Federal government debt is rising to dangerous and unprecedented levels. Federal debt held by the public now tops $26 trillion, which is almost $200,000 for every household in the nation. At almost 100 percent of gross domestic product (GDP) and rising, the debt will soon reach levels never seen in our nation’s history.

The growing debt is imposing large burdens on current and future taxpayers, while also increasing the risks of macroeconomic instability and financial crises. Compared to GDP, the debt has already surpassed a threshold where it likely undermines economic growth.1

Congress should change course and cut spending to reduce debt. Lawmakers have tried to tackle the debt with new budget rules, but they have not balanced the budget in more than two decades and today are financing more than a quarter of federal spending with borrowing. No mechanisms to effectively restrain debt have gained wide support in Congress.

However, there is hope. A partial solution presents itself when we compare out-of-control federal debt to stable and legally constrained state debt. Federal debt is eight times larger than the combined debt of all state and local governments. Why is that the case, given that all elected officials have the same incentives to borrow and spend? The answer is that the states have extensive constitutional, statutory, and economic restrictions on deficits, debt, and spending that steer them toward greater fiscal responsibility.

An important way to tackle America’s debt problem is to devolve a large part of federal spending to the states, allowing them to fund it themselves. The federal government spends more than $1 trillion a year on state and local activities such as education, housing, and transportation. Congress should phase out federal spending on those activities, and if states wanted to fill the funding void, they would do so with current revenues, not debt.

It is better to fund government spending on domestic activities at the state level because state debt issuance is restricted. Legal rules and economic limitations force state policymakers to make responsible tax and spending trade-offs. To avert a debt crisis, America should take advantage of its federal structure and decentralize most government programs.

This study reviews efforts to restrain federal spending and debt, compares federal debt to state debt, and discusses how the states restrain debt. The final section proposes entitlement and federalism reforms that would avert the debt crisis and stabilize debt relative to GDP.

Restraining Federal Spending and Debt

The federal government has few restraints on borrowing. Every year it increases spending by however much Congress favors, and then the US Treasury borrows the funds needed beyond the revenues flowing in from taxes. In 2023 the federal government spent $6.1 trillion, raised $4.4 trillion in taxes, and borrowed $1.7 trillion to fill the gap.2 More than one-quarter of federal spending is being financed by fresh borrowing every year.

Unlike federal budgeting, state budgeting is bound by restrictions that steer policymakers toward balancing their budgets. Unfortunately, such restrictions were never imposed on the federal government, despite the anti-debt views of many of the Founders. In 1798 Thomas Jefferson wrote, “I wish it were possible to obtain a single amendment to our constitution … I mean an additional article taking from the federal government the power of borrowing.”3

There have been efforts to heed Jefferson and pass a balanced-budget amendment (BBA) to the US Constitution. In 1982 the Senate passed a BBA by a vote of 69–31, but the measure failed to gain the needed two-thirds approval in the House. In 1995 the House passed a BBA by a 300–132 margin, but the measure did not pass the Senate. In 2011 both chambers voted on BBAs, but again support came up short.

Congress has imposed a statutory limit on accumulated federal debt since 1917, but lawmakers routinely vote to increase it. Congress has occasionally passed anti-deficit laws, but these have since expired. The 1985 Gramm-Rudman-Hollings Act established deficit targets, which if not met resulted in automatic across-the-board cuts. Congress replaced that law in 1990 with the Budget Enforcement Act, which imposed dollar caps on discretionary spending and rules requiring any entitlement expansions to be offset elsewhere in the budget. The Budget Control Act of 2011 imposed multiyear caps on discretionary spending, but those have expired.

In 2023 the Fiscal Responsibility Act imposed two-year caps on discretionary spending, but the law did not limit entitlement spending, the largest part of the budget. Numerous proposals have been floated in Congress to cap overall spending growth, but none have been enacted.4 We are left today with exploding federal debt and Congress divided over which new rules are needed to limit the flood of red ink.

Federal Debt versus State Debt

The federal government needs to borrow during recessions when revenues decline, but those borrowings should be paid back when the economy is growing and revenues are rising. Congress has not practiced such prudent budgeting in more than two decades, which has resulted in massive and chronic deficits.

To appreciate just how massive, we can compare federal debt to state debt. Federal debt held by the public of $26 trillion is almost eight times larger than the $3.3 trillion combined debt of all state and local governments.5 Not only is the federal debt much larger, but the federal government has less justification for accumulating debt than the states. That is because the great majority of state and local debt is issued to finance capital investment. The debt is matched by large holdings of return-producing assets such as highways. By contrast, the great majority of federal debt funds consumption, not capital investment.

Also, most state‐local government debt consists of revenue bonds, which will be paid back mainly from revenues for facilities such as utilities, colleges, and hospitals. General obligation bonds backed by taxes account for a minority of state‐local debt. Thus, not only is state‐local debt much smaller than federal debt, but much of it will not be a burden on taxpayers.

Moody’s Investors Service reports on the portion of state government debt that is backed by taxes.6 In 2022 this debt averaged 2.8 percent of personal income across the states, which compared to federal debt as a percentage of personal income that year of 114 percent.

Moody’s also reports on debt-servicing costs for the states. In 2022 debt-servicing costs for state tax-supported debt were 2.2 percent of revenues, which compared to interest costs that year on federal debt of 9.7 percent of revenues. Currently, rising interest rates are pushing up interest costs for both the federal and state governments. The difference between the governments is that federal lawmakers have no plan to tackle the rising costs, but state lawmakers face budget restraints and will need to take actions to retain fiscal balance.

Those budget restraints are discussed next. We should use the built-in state restraints to reshape the nation’s government spending. Whatever overall level of spending Americans favor, most of it should be done by the states, not the federal government. This would ensure that spending is not financed by massive borrowing that endangers our future.

How States Limit Debt

State governments follow many constitutional, statutory, and procedural rules that steer policymakers toward fiscal restraint. The rules vary by state but generally include balanced budget requirements, limitations on debt, and tax and spending restraints. In addition, competition between the states restrains fiscal policies, as does the desire of state lawmakers to maintain strong ratings on state bonds.

Balanced Budget Requirements. Forty-nine of the 50 states have constitutional or statutory requirements to balance their annual budgets.7 The requirements take different forms: in 45 states the governor must submit a balanced budget; in 44 states the legislature must enact a balanced budget; and in 41 states the governor must sign a balanced budget.8 And, as the National Conference of State Legislatures noted, “political cultures reinforce the requirements.”9

State budget offices provide regular projections of revenues to alert policymakers if budgets are becoming unbalanced. Governors and legislatures take mid-year actions, such as spending cuts and hiring freezes, to ensure that budgets are on track to balance. At year-end, 35 states require policy actions to ensure that final spending matches revenues.10

Legal Debt Limits. Unlike the federal government, “borrowing is not a routine matter for state governments.”11 Forty-three states impose legal limits on either debt outstanding or debt-servicing costs, while just seven states do not have such limits.12

The states have learned from history the dangers of debt. Following the construction of the Erie Canal in the early 19th century, many state governments borrowed heavily to spend on canal projects. But lawmakers overestimated canal demand and underestimated costs, and most projects lost money.13 The failure of canals and other debt-backed state projects led to numerous debt defaults, which in turn spurred a wave of budget reforms. Between 1840 and 1855, 19 states imposed constitutional limits on state debt, and many further restrictions have been passed since.14

Today, about 40 states limit the level of state debt outstanding with either fixed dollar caps, caps tied to tax revenues, caps tied to statewide property values, or caps tied to state personal income. For example, five states have limits on state debt as a percentage of personal income, with an average of 3.8 percent.15 By comparison, federal debt was 116 percent of personal income in 2023.

About 29 states limit annual state debt-servicing costs. Of these, about 22 states impose debt-servicing limits calculated as a percentage of tax revenues, with an average of 7.2 percent. By comparison, federal interest costs as a percentage of tax revenues were 13.8 percent in 2023 and rising rapidly.16

General Obligation (GO) Bonds. Because GO bonds are a burden on taxpayers, states put more restrictions on them than revenue bonds, which are often backed by non-tax revenues. A handful of states, such as Idaho and Iowa, essentially ban GO bonds, and about half of the rest require voter approval for issuance.17 Of the remaining states, many require supermajority votes in the legislature to issue GO bonds.

Tax-and-Expenditure Limits (TELs). These are restraints that 26 states impose to provide a layer of restraint on top of balanced budget requirements and debt limits. For example, Colorado’s Taxpayer Bill of Rights—passed by initiative and part of the state constitution—requires the state to refund taxes to residents if revenue growth in a year exceeds the growth in population plus inflation. In addition, Colorado limits state spending to either 5 percent of personal income or 6 percent growth from the prior year, whichever is less.

Rainy Day Funds. All 50 states use rainy day funds, a budgeting device to avoid the need to borrow during downturns. In years with strong economic growth, states put a portion of tax revenues aside in the funds, and then funds can be withdrawn during lean years to maintain budget balance. In 2023 the savings in these state funds averaged 13 percent of annual expenditures.18

Other Restraints. States have additional structures that steer policymakers toward restraint. Legislatures generally appropriate all spending during each budget cycle, and they have generally not created “mandatory” spending that is on autopilot, as Congress has.19 Also, governors in 43 states have line-item vetoes that allow them to strike spending items they do not approve.20

Economic Restraints. State budgeting is restrained by economic forces. The states compete with one another for residents and investments, and their taxes, budgets, and economies are easily compared. State policymakers face competitive pressures to keep government lean that the federal government, with its national monopoly, does not.

One aspect of competitive federalism is the market for state and local borrowing. Credit rating agencies examine government finances and assign ratings that affect interest rates paid on state debt. The process encourages governments to stabilize their budgets and minimize debt and unfunded liabilities. A state bond rating downgrade is painful because policymakers know that rising interest costs will displace other budget priorities. By contrast, federal policymakers seem to assume that they can always borrow more to fund increased spending.

It is true that some states are more fiscally irresponsible than others. But even the state with the highest tax-supported debt as a percentage of personal income—Hawaii, at 11 percent in 2022—appears frugal compared to the federal government, with its debt of 114 percent of personal income that year.21

It is also true that many states have underfunded employee pension and retirement health plans. But the total amount of underfunding (about $3 trillion) is just a fraction of the federal underfunded obligations of Social Security and Medicare of about $177 trillion.22 Also, unlike the federal government, state governments have been making incremental reforms to reduce their underfunded costs.

Finally, state policymakers sometimes cheat on state fiscal rules. They delay required pension contributions, defer payments to state vendors, and maneuver to get around debt restrictions. But large-scale cheating on state debt restraints is the exception rather than the rule. The proof that the combination of all these state restraints works is that total state and local debt is just a small fraction of federal debt.

Federalism Solution

The stark difference in restraint between federal and state budgeting suggests that the former should adopt the practices of the latter. It would be a major advance to impose state-style spending and debt restraints on the federal budget, but enacting such restraints has proven elusive. Moreover, even if the federal budget were subject to tighter legal restraints, it still does not face the same high level of credit-market discipline that state budgets do.

The good news is that there is another way to bring state-style discipline to federal spending: move federal programs down to the state level. To revive fiscal sanity, we should take advantage of America’s federalist structure and devolve the funding of most government programs to the states. Most programs should be funded by the states because they have better fiscal controls than the federal government.

The federal government accounts for about two-thirds of the nation’s government spending, with state and local governments accounting for about one-third.23 We face a debt crisis because government spending is dominated by a government devoid of restraints. We should flip the spending structure and fund most programs at the state level.

Such a reform may sound radical, but several high-income democracies have such decentralized structures. In 2021 federal spending as a percentage of total government spending was just 35 percent in Switzerland and 42 percent in Canada, compared to 71 percent in the United States.24 As an example of decentralization, Canada’s federal government does not subsidize K–12 education—school funding is purely a provincial and local matter.25

Decentralization would begin solving the debt crisis, and there would be other benefits. As detailed in a 2019 Cato study, devolving programs to the states would do the following:

- Reduce spending distortions. Federal aid for the states induces state lawmakers to spend more on the subsidized activities than their residents would favor if they were directly footing the bill.

- Reduce bureaucracy. Federally funded programs require more layers of wasteful bureaucracy than purely state and local programs.

- Reduce fraud and abuse. To state administrators, federal aid is “free” money for the state, reducing the incentive to spend frugally.

- Reduce regulations. Federal aid is tied to piles of top-down labor, environmental, safety, and other regulations that raise the costs of programs and projects.

- Increase diversity. State residents vary in their preferences for education, welfare, transit, and other activities. Removing federal intervention would allow each state to better match programs to local preferences.

- Increase democracy. Federal aid and related regulations are imposed by unknown bureaucracies in faraway Washington. Devolving programs would move decisionmaking back to elected officials in the states.

- Increase accountability. The confused mess of three layers of government being involved in local activities, such as K–12 schools, reduces political accountability. Removing federal rules and bureaucracies would make lines of authority clearer to citizens.26

In sum, adding fiscal restraints to the federal budget would be beneficial, but we do not need to reinvent the wheel. The 50 states already have sophisticated budgeting systems that require policymakers to balance budgets and restrain debt. Decentralizing the funding of programs would take advantage of the nation’s federalist structure and improve the quality and efficiency of government services.

Plan to Stabilize Debt

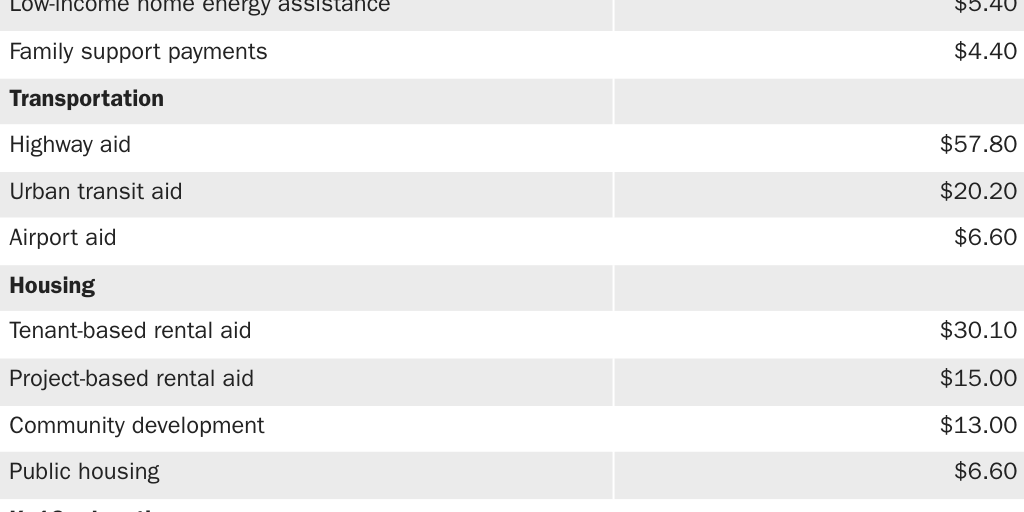

Table 1 summarizes $1.3 trillion in aid-to-state programs, which are federal subsidies to state and local governments that are paired with top-down regulations.27 The states use the subsidies to administer programs in health care, welfare, transportation, housing, education, and other activities.

The table lists the 30 largest aid-to-state programs and also tallies total spending on hundreds of smaller aid-to-state programs. I have included two programs that are not officially aid-to-state programs but operate similarly—the Supplemental Nutrition Assistance Program and project-based rental assistance.

Congress should begin devolving aid-to-state programs to the states. State and local governments are entirely capable of funding their own domestic programs. Such federalism reforms should be a component of broader efforts to reduce federal spending and debt.

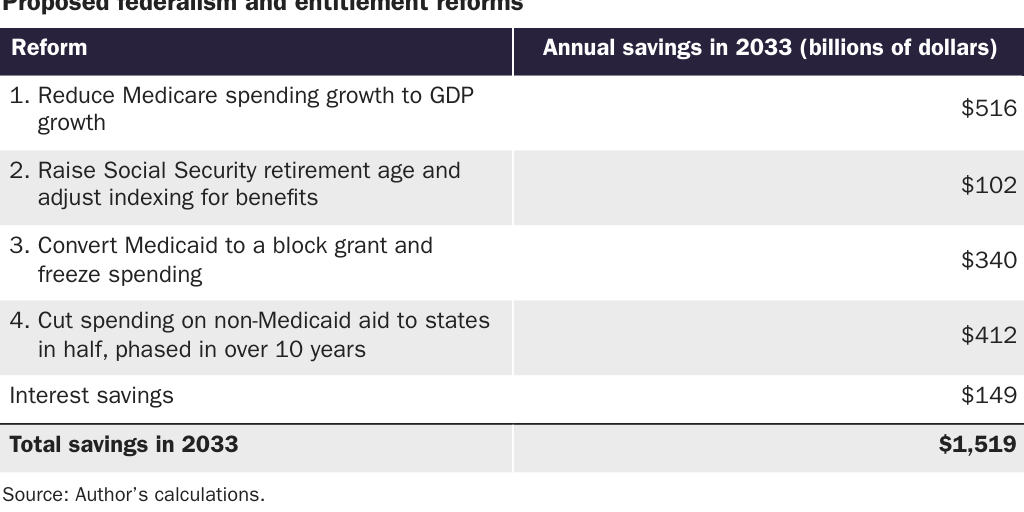

A near-term goal of such efforts should be to stabilize federal debt held by the public at 100 percent of GDP. Debt is currently projected to rise to 115 percent of GDP by 2033 and continue rising after that. Table 2 lists four federalism and entitlement reforms that together would stabilize the debt at 100 percent of GDP by 2033.

First, Congress should limit Medicare’s growth to the growth rate of GDP. One way to achieve that would be to restructure benefits as individual vouchers for buying health insurance in the marketplace. Such reforms would improve choice, encourage competition, and restrain costs.28 Restraining Medicare growth to GDP beginning in 2026 would save $516 billion annually by 2033.

Second, Congress should trim the growth in Social Security by raising the full retirement age and adjusting the inflation calculation for benefits. These changes—based on Congressional Budget Office options—would save $102 billion annually by 2033.29

Third, Congress should convert Medicaid to a block grant and freeze spending at the 2024 level. The states would receive a fixed amount of funding but would face reduced federal regulations, allowing them to pursue efficiencies and innovations. This would save $340 billion annually by 2033.

Fourth, Congress should cut spending on all non-Medicaid aid-to-state programs in half by 2033. The federal government should remove itself from purely state-local activities such as low-income housing and K–12 education. Phased in over 10 years, the cuts would save $412 billion annually by 2033.30

These four spending reductions, along with related reductions in interest costs, would cut federal spending by $1.5 trillion in 2033, or 16 percent of the Congressional Budget Office’s projected spending for 2033. By my estimate, that would be enough to reduce federal debt from the currently projected 115 percent of GDP that year to 100 percent.

The states could respond to receiving less federal aid in several ways. They could raise taxes to continue funding programs at previous levels. They could innovate and reduce program costs. They could cut other parts of their budgets to free up funds. Or they could privatize programs and facilities, such as airports, to fund them in the marketplace rather than with subsidies.

In addition to these federalism and entitlement reforms, Congress should cut business subsidies, farm subsidies, foreign aid, and energy subsidies. Congress is overspending in many areas, but reviving federalism is one crucial way to tackle the debt crisis.

In sum, the federal government is spending more than $1 trillion a year on properly state and local activities. With rapid spending growth on Medicare, Social Security, and interest, the federal government can no longer afford to fund activities that the states can fund themselves.

As debt soars to unprecedented levels, the federal budget must be cut. Reducing federal spending on state and local activities would help solve the debt crisis and improve the efficiency and accountability of government programs.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.