The Financial Report of the United States Government (also known as the Financial Report) raises significant concerns about the country’s long-term financial health with increasing deficits and debt levels. Over the next 75 years, U.S. taxpayers face nearly $80 trillion in long-term unfunded obligations. What’s more, 95 percent of this unfunded obligation is driven by only two federal government programs: Medicare and Social Security.

Here are five key takeaways from the Financial Report:

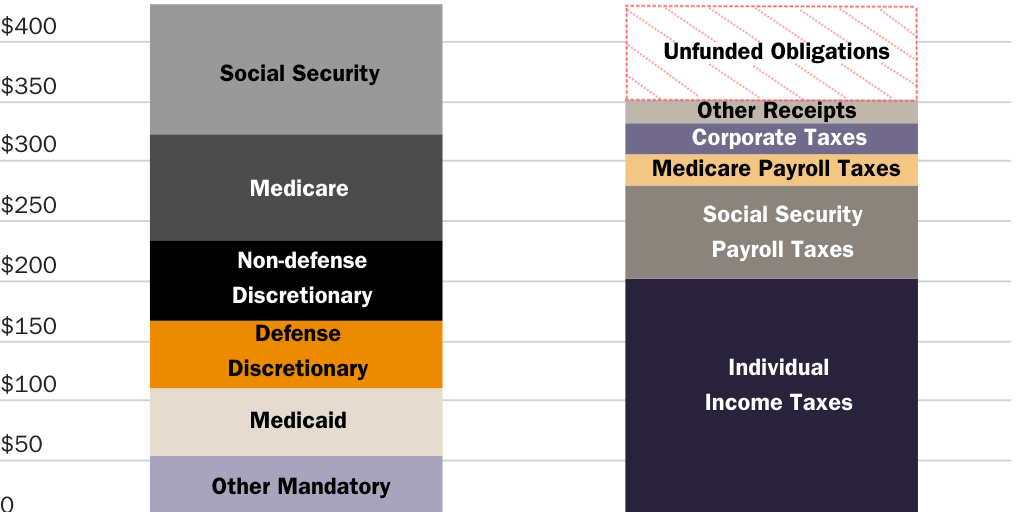

Over the next 75 years, the U.S. government’s unfunded obligations total $79.5 trillion. Over the next 75 years, the unfunded obligations are the difference between the present value of projected non-interest spending of $430.2 trillion (see Figure 1) and the present value of total receipts of $350.6 trillion over the same period. Present value means that future cash flows have been discounted to adjust for expected inflation and interest rates, recognizing that one dollar today is more valuable than one dollar tomorrow. The discount rate reflects the expected rate of return taxpayers could have received over the next 75 years if they invested the 2022 value.

Over the next 75 years, Medicare and Social Security funding shortfalls comprise 95 percent of the total unfunded obligation. As shown in Figure 2 below, of the $79.5 trillion in unfunded U.S. government obligations over the next 75 years, Medicare and Social Security’s funding shortfalls make up $75.9 trillion, or 95 percent. The Statement of Social Insurance (SOSI) shows the present value of the government’s projected expenditures for Social Security and Medicare Parts A, B, and D, as well as the railroad retirement and black lung benefits programs, in comparison to social insurance revenue. Of the total unfunded obligation, less than 0.2 percent is due to railroad retirement and black lung benefits.

The financial report projects the debt-to-GDP ratio will reach 200 percent by 2046 and 566 percent by 2097, based on current policy. The report’s authors state the obvious, albeit in muted terms: “The continuous rise of the debt-to-GDP ratio indicates that current fiscal policy is unsustainable.”

Closing the fiscal gap requires primary (non-interest) deficit reduction of 4.9 percent of gross domestic product (GDP) over the next 75 years. The fiscal gap is an estimate of what it would take, over the next 75 years, to stabilize fiscal policy. The financial report indicates that closing the fiscal gap would require non-interest spending reductions and or revenue increases of 4.9 percent of GDP annually, over the next 75 years. Any delays in adopting this deficit reduction would substantially increase required future deficit reductions. If legislators delay reforms for 10 years, to begin in 2033, closing the fiscal gap will require 5.7 percent of GDP. Delaying reforms by 20 years increases the required deficit reduction to 7.0 percent of GDP. The fiscal gap is an effective way to measure the burden that current U.S. government budget policy will impose on future generations.

Overshadowed by the CBO Outlook

The Financial Report of the United States Government received a silent reception in Washington and across the country when it was published on February 14. Readers of this blog will be hard-pressed to find mention of it among any of the major news outlets. This is in stark contrast to the Congressional Budget Office’s (CBO’s) Budget and Economic Outlook, which dropped the next day and made headlines far and wide.

Perhaps it was the unfortunate timing of the Financial Report that led to it getting buried. Or perhaps the focus on a 10-year budget outlook over a 75-year projection of government revenues and spending is one more example of the myopia that characterizes U.S. fiscal policy. While both the CBO and Treasury reports provide legislators and the public with valuable information about the U.S. government’s fiscal health, they focus on different time horizons and present different data.

The Financial Report of the United States Government provides a comprehensive overview of the government’s financial position, including long-term trends and risks. In it, readers will find a detailed analysis of the government’s assets, liabilities, revenues, expenses, and projections of future obligations, prepared in accordance with general accounting standards. It is intended to provide a long-term view of the government’s financial health.

In contrast, the CBO Budget and Economic Outlook is a budgetary analysis that provides 10-year projections of federal spending, revenues, deficits, and debt. CBO also provides estimates of key economic indicators such as GDP, inflation, and unemployment. This report is intended to provide a short-term view of the government’s financial health, including the baseline against which new spending and tax proposals will be scored. Such scores inform legislators about the fiscal impact their proposals would have on 10-year budget projections and whether they would trigger deficit-reduction rules such as CUT-GO, a House rule that requires offsetting spending reductions if legislation were to increase mandatory spending during the decade.

The Financial Report Deserves More Attention

The Financial Report of the U.S. Government deserves more attention. The report’s findings are especially relevant in today’s political climate where politicians from both parties feel pressure to distance themselves from benefit cuts to Medicare and Social Security. The report makes it painfully obvious that Medicare and Social Security spending are the primary drivers of government debt. Adopting sensible reforms to old age entitlement programs is both necessary and urgent.