Following up on what Dan and Chris have said …

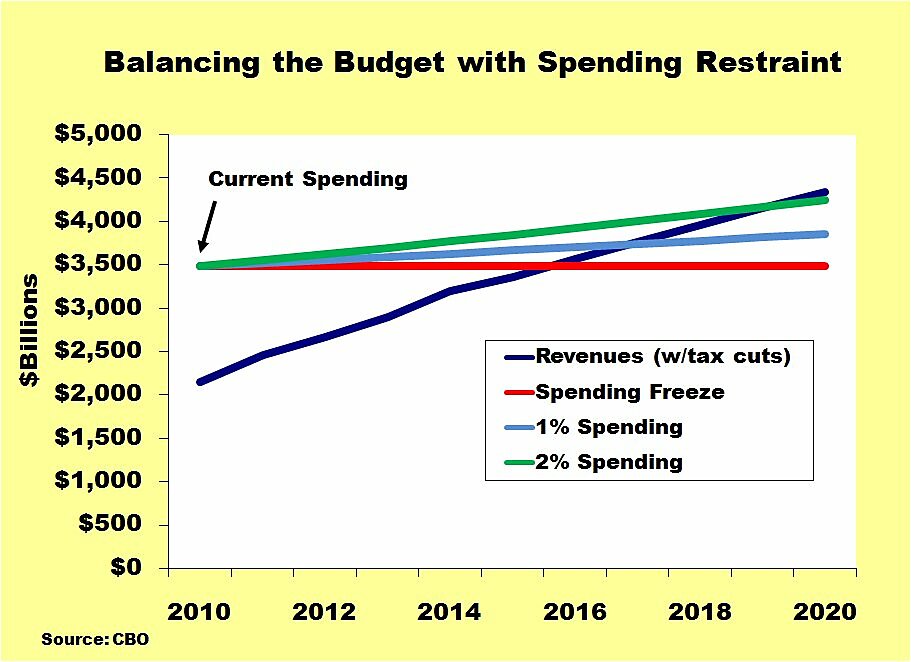

If the co-chairs of President Obama’s fiscal commission were serious about reducing federal spending and deficits, they would have proposed eliminating the federal deficit, rather than “reduc[ing] it to 2.2 percent of GDP by 2015.” Yawn. They would have proposed cutting federal spending (currently, 24 percent of GDP and rising) to match federal tax revenue (currently at 15 percent of GDP). But the co-chairs proposed only to “bring spending down to 22 percent and eventually 21 percent of GDP.” Not only does that elicit another yawn, but since the co-chairs only asked for half a loaf, they won’t even get that much.

If the co-chairs were serious about reducing federal spending and deficits, they would have proposed a balanced-budget amendment. They would have proposed block-granting Medicaid. They would have proposed implementing Medicare vouchers immediately. (Vouchers are the only way to reduce Medicare spending while protecting seniors from government rationing. They would also change the political dynamics that repeatedly stymie efforts to reduce Medicare spending.) Instead, the co-chairs propose the same ol’ failed strategy of trying to limit Medicare and Medicaid spending using government price-and-exchange controls, which they euphemistically describe as “rebates” and “payment reforms.” Along the same lines, they propose strengthening IPAB, ObamaCare’s rationing board. IPAB’s mandate is — you guessed it — to ration care by fiddling with Medicare and Medicaid’s price and exchange controls. It will therefore inevitably fall prey to the same political buzzsaw. To appease Republicans, the co-chairs propose unwise and unconstitutional federal rules that would prevent patients injured by negligent physicians from recovering the full amount they are due (euphemism: medical malpractice liability “reform”). Finally, the co-chairs propose that if federal health spending continues to grow faster than GDP growth plus 1 percent, Congress should consider “a premium support system for Medicare” (which could mean vouchers) and “a robust public option and/or all-payer system” for people under age 65 — a debate that wouldn’t even begin until 2020.

Fiscal Commission members, congresscritters, and citizens who are serious about reducing federal spending and deficits — and who are looking for specific ways to cut government spending — should instead consult Cato’s excellent web site DownsizingGovernment.org.