In the Republican debate last night, former Gov. Mike Huckabee of Arkansas criticized calls for Social Security reform, saying “people paid their money. They expect to have it,” and that the country needs to honor its promises to seniors. There are problems with this line of argument: the Social Security payroll taxes a person pays are not tied to the benefits they receive in a legal sense, and the ‘promises’ made by Social Security are, and always have been, subject to change.

Congress has had the authority to alter Social Security since its inception. Section 1104 of The Social Security Act of 1935 explicitly says: “The right to alter, amend, or repeal any provision of this Act is hereby reserved to the Congress.”

Not only does Congress have the right to make changes, it has done so multiple times in the past. Sometimes these changes are smaller things, like a technical correction to the indexation formula, but there were also larger reforms that were part of attempts to address the programs solvency issues.

The Supreme Court revisited the issue of Social Security’s promises in Flemming v. Nestor, in which Nestor, who had paid into Social Security for 19 years and begun to receive benefits, was then deported for previous ties to the Communist Party. Nestor tried to appeal the termination of his benefits, citing his previous contributions, but the Supreme Court upheld it, saying:

To engraft upon the Social Security system a concept of ‘accrued property rights’ would deprive it of the flexibility and boldness in adjustment to ever changing conditions which it demands… It is apparent that the non-contractual interest of an employee covered by the [Social Security] Act cannot be soundly analogized to that of the holder of an annuity, whose right to benefits is bottomed on his contractual premium payments.

The other aspect Huckabee touches on is the link between the taxes paid in and the benefits a person ultimately receives, implying that a worker’s contributions are kept in some kind of silo to be paid out to them at a later date. As another Supreme Court case found, this is not true.

In Helvering v. Davis (1937)the Court held that Social Security was not a contributory insurance program in the sense that “[t]he proceeds of both the employee and employer taxes are to be paid into the Treasury like any other internal revenue generally, and are not earmarked in any way.” Despite how Huckabee and his fellow defenders of the status quo describe the program, the payroll tax payments a person pays into Social Security have no direct link to the benefits that they receive in a legal sense: they are subject to future changes made by Congress and dependent on the program having sufficient revenue.

Huckabee doesn’t need to familiarize himself with these decades-old Supreme Court cases or the Social Security Act to be able to understand the problems with his invocation of the program’s ‘promises’. Anyone, including Huckabee, can see this for themselves in the Social Security Statement that the Social Security Administration periodically sends to workers:

Your estimated benefits are based on current law. Congress has made changes to the law in the past and can do so at any time.

The ‘promises’ with Social Security always came with an asterisk, and beneficiaries are not entitled to a certain amount because they have contributed payroll taxes. In the past the law has been altered to change the deal facing beneficiaries, and there will undoubtedly have to be more changes in the future if Social Security is to remain viable. If we maintain the status quo and do nothing, benefits will have to cut by 23 percent across the board when the combined trust fund is exhausted in 2034. There can be disagreements about the best way to reform Social Security, but when it is facing trillions in unfunded obligations and the certainty of drastic cuts in the future absent reform, doing nothing is not a feasible option.

Cato at Liberty

Cato at Liberty

Social Security

A recent report from the Social Security Advisory Board’s Technical Panel found that the 75-year shortfall could be 28 percent (roughly $2.6 trillion) larger than the estimate in this year’s Trustees Report due to changes in some of the underlying technical assumptions. This disparity is more the product of the difficulties related to projecting the trajectory of a program as large and complicated as Social Security so far into the future, with the chair of the Technical Panel taking pains to reiterate that “the methods and assumptions used by the Social Security actuaries and Trustees are reasonable.” Even so, the report reveals the uncertainty related to the long-term projections for Social Security, with relatively small changes to some of the underlying assumptions significantly changing the program’s financial solvency outlook. Social Security is the largest government program in the world, and changes in its fiscal outlook could have a large impact on the government’s overall finances.

The changes in the Technical Panel report that would have the largest impact are concentrated in a few variables:

- Higher fertility rate

- Higher life expectancy

- Higher interest rates

Other changes to inflation and real earnings growth rate assumptions have a small negative impact, while changes to immigration assumptions slightly improve the program’s financial picture. Some of the changes reflect developments that are good overall but have a negative impact on Social Security’s finances, like higher life expectancy.

Some of the panel’s recommendations focus on making the methodology of the Trustees’ Report more transparent and the degree of uncertainty more clear. While it’s possible that unforeseen changes to underlying variables like the fertility rate could improve the program’s financial outlook, it is much more likely that the trillions in unfunded obligations published in the Annual Trustees’ Report understate the shortfall, if anything.

To some extent we don’t know what Social Security’s long-run shortfall is, but we do know that there will have to be significant reforms to make the program solvent, and the longer these changes are delayed the bigger they’ll need to be. Whether it is raising payroll tax rates or cutting benefits, delaying reform only makes the needed changes more severe.

Percent Change Needed for 75-Year Solvency

Source: Social Security Administration, The 2015 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds, July 2015, p. 25.

One of the goals Social Security is to remove some degree of uncertainty related to life in old age, but this new report confirms that a high degree of uncertainty remains, both for the program’s overall solvency and for individual workers. Younger workers already get a worse deal than previous generations due to demographic change and the program’s structure. Even more troubling, they can’t know how much worse their deal will become as benefits are cut or taxes are increased in the future to try to address this shortfall.

One option that could remedy some of these inherent problems would be to allow workers, especially young workers, to divert some of their payroll taxes to individual accounts. Cato has explored this issue in the past. Chile, for example, has an elderly extreme poverty rate of 1.6 percent, and pension funds have seen a real annual return of 8.6 percent from 1981 to 2013. The United States should heed some of these lessons. Other countries, especially those in South America, have successfully introduced reforms along these lines.

Related Tags

A recent Gallup poll finds that government employees are considerably more satisfied than their private sector counterparts with their compensation fringe benefits–namely government retirement plans (+25), health insurance benefits (+23), and vacation time (+17).

The poll compared satisfaction with 13 different job aspects for both government and nongovernment employees, ranging from stress on the job, flexibility, recognition, salary, relations with coworkers and bosses, etc. In 9 of the 13 characteristics, government and private sector workers reported similar levels of satisfaction (all above 60%) with job stress, recognition, flexibility, safety, salary, hours, promotion opportunities and job security.

However, 82 percent of government workers reported being completely or somewhat satisfied with their retirement plan compared to 57 percent of their private sector peers, a +25 point difference. Government workers typically receive defined benefit pension plans, which typically offer employees a guaranteed monthly amount in retirement. In contrast, private sector workers’ retirement plans are not guaranteed but based on the amount they save, their employer contributes, and investment returns.

Again, 80% of government workers say they are satisfied with their health insurance benefits compared to 57% of private sector workers (a +23 point difference). Gallup reports that government worker health insurance plans typically require lower out-of-pocket costs than found in the private sector, which may explain these differences.

In addition, fully 9 in 10 government employees are satisfied with their vacation time compared to 74% of private sector employees (a +17 point difference).

These stark disparities in satisfaction with retirement and health insurance benefits and vacation between government and private sector workers may indicate that government workers receive “above market” fringe benefits, meaning they receive more than what the market would pay. The fact that government and non-government workers report similar satisfaction with their salaries, but significant differences in non-salary perks raises the question if government employee compensation packages should be adjusted to match market offerings.

Research Assistant Nick Zaiac contributed to this post.

For more public opinion analysis sign up here for Cato’s regular digest of Public Opinion Insights.

“The godfather of inequality research,” is how The Economist describes septuagenarian British economist Anthony Atkinson. A frequent co-author with Thomas Piketty and Joe Stiglitz, Sir Atkinson has written a book about inequality which a New York Times reviewer described as a “flurry of largely recycled policy proposals.” Inequality: What can be done? is all about “unapologetic support for aggressive government intervention,” says The Economist, and “a throwback to the 1960s and 1970s.”

There is no need to buy the book, because the following summary – “15 Proposals from Tony Atkinson’s book ‘Inequality: What can be done?’ – is more than enough. Each Proposal is in the author’s own words, but followed by my own view of Problems with those plans. [I skip Proposals 9–11, which are just inflated versions of policies similar to those in the U.S. – the earned income credit, estate & gift tax, and property tax.]

Proposal 1: The direction of technological change should be an explicit concern of policy-makers, encouraging innovation in a form that increases the employability of workers and emphasizes the human dimension of service provision.

Problem 1: To invite political officials to obstruct labor-saving technology or to encourage (subsidize) employment growth at the expense of output growth are plans to depress the growth of real output per worker (productivity) and therefore depress real income per worker.

Proposal 2: Public policy should aim at a proper balance of power among stakeholders, and to this end should

(a) introduce an explicitly distributional dimension into competition policy;

(b) ensure a legal framework that allows trade unions to represent workers on level terms; and

(c) establish, where it does not already exist, a Social and Economic Council involving the social partners and other nongovernmental bodies.

Problem 2: The first proposal (2a) hopes to turn antitrust lawsuits into a device for reducing profits, apparently based on a zero-sum notion that smaller profits ensure larger wages. The second proposal (2b) insinuates that current law is biased against unions in unspecified ways. The third (2c) endorses a Social and Economic Council composed of private interest groups. Such councils already exist at the Arab League and U.N., apparently as a pretext for conferences.

Proposal 3: The government should adopt an explicit target for preventing and reducing unemployment and underpin this ambition by offering guaranteed public employment at the minimum wage to those who seek it.

Problem 3: Guaranteed public employment at the minimum wage would have to be financed by taxes, which reduce employment in the private sector. If the minimum wage were both high and binding, this could shift a large and growing share of employment away from production of marketable products into provision of “free” government services of unknown value to consumers. By creating a growing constituency for large increases in the minimum wages, guaranteed tax-financed public jobs could displace or “crowd out” more and more private employment. In the U.S., the legal minimum of $7.25 an hour is not binding; it applies only to certain formal and visible forms of employment. The U.S. Bureau of Labor Statistics reports that in 2014 there were only 550,000 people over the age of 25 earning the federal minimum wage of $7.25 an hour, but 999,000 earning less than that minimum wage.

Proposal 4: There should be a national pay policy, consisting of two elements: a statutory minimum wage set at a living wage, and a code of practice for pay above the minimum, agreed as part of a “national conversation” involving the Social and Economic Council.

Problem 4: How could the proposed overturning of private labor contracts by an unelected “Council” be consistent with any concept of political or economic liberty? This comes frighteningly close to saying governments (e.g., Nixon’s wage controls) and/or non-governmental interest groups (e.g., Medieval guilds) can and should dictate to workers how much they should charge for their work, and how much employers must offer. Yet inequality is famously low in countries with no minimum wage, such as Sweden, Austria, Denmark and (until 2015) Germany. And inequality is very high in U.S. cities with a high minimum wage, such as San Francisco. The concept of nationwide “living wage” is arbitrary gibberish, since such a goal cannot possibly be the same for an Alabama teen living with parents as it is for a single mother in Manhattan with four children.

Proposal 5: The government should offer via national savings bonds a guaranteed positive real rate of interest on savings, with a maximum holding per person.

Problem 5: U.S. Treasury inflation-protected securities (TIPS) guarantee a positive real rate if held to maturity, as do similar bonds in Europe. There could be no maximum holding of such bonds unless savers were somehow prohibited from selling their securities (which would make them illiquid and undesirable). If Atkinson means to offer a higher real return than the market provides then the proposal would misallocate capital and increase government (taxpayer) debt.

Proposal 6: There should be a capital endowment (minimum inheritance) paid to all at adulthood.

Problem 6: This proposal would everyone a check for about $15,000 upon reaching adulthood, described as “capital” yet likely used for consumption. This indiscriminate transfer payment is to be financed by a 65% death tax. Higher tax rates on the capital accumulation of older savers to pay for large subsidies to the consumption of young consumers would, as Joe Stiglitz explained in 1978, reduce productivity and weal wages by reducing the ratio of capital to labor.

Proposal 7: A public Investment Authority should be created, operating a sovereign wealth fund with the aim of building up the net worth of the state by holding investments in companies and in property.

Problem 7: Atkinson is proposing to emulate Arabian princedoms, China and other autocratic states by investing taxpayer funds (like the U.S. Social Security trust fund) in private equites and real estate. Malaysia’s wealth fund, for example, is the majority shareholder in Malaysian Airlines, whose stock recently fell 90%. Governments with budget deficits would be investing borrowed funds in stock markets, which is as speculative as individuals buying stocks on margin. The authority to allocate taxpayer capital by political favoritism could not safely be entrusted to even the most saintly and omniscient bureaucrats and politicians, and they would bear none of the losses from bad investments.

Proposal 8: We should return to a more progressive rate structure for the personal income tax, with marginal rates of tax increasing by ranges of taxable income, up to a top rate of 65 per cent, accompanied by a broadening of the tax base.

Problem 8: If a top tax rate of 65% would be harmless to the economy and raise more revenue, then why is no country in the world adopting this advice? All of the fastest-growing economies in Asia and Eastern Europe have very low and sometimes flat marginal tax rates, particularly on capital. All countries with very high and/or rising marginal tax rates (France, Greece, Japan, etc.) have performed quite poorly. U.S. tax revenues were a larger share of GDP when the top tax rate was 28% than when it was 70% or 91%.

Proposal 12: Child Benefit should be paid for all children at a substantial rate and should be taxed as income.

Problem 12: Atkinson views his “Child Basic Income” (CBI) plan as an intermediate stepping stone toward his comprehensive Basic Income plan because he thinks it easier to peddle to intransigent voters than his actual Basic Income goal for everyone. Basic Income is essentially the 1967 “credit income tax” plan designed by James Tobin of Yale and converted into a $1000 “demogrant” for Sen. McGovern’s 1972 Presidential campaign. What McGovern missed is that a flat tax was the other key element of Tobin’s plan, as was confirmed by later work by Atkinson and Stiglitz on optimum taxation.

Proposal 13: A participation income should be introduced at a national level, complementing existing social protection, with the prospect of an EU-wide child basic income.

Problem 13: Participation income is another rhetorical device (like CBI) for moving toward a Basic Income on a piecemeal basis. The pretense is to make guaranteed income conditional on “participation in the society” by residents (not just citizens). In addition to all children and seniors, checks go out to those participating in approved training, taking approved care of children; doing approved volunteer work, etc. Caseworkers empowered to decide which activities get approved would have treacherous authority to promote politically-favored nonprofits and thwart others. If he can’t sell this idea, Atkinson’s alternative Proposal 14 is to simply to spend more on “social insurance, raising the level of benefits and extending their coverage.”

Proposal 15: Rich countries should raise their target for Official Development Assistance to 1 per cent of Gross National Income.

Problem 15: Foreign aid has often been used to prop-up bad policies and authoritarian politicians, and has never helped those economies in Asia and elsewhere which lifted themselves from chronic poverty to rapid economic growth – after reducing tax rates, tariffs and regulations. Besides, no academic has any right to tell taxpayers of sovereign nations how their elected representatives “should” spend their money

After his 15 Proposals, Atkinson also mentions even stranger “Ideas to pursue.” The zaniest, borrowed from Thomas Piketty, is “a global tax regime for personal taxpayers, based on total wealth.” Try to imagine the size and power of the required global army of tax collectors attempting to assess every wealthy individual in every country and collect a tax based on such inevitably arbitrary assessments. If such a tax could be enforced on a global scale, there would clearly be no democracy anywhere.

Sir Atkinson’s old-fashioned “policy polemic,” as the New York Times’ reviewer described it, is surprisingly disappointing. He wrote a much bolder and better book back in 1995: Public Economics in Action: The Basic Income/Flat Tax Proposal. In it, he suggested replacing all means-tested and social insurance benefits (such as unemployment or disability benefits) with a guaranteed annual income (refundable tax credit). This would, he wrote, “do away with the present complicated means-tested benefits” and shrink unemployment. A key second part of the plan required replacing the progressive income tax with an optimal flat tax of 16–31%. The combination of a flat tax and basic income, he concluded, “should definitely be on the agenda for public discussion.” What Atkinson now proposes, unfortunately, is the exact opposite – numerous lavish political gifts ostensibly financed with destructive tax rates on capital and entrepreneurship. These proposals would soon leave any country that adopted them in ruins.

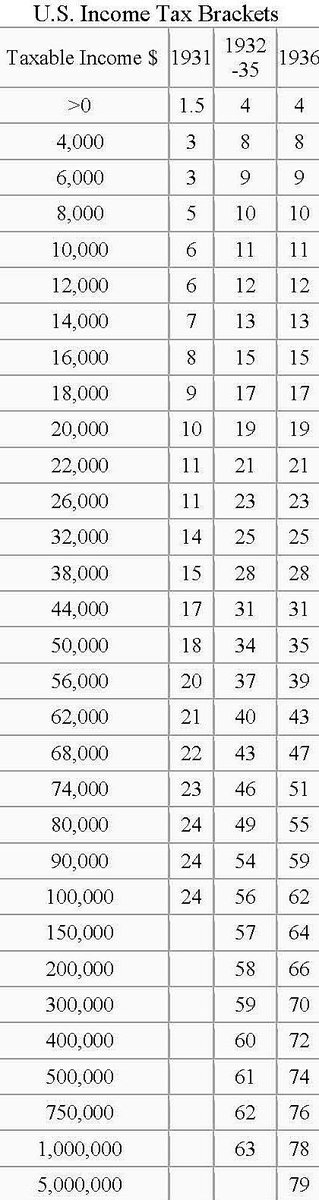

My recent Wall Street Journal op-ed, “Hillary Parties Like It’s 1938,” is not just about FDR’s self-defeating “tax increases” in 1936–37. It is also about the particularly huge across-the-board increase in marginal tax rates the Herbert Hoover pushed for and enacted retroactively in 1932. The primary motive in 1932, as in 1936, was to raise more revenue. Federal spending under President Hoover doubled from 3.4% of GDP in 1930 to 6.8% in 1932, and he believed that unprecedented spending spree required that tax rates be even more than doubled to “restore confidence.”

{kind=link}

Unfortunately, things did not quite work out as planned. Total federal revenues fell dramatically to less than $2 billion in 1932 and 1933 — after all tax rates had been at least doubled and the top rate raised from 25% to 63%. That was a sharp decline from revenues of $3.1 billion in 1931 and more than $4 billion in 1930, when the top tax was just 25%.

Some may object that this is unfair, arguing that revenues should be expressed as a share of GDP because GDP fell so sharply in 1932 and 1933. But that begs a key question. Comparing the drop in revenues to the even deeper drop in GDP would make sense only if the depth and duration of the 1932–33 drop in GDP had absolutely nothing to do with higher tax rates (including Smoot-Hawley tariffs). Yet neither Keynesian nor supply-side economics would consider huge tax hikes are so harmless (though Keynesians, seeing no revenue gain, might come to the paradoxical conclusion the Hoover actually cut taxes).

In any case, dividing weak revenues by even weaker GDP doesn’t help support the conventional wisdom that higher tax rates always bring higher revenues. Revenues fell even as a share of falling GDP – from 4.1% in 1930 and 3.7% in 1931 to 2.8% in 1932 (the first year of the Hoover tax increase) and 3.4% in 1933. That illusory 1932–33 “increase” was entirely due to less GDP, not more revenue.

The 15 highest tax rates were increased again in 1936, dividends were made fully taxable at those higher rates, and both corporate and capital gains tax rates were also increased as explained in my Journal piece. Yet all of those massive “tax increases” imposed by Presidents Hoover and Roosevelt failed to bring as much revenue in 1936 as was collected with much lower tax rates in 1930.

If the goal is to shrink GDP, the 1932–37 experience suggests that steeply progressive tax rates certainly accomplish that, particularly when they’re aimed at business and investors.

If the goal is to raise more revenue, on the other hand, the fact is that a top tax of 28% brought in more revenue than we ever did with top tax rates of 70% or 91%.

{kind=link}

Related Tags

There have been many good, if ultimately unconvincing, arguments against allowing younger workers to privately invest a portion of their Social Security taxes through personal accounts. There have been even more silly ones. One of the silliest is the one regurgitated Monday by ThinkProgress, that this week’s stock market decline proves that “If Social Security Had Been In Private Accounts The Stock Market Drop Could Have Been A Disaster.”

Few personal account plans would require a retiree to cash out their entire account on the day that the market crashed. But what if they did? It is important to understand that someone retiring Monday would have begun paying into their account 40 years ago when the Dow was at 835.34. After yesterday’s decline, it opened at 15,676 today. Over those 40 years, the worker would have made roughly 1,040 contributions to their account. Only 48 of them would have been at a time when the market was higher than today’s open.

Yep, even after Monday’s crash, the worker would have made a tidy profit. In fact, his return would have been substantially higher than what he could expect to receive from Social Security.

The last that defenders of the status quo made this argument was 2009, during the market crash that led into the Great Recession. At that time the market hit a low of 6,547. Obviously, if workers had been allowed to start investing then, they would have done pretty well. But more importantly, retirees in 2009 would have done well too, once again better than Social Security.

Cato published this comprehensive study of that downturn and its impact on personal accounts.

Social Security is running nearly $26 trillion in future unfunded liabilities. It cannot pay promised future benefits to young workers without substantial tax hikes. We should begin a discussion of how to reform this troubled program. A start to such a discussion would be to retire the canard about market crashes and personal accounts.

Cross-posted at TannerOnPolicy

Related Tags

Several recent news stories report information that was hardly surprising to anyone who has studied economics or read Cato at Liberty. We talk a lot about unintended or unanticipated consequences around here, but in these cases the consequences were anticipated and even predicted by a lot of people.

First, consider this front-page story from the Washington Post on Monday:

The [fast-food] industry could be ready for another jolt as a ballot initiative to raise the minimum wage to $15 an hour nears in the District and as other campaigns to boost wages gain traction around the country. About 30 percent of the restaurant industry’s costs come from salaries, so burger-flipping robots — or at least super-fast ovens that expedite the process — become that much more cost-competitive if the current federal minimum wage of $7.25 an hour is doubled.…

Many chains are already at work looking for ingenious ways to take humans out of the picture, threatening workers in an industry that employs 2.4 million wait staffers, nearly 3 million cooks and food preparers and many of the nation’s 3.3 million cashiers.…

The labor-saving technology that has so far been rolled out most extensively — kiosk and tablet-based ordering — could be used to replace cashiers and the part of the wait staff’s job that involves taking orders and bringing checks.

Who could have predicted that? Well, Cato vice president Jim Dorn in his 2014 testimony to the Maryland legislature. Or Bill Gates around the same time.

Then there’s this all-too-typical AP story out of California:

California lawmakers from both parties are calling for more stringent oversight of a clean jobs initiative after an Associated Press report found that a fraction of the promised jobs have been created.

The report also found that the state has no comprehensive list to show much work has been done or energy saved, three years after voters approved a ballot measure to raise taxes on corporations and generate clean-energy jobs.…

The AP reported that three years after voters passed Proposition 39, money is trickling in at a slower-than-anticipated rate, and more than half of the $297 million given to schools so far has gone to consultants and energy auditors.

Well, you might have seen that coming if you’d read Cato’s 2011 book The False Promise of Green Energy. Or Thomas Hemphill and Mark Perry in 2012. Or Dan Mitchell in 2008 on government job creation. Or indeed Henry Hazlitt in 1946.

And finally this recent study from the Federal Reserve finding, as reported by Bloomberg:

The surging cost of U.S. college tuition has an unlikely culprit: the generosity of the government’s student-aid program, a report by the Federal Reserve Bank of New York said.

Increases in federal loans, meant to help students cope with rising costs, are quickly eaten up by schools in higher prices, wrote David O. Lucca, Karen Shen and Taylor Nadauld.

Private colleges raise their tuition 65 cents for every dollar increase in federal subsidized loans and 55 cents for Pell grants given to low-income students, according to the report. College tuition has outstripped U.S. inflation for decades.

Who would have guessed? Certainly not Hillary Clinton. But Gary Wolfram, author of this 2005 Cato study, understood what was going on. So did Neal McCluskey in 2009 and Jason Bedrick in 2012 and Steven Pearlstein in 2004. Clinton and other political leaders may not read the Cato website diligently. But you’d think they’d have seen Pearlstein’s article in the, um, widely read Washington Post.

Understanding basic economics can make it fairly easy to predict the results of price floors, price ceilings, subsidies, job creation schemes, and other efforts in economic discoordination. It’s too bad that the widespread availability of economic knowledge doesn’t seem to do much to improve public policy.