The US Department of Education is in the Trump administration’s crosshairs. Here are five major reasons it should be:

1. It’s unconstitutional: Education is nowhere among the specific, enumerated powers given to the federal government. That means the feds have no authority to govern in education. Even the big-government administration of Franklin Delano Roosevelt knew that. In 1943, the US Constitution Sesquicentennial Commission, which Roosevelt chaired, published a document that included the following: “Q. Where, in the Constitution, is there mention of education? A. There is none; education is a matter reserved for the states.”

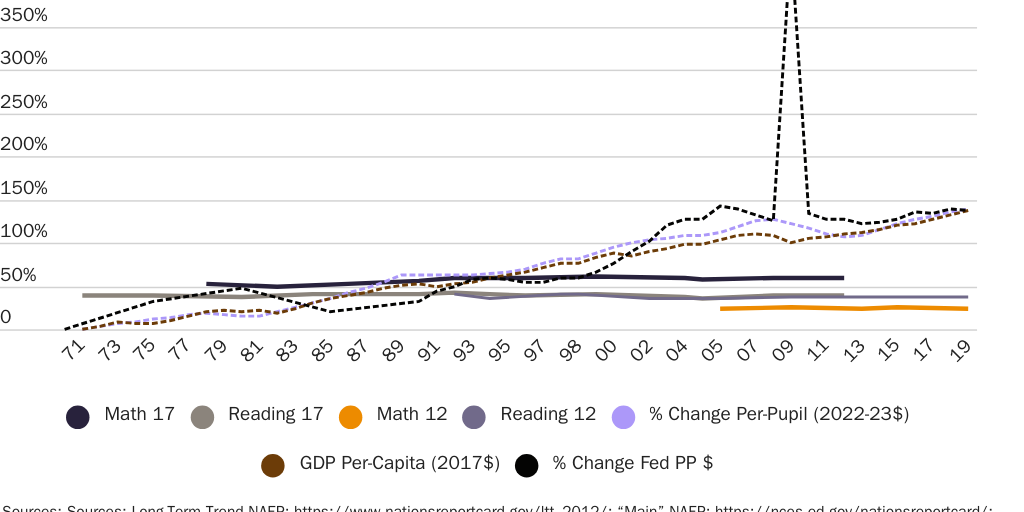

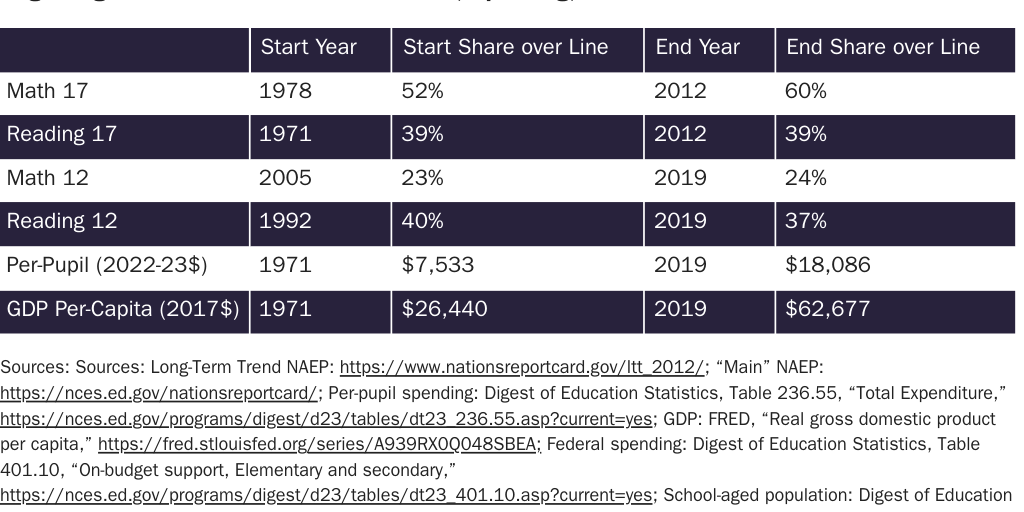

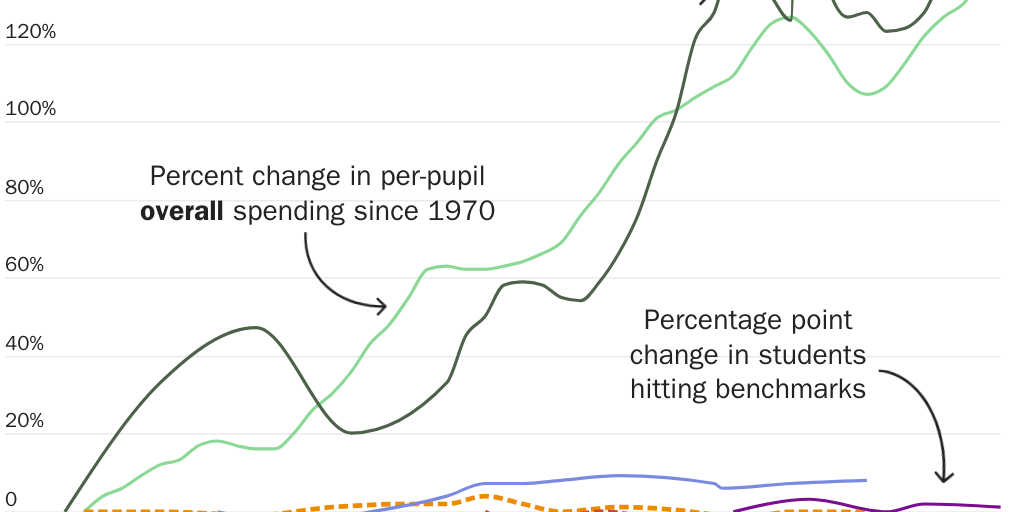

2. It’s ineffective: As indicated by the chart below, in K–12 education there is no meaningful evidence that the department, or federal spending generally, has improved education outcomes. While federal spending has risen, National Assessment of Educational Progress outcomes have largely stagnated. Of course, standardized test scores might not be a great barometer of how well the education system is working, but it is the feds that elevated them under the No Child Left Behind Act, Race to the Top, and Common Core. So by Washington’s own measure, it has not been very effective.

3. It’s incompetent: US ED’s biggest job is to administer federal student aid programs, especially student loans. But as the Government Accountability Office recently reported, US ED has failed at basic functions like tracking repayments for years. Heck, it could not even simplify the form to apply for aid without creating havoc, and it has failed audits for three years in a row.

4. It’s unnecessary: We had been educating kids for centuries before the department launched in 1980 and leading the world economically, technologically, and more. And US ED’s own mission statement is full of words such as “promote” and “supplement,” not “control” or “run.” Because states, districts, families, and educators are responsible for education, not Washington.

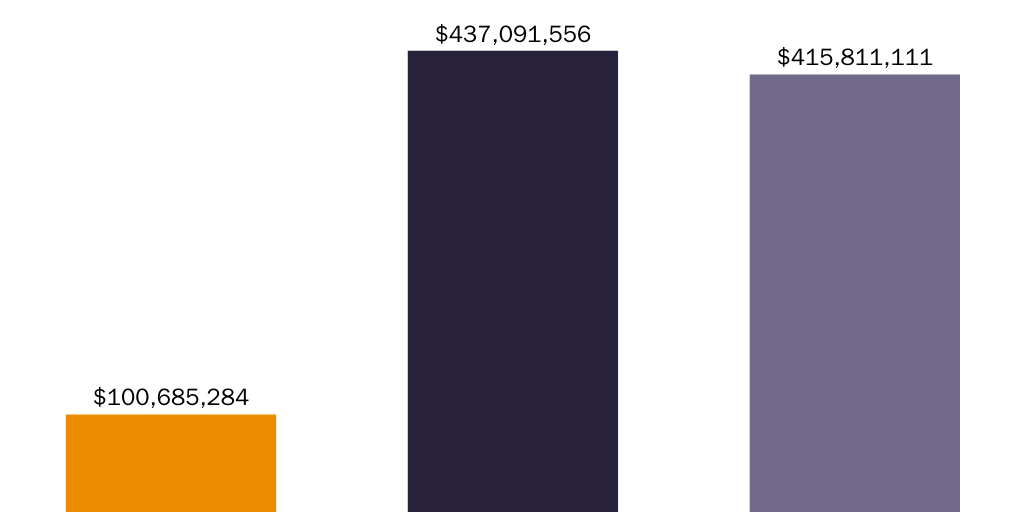

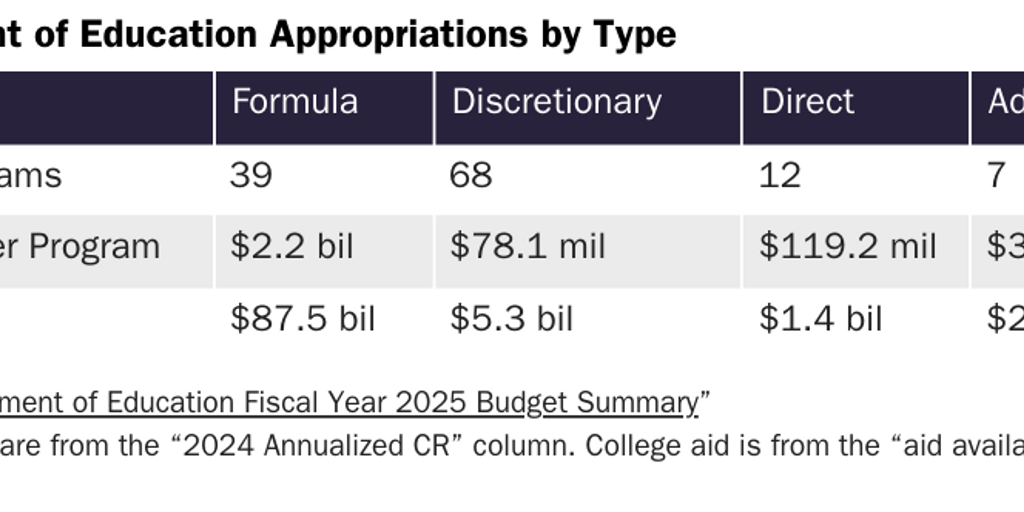

5. It’s expensive: Until recently, the department employed nearly 4,200 people and cost about $2.8 billion for salaries and expenses. And that’s setting aside all of the money it distributes and programs it runs, which are not about the department itself but tally hundreds of billions of dollars a year, depending on how you account for the huge, murky, unconstitutional student loan programs.

An unconstitutional, ineffective, incompetent, unnecessary, and expensive federal department is not a benefit to the country. It’s a mistake that must go away.