On July 21, 2010, President Obama signed into law the Dodd-Frank Wall Street Reform and Consumer Protection Act. Critics decried the legislation as one of the most onerous pieces of corporate governance regulation since the Sarbanes-Oxley Act of 2002 (SOX).

One of Dodd-Frank’s most contentious provisions is Section 922, which directs the Securities and Exchange Commission to implement a “whistleblower” program by which individuals may report suspected securities violations to the agency. Previously, SOX’s Section 301 had required firms’ audit committees to establish and monitor whistleblower programs by which suspected violations could be reported internally, but Dodd-Frank elevates whistleblowing by enabling employees, vendors, and customers, among others, to bypass companies’ internal control systems and report accusations directly to the U.S. Government. Dodd-Frank further stipulates that whistleblowers could receive as much as 30 percent of any fines, penalties, or the repayment of losses resulting from their reports.

Firms, attorneys, and others have been vocal about the potential for harm associated with the Dodd-Frank whistleblowing mechanisms. The SEC received over 950 comment letters following its publication of proposed rules for implementing Section 922. In particular, concerns have been expressed about the potential for disgruntled individuals to make unsubstantiated accusations in an effort to gain financial rewards, and the potential adverse impact of false claims on stock prices and customer and vendor relationships.

In this article, we attempt to determine how heavily the Dodd-Frank whistleblower bounty program might be utilized and the likelihood that it would be successful in its mission to “encourage people to report securities violations.” We do this by examining two analogous federal bounty programs, the Federal False Claims Act of 1863, as amended in 1986 and 2008, and the Internal Revenue Service’s Informant Claims Program. Our results suggest that, although rewards under these programs may be substantial, general use of the programs is not high. In light of Dodd-Frank’s similarities to these programs, and an expected lack of adequate federal funding to pursue reported claims, it is likely Section 922 will have similar results.

Comparing Whistleblower Programs

The United States has used whistleblower programs for almost 150 years. Below is a brief description of three of these programs, along with the Section 922 program.

The FFCA | The Federal False Claims Act (FFCA) offers incentives to individuals who report companies or individuals defrauding the government. It was implemented by President Lincoln in 1863 to protect the United States from purchases of fake gunpowder during the Civil War. Claims under the FFCA are typically related to health care or the military, and often report over-billing or billing for fraudulent services. Reporting of suspected tax fraud is excluded under the FFCA and instead is covered by the IRS’s whistleblower program described below.

As amended in 1986 and 2009, the FFCA offers financial incentives to whistleblowers of up to 30 percent of any recovery. It also includes anti-retaliation provisions including reinstatement, damages, and double back pay for workers who report their employers. Claims under the FFCA are filed with the Department of Justice under seal, meaning they will not be made public until the government decides to intervene. Claims cannot be brought against members of the armed forces, the judiciary, Congress, or senior executive branch officials.

To reduce the likelihood of false accusations, the FFCA imposes monetary penalties on individuals reporting false claims. Some states have enacted laws similar to the FFCA.

ICP | The Informant Claims Program (ICP), implemented under Section 7623 of the Internal Revenue Code, has been in effect since 1867. Under the ICP, an individual may report a taxpayer who underreports his tax liabilities, and the whistleblower could receive a bounty in return for the report.

The ICP’s only substantial modification came in 2006 when discretion of the amount of bounty paid to whistleblowers was removed, eligibility thresholds were enacted, and whistleblower appeals were provided. Under the program’s current form, if the IRS successfully uses the whistleblower’s information against an individual with adjusted gross income of at least $200,000 or an entity with underpayments of at least $2 million, the whistleblower is entitled to a bounty of up to 30 percent of funds collected, including taxes, penalties, and interest. Whistleblower bounties of up to 15 percent of recovered amounts are also available for smaller disputes. The IRS reserves the right to refuse payment of a bounty if the whistleblower is convicted of criminal conduct associated with the reported tax evasion.

SOX | The Sarbanes-Oxley Act’s Section 301 requires issuers’ audit committees to implement mechanisms for recording, tracking, and acting on information about potential securities violations provided by employees anonymously and confidentially. SOX Section 806 also broadened previous whistleblower protections to cover employees who report fraud to any federal regulatory or law enforcement agency, any member or committee of Congress, or any person with supervisory authority over the employee. Potential securities violations reported to a federal agency or an internal corporate compliance office under SOX carry no opportunity for financial bounty.

Dodd-Frank | To be eligible for a bounty under the Dodd-Frank Act’s Section 922, individuals — not organizations — must submit original information derived from the whistleblower’s independent knowledge pertaining to a corporation’s violation of securities laws. If the information results in a recovery, including fines and penalties, of at least $1 million from the accused corporation, the whistleblower may earn a bounty of 10–30 percent of the recovery. For example, if an employee supplies the SEC with a duplicate set of financial records that suggests his or her employer has reported falsified financial information and, as a result of the SEC’s investigation, the corporation is required to pay a $1 million fine, the whistleblower is eligible for a bounty of up to $300,000.

Individuals who are convicted of a crime related to the reported misconduct or who participate in reported violations are not eligible for the bounty. For example, if an employee of a foreign, government-controlled entity reports evidence of receiving a $10,000 bribe from a U.S. corporation to secure a $5 million contract and, as a result of the SEC’s investigation, the corporation must pay a $10 million fine under the Foreign Corrupt Practices Act, the reporting individual would not be eligible for a bounty. Issuers’ internal compliance personnel, attorneys, auditors, and other recipients of privileged communications are also ineligible to receive bounties for claims related to their clients’ securities violations. Uncertainty as to how the SEC would treat a whistleblower under these proposed disqualification rules may discourage whistleblowers from filing claims.

Dodd-Frank also includes protections for the whistleblower against employer retaliation. In the event of successful claims, protections include the possibility of reinstatement, double back pay with interest, expert witness fees, and attorney fees.

Claims and Bounties Under Existing Whistleblower Programs

The frequently offered concern about the Dodd-Frank whistleblower provision is that it will prompt many baseless reports that will be costly to accused firms. However, the relatively few instances in which would-be whistleblowers — legitimately or not — have made use of the FFCA and ICP suggest that this concern may be overstated.

The Department of Justice recently reported that, for the fiscal year ended September 30, 2010, recoveries under the FFCA totaled roughly $3.0 billion, of which $2.5 billion related to health care fraud recoveries (exclusive of criminal penalties and recoveries passed along to states). Some $2.3 billion of those recoveries were the result of information reported by whistleblowers, who received approximately $385 million in bounties. Since 1986, bounties paid to whistleblowers have totaled a little over $2.8 billion.

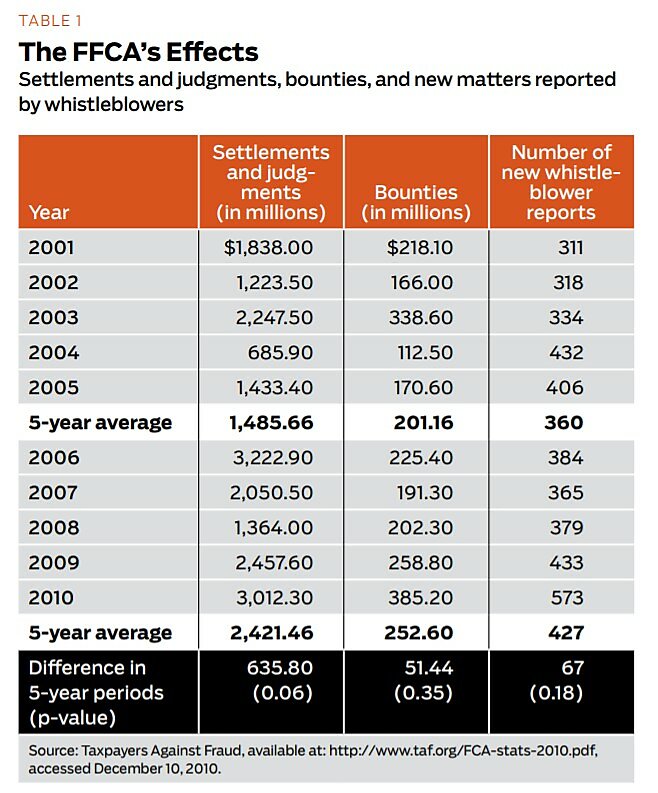

Table 1 presents data made available by Taxpayers Against Fraud, an organization that actively encourages individuals to report fraud under the FFCA. The table summarizes FFCA settlements and judgments, bounty payments, and number of new matters reported by whistleblowers (i.e., qui tam matters) during the period from fiscal year 2001 to 2010.

Although there was an increase in the number of whistleblower reports in 2010 (n = 573, compared to an annual average during the 10-year period of 393), the number of new reports did not change significantly if one were to compare the more recent five-year period (mean = 427) to the previous five-year period (mean = 360), p > 0.10. Civil settlements over the 10-year period averaged $1.9 billion per year and bounties averaged $226.9 million per year. Average annual settlements and judgments have increased moderately comparing the latest five-year period (mean = $2.4 billion) to the previous five-year period (mean = $1.5 billion), p = 0.06; while average annual bounties comparing the same periods have not changed significantly (mean of $253 million vs. mean of $201 million), p > 0.10.

Taxpayers Against Fraud further reports the number of cases associated with settlements and judgments during the period 2004–2010 ranged from 74 to 145, and the average bounty was $1.6 million per settled case. Settlements and judgments in 2010 were associated with 145 cases, or an average bounty of approximately $2.6 million per settled case. Based on these recent data, approximately 23 percent of whistleblower reports result in a bounty.

The types of matters reported by whistleblowers vary dramatically, but in the current decade many reports have pertained to the over-billing of Medicare and Medicaid. For example, drug maker Schwarz Pharma was found to have sold drugs to Medicaid that had never been approved by the Federal Drug Administration. Recoveries in the case amounted to $22 million and two whistleblowers received a bounty of $1.8 million. In another case, Chicago-area cardiologist Sushil A. Sheth pled guilty in 2010 to billing Medicare (and other entities) over a five-year period for 14,800 procedures that he never performed. In addition to jail time and fines of $24.3 million associated with the criminal case, Sheth also settled the related civil matter for $20 million. The whistleblower was credited with a bounty equal to 17.5 percent of the civil settlement, or $3.5 million.

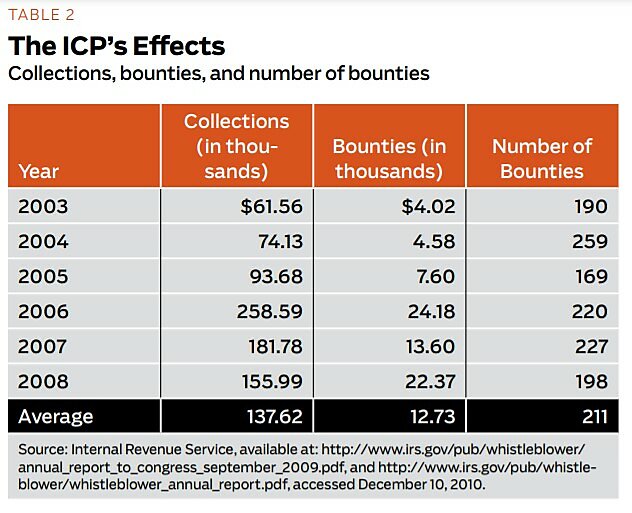

Data on claims under the IRS’s ICP are more limited than those of FFCA. Table 2 presents data reported by the IRS to Congress in 2009 summarizing collections, bounty payments, and number of bounties paid during the period from fiscal year 2003 to 2008. Annual collections during the period averaged $138 million and bounties averaged $13 million. The number of bounties associated with collections during the period ranged from 169 to 259, suggesting an average bounty of approximately $60,000 per report. These data do not reflect the effect of amendments to the ICP in 2006 removing discretion associated with bounty payments and instituting minimum thresholds for bounty payments.

The IRS reported to Congress that eligible ICP reports in 2008 totaled 1,246 and pertained to 476 taxpayers. Of those reports, 292 represented possible recoveries in excess of $10 million. Also in 2008, 198 investigations were settled, but only eight of those cases met the $2 million underpayment eligibility threshold enacted in 2006 and applicable beginning in fiscal 2009. The IRS also reported its whistleblower office recently increased in size from four to 14 full-time staff, likely in response to increased whistleblower reports and the results of a 2009 audit by the Treasury Department’s inspector general for tax administration that reported inadequate processes and procedures for timely pursuit of whistleblower claims.

A recent matter illustrates the complexity of ICP whistleblower reports. In 2007, a former employee of Switzerland-based UBS asserted the bank was guilty of helping American offshore taxpayers avoid U.S. taxes and filed a claim for an ICP whistleblower bounty. The matter resulted in collection of a $780 million settlement and UBS is required to turn over the names of the depositors it assisted. While the whistleblower and his attorney believe he is entitled to an ICP bounty that could ultimately be in the hundreds of millions of dollars, the IRS contends that it should not have to pay any bounty because, during the course of the investigation, the whistleblower pled guilty to a related criminal charge brought by the Department of Justice and is now serving jail time. While employed by UBS, the whistleblower reportedly had an apartment in Geneva and a million-dollar home in Zermatt, Switzerland. It is not clear whether this example is best classified as “no good deed goes unpunished” or as “you can’t have your cake and eat it too.”

ConclusionCollectively, these data suggest that although rewards under existing whistleblower programs may be substantial, general use of the programs is not high. New whistleblower reports to either the Department of Justice under the FFCA or the IRS under the ICP totaled 1,625 in 2008. The number of new whistleblower reports under the FFCA has not varied significantly between the most recent five-year period and the preceding five-year period. Although comparable data are not available for the ICP, based on the number of bounties paid under the program there is no reason to believe the number of new reports is increasing — particularly in light of recent changes concerning minimum collection thresholds. In 2008, a total of $225 million in bounties associated with 631 whistleblower reports were paid under the FFCA and ICP.

Similarities between the FFCA, ICP, and Dodd-Frank lead us to believe the use and success of Dodd-Frank may be similar. Neither the FFCA nor the ICP is advertised broadly to individuals who are likely to become aware of fraudulent activities, and there is currently no indication that the Dodd-Frank whistleblower program will be broadly advertised. Historically, both the FFCA and ICP have been underfunded. The nation’s current budget deficit and the SEC’s recent announcement that it will not meet the Dodd-Frank deadline for establishing and staffing a whistleblower office suggest the program will not receive funding necessary for the timely pursuit of large volumes of whistleblower reports.

To reduce the likelihood employees will bypass companies’ internal whistleblower programs in favor of potential bounties that may be gained under Dodd-Frank, some have suggested firms consider changing their whistleblower programs so as to encourage internal reporting, perhaps even instituting firm-sponsored bounties. Our analyses suggest such changes are not necessary. Existing whistleblower programs have received limited use in spite of offered bounties and implementing internal bounties may have unintended consequences, including increases in unwarranted reports and additional administrative costs. Instead, firms should devote resources to reinforcing a “tone at the top” that promotes ethical behavior and legal compliance throughout the organization and encourages employees to use internal whistleblower programs to report any suspected wrongdoing.

Readings- “Audit Finds Flaw in Tax Whistleblower Program,” by S. Lengell. Washington Post, October 8, 2009.

- Brief Summary of the Dodd-Frank Wall Street Reform and Consumer Protection Act, U.S. Senate, July 10, 2010.

- “Dodd-Frank’s Whistleblower Bounties: An Effective Hotline May Keep You Out of Hot Water,” by M. J. Missal and M. T. Morley. Government Enforcement Alert, September 7, 2010.

- “For American Who Blew Whistle, Only Reward May Be a Jail Sentence,” by D.S. Hilzenrath. Washington Post, August 20, 2009.

- “Implementing the Dodd-Frank Wall Street Reform and Consumer Protection Act — Dates to be Determined,” published by the Securities and Exchange Commission. Online at http://www.sec.gov/spotlight/dodd-frank/dates_to_be_determined.shtml.

- “Pitfalls Emerge in Dodd-Frank Whistleblower Bounty Provision,” by B. Carton. Securities Docket: Global Securities Litigation and Enforcement Report, September 9, 2010.

- United States of America v. Sheth, 09-CR-00069, N.D. Ill., Aug 19, 2010, and United States of America and the State of Illinois, ex rel. Lokesh Chandra, M.D. v Sushil A. Sheth, M.D., 06 C 2191, N.D. Ill., filed Apr 19, 2006.

- United States ex rel. Constance Conrad v. Schwarz Pharma, et al., No. 02–11738-NG (D. Mass.)

- “Whistleblowing Galore under the Dodd-Frank Act,” by K. Griffith. Employer Law Report, August 2010.

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.