Earlier this week I repeatedly heard the claim that if the federal government does not guarantee credit risk in the mortgage market, foreigners won’t buy U.S. mortgage-related debt. Before we test whether that claim is true, let’s first determine just how important are foreign investors in the U.S. mortgage market.

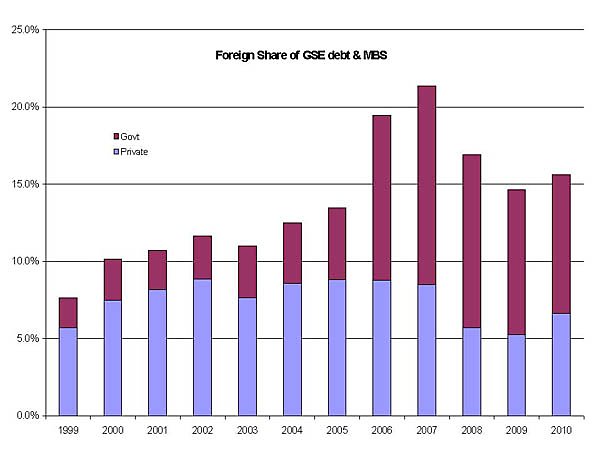

For the most part, foreign investors do not hold U.S. mortgages directly, but either hold Fannie and Freddie debt and mortgage-backed securities (MBS) or hold private-label MBS. As the private-label securities lack a government guarantee, we can ignore that segment of the market. The chart below depicts the percentage share of foreign ownership of these securities in recent years:

The chart illustrates that, at times (particularly around the peak of the recent housing bubble), foreign investors have been large providers of capital to the GSEs. In 2007, over 20% of GSE debt was held outside the United States, double the percentage from only a few years earlier. The increase was driven almost exclusively by purchases by foreign governments (mostly central banks for the purpose of currency manipulation). In 2007, this amounted to just over $1.5 trillion.

However, if we went back and looked at a year prior to the super-heated housing market — say 2003 — then this total is about $650 billion. Given that U.S. commercial banks now have about $1 trillion in cash sitting on their balance sheets, it appears that domestic sources could completely fund the U.S. mortgage market without any foreign funds.

But let’s say we want to keep the option of living beyond our means and have the rest of the world fund a large part of our mortgage market. Would they? Given that foreign investors currently hold over $5.4 trillion in U.S. corporate bonds and equities (not all guaranteed by the U.S. taxpayer), I think it’s fair to assume that these foreign investors have some appetite for U.S. assets.

Now does that mean foreigners would buy the debt of massively leveraged, mismanaged mortgage companies subject to constant political-cronyism, without some guarantee? Probably not. But then, it strikes me that a better way to attract foreign investment into the U.S. mortgage market is to deal with those issues, rather than paper over those problems with a taxpayer-funded guarantee.

It is also worth noting that when we most needed foreign support for the U.S. mortgage market, in 2008, foreign investors were dumping Fannie and Freddie debt in significant amounts. And obviously I think we’d prefer that the Chinese Central Bank stop using the purchase of Fannie and Freddie debt to depress the value of their own currency.