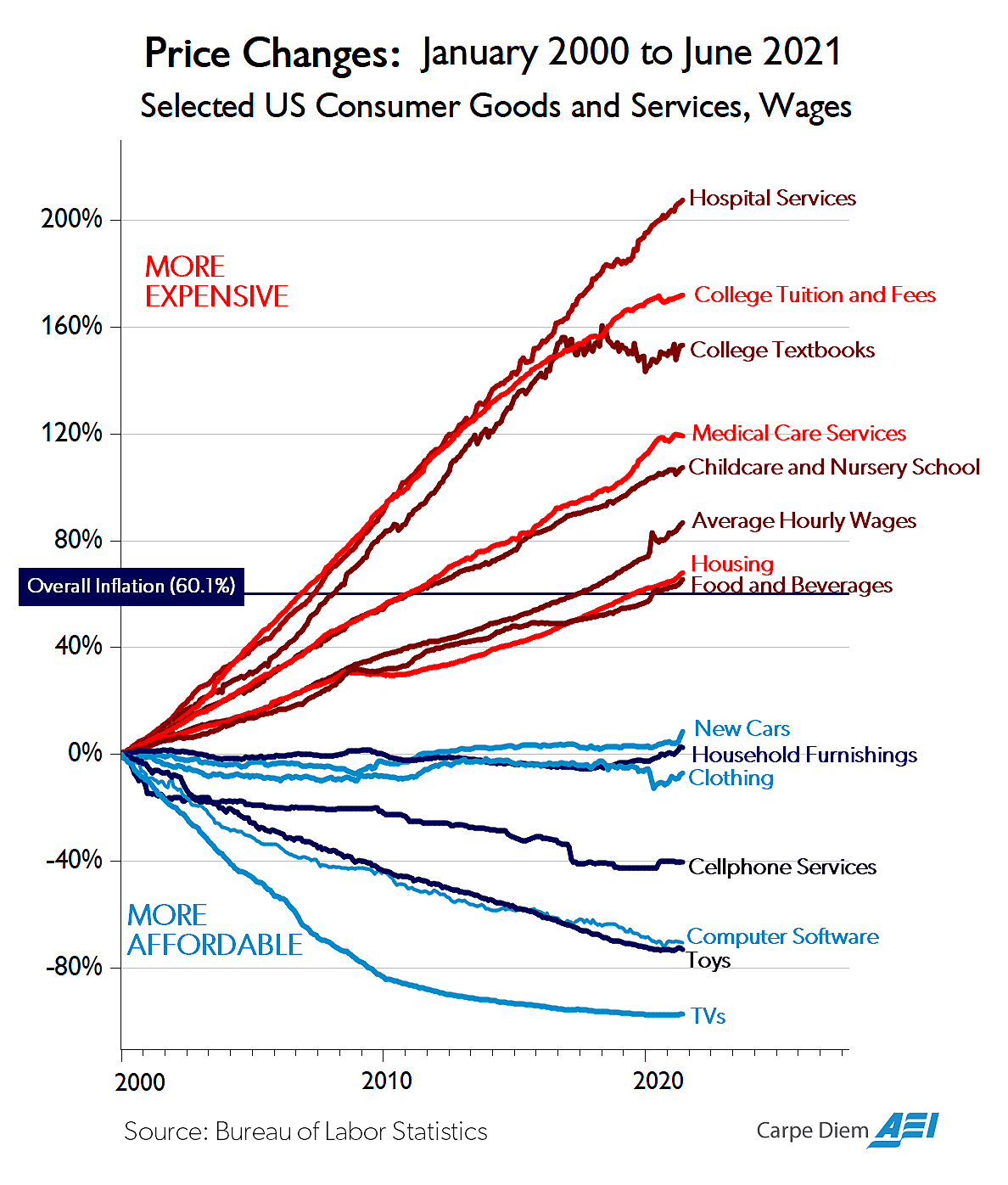

Congress successfully engineered the perfect inflation scenario. They reacted to a supply shock (lockdowns and supply chain disruptions) with a massive demand shock (stimulus checks and new spending). Simply put, there was too much money chasing too little output. By mid-2022, inflation hit 40-year highs (see the graph below).

Worse yet, the federal deficit has yet to return to pre-pandemic levels. In 2025, the deficit sits at nearly 6 percent of GDP. We have effectively normalized emergency-level borrowing during peacetime.

This persistent fiscal imbalance, driven by emergency spending and entitlement programs, is a major driver of today’s perceived affordability crisis. When the government borrows at this scale and frequency, interest rates rise and income growth stalls, making life less affordable for everyone.

The alternative to shoveling more money into the pit is supply-side reform.

One of the key themes Adam Michel highlighted is the need to distinguish between policies that help affordability and those that hurt it.

The demand-side stimulus favored by some policymakers injects more money into the economy without increasing supply. Most of the time, these subsidies appear as cash for consumers to purchase goods—such as student or housing loans—which drives up the price. To the extent some subsidy beneficiaries may see lower sticker prices, like with Obamacare, the true cost of the good or service hasn’t actually gone down. Instead, the cost has just been shifted from beneficiaries to present and future taxpayers.

By contrast, supply-side tax cuts and deregulation are generally deflationary. Take the 2017 Tax Cuts and Jobs Act. By increasing the economy’s productive capacity, the US can produce more goods and services to meet demand. Costs come down, incomes rise, and affordability improves.

The chart below effectively illustrates the overall trend. Markets with the highest levels of government regulation and subsidies, across health care and education, have experienced the largest price increases. Meanwhile, markets with relatively fewer government-imposed supply constraints and subsidies have experienced price declines.

Subsidies are driving healthcare costs higher.

Perhaps nowhere is the government’s role in driving up costs clearer than in healthcare.

As Michael Cannon explained, the US spends more on healthcare per capita than any other country. Some of that spending is there for good reasons, including higher-quality care. However, a lot of the high cost of health care is driven by government policy. FDA regulations, licensing rules, and the tax exclusion for employer-sponsored health insurance distort the market and restrict supply.

Medicare, Medicaid, and the inaptly named Affordable Care Act exacerbate the problem by subsidizing demand without increasing supply. The result is a vicious cycle. Subsidies contribute to higher prices, consumers get frustrated with high costs, politicians react with more subsidies, and the cycle continues.

To actually lower costs, Cannon suggested that Congress let the enhanced Obamacare subsidies expire and prioritize reforms that stimulate competition and empower consumers. A few examples include allowing individuals and employers to purchase Obamacare-exempt health plans (short-term, limited-duration insurance) and expanding Health Savings Accounts (HSAs).

Conclusion

If there’s one clear lesson from the pandemic spending spree, it is that affordability is not something Congress can deliver with a deficit-financed check. Democrats attempted to do so with the American Rescue Plan Act (both with enhanced Obamacare subsidies and stimulus checks). Prices rose across the board, and voters punished incumbent politicians at the ballot box.

Given America’s dire fiscal environment and its impact on prices and incomes, getting government out of the way via supply-side tweaks will be a necessary but insufficient fix alone. To truly deliver on affordability, Congress needs to hunker down and slow the growth of health care and Social Security spending.

The sooner Washington stops stealing from our future to subsidize the present, the better.