Going into 2020, the United States was in its 11th year of economic expansion and state governments were enjoying robust revenue and spending growth. Then COVID-19 hit and triggered a deep recession. State governments have seen their projected revenues decline and have started trimming spending to keep their 2021 budgets balanced. Some states had accumulated large rainy day funds and were prepared for the downturn, but other states have been overspending, accumulating debt, and saving little for the rainy day that has now arrived.

That is the backdrop to this year’s 15th biennial fiscal report card on the governors, which examines state budget actions since 2018. It uses statistical data to grade the governors on their tax and spending records—governors who have restrained taxes and spending receive higher grades, while those who have substantially increased taxes and spending receive lower grades.

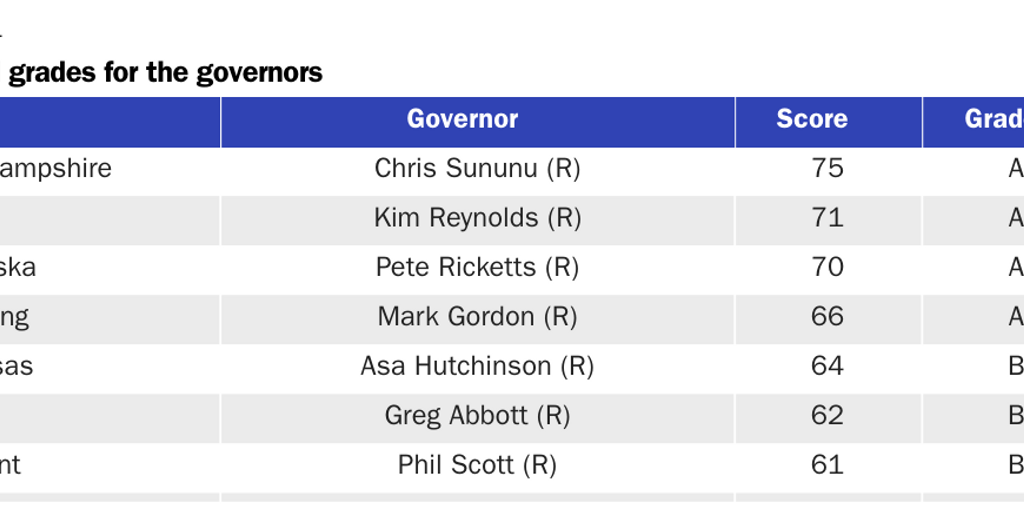

Four governors were awarded an A on this report: Chris Sununu of New Hampshire, Kim Reynolds of Iowa, Pete Ricketts of Nebraska, and Mark Gordon of Wyoming. Seven governors were awarded an F: Ralph Northam of Virginia, Andrew Cuomo of New York, Gretchen Whitmer of Michigan, Phil Murphy of New Jersey, J. B. Pritzker of Illinois, Kate Brown of Oregon, and Jay Inslee of Washington.

This report examines the widely varying tax and spending choices that governors have made in recent years. It discusses ways that states can respond to today’s budget challenges, including tapping revenues from marijuana legalization and cutting costs by prohibiting public-sector collective bargaining. The report also describes how states can prepare for future downturns by building large rainy day funds and creating stable and pro-growth tax bases.

With the 2020 health crisis and recession, governors across the nation are facing tough fiscal choices. However, the need for restraint and recovery provides an opportunity for governors to prune low-value spending from state budgets and to pursue growth-enhancing tax reforms.

Related Event

Focus on Fiscal Leadership: Release of the 2020 Fiscal Report Card on America’s Governors

Going into 2020, the United States was in its 11th year of economic expansion and state governments were enjoying robust revenue and spending growth. Then COVID-19 hit and triggered a deep recession, which has created new budget challenges for the nation’s governors. That is the backdrop to this year’s 15th biennial Fiscal Report Card on America’s Governors, which grades them based on their tax and spending policies. Please join us for a conversation with New Hampshire Governor Chris Sununu about this year’s report and the importance of fiscal restraint in state government.

Introduction

Governors play a key role in state fiscal policy. They propose budgets, recommend tax changes, and sign or veto tax and spending bills. When the economy is growing, governors can use rising revenues to expand programs or they can return extra revenues to the public through tax cuts. When the economy is stagnant and budget deficits appear, governors can respond by raising taxes or trimming spending.

This report grades governors on their fiscal policies from a limited-government perspective. Governors receiving an A are those who have cut taxes and spending the most, whereas governors receiving an F have raised taxes and spending the most. The grading mechanism is based on seven variables: two spending variables, one revenue variable, and four tax-rate variables. Cato has used the same methodology on its fiscal report cards since 2008.

The results are data-driven. They account for tax and spending actions that affect short-term budgets in the states. However, they do not account for longer-term or structural changes that governors may make, such as reforms to state pension plans. Thus, the results provide one measure of how fiscally conservative each governor is, but they do not reflect all the fiscal actions that governors make.

Tax and spending data for the report come from the National Association of State Budget Officers, the National Conference of State Legislatures, the Tax Foundation, the budget agencies of each state, and many news articles. The data cover the period January 2018 to August 2020, which was mainly a period of strong budget expansion before the recession began.1 The report rates 47 governors. It excludes the governors of Kentucky and Mississippi because they have been in office only a brief time, and it excludes the governor of Alaska because of peculiarities in that state’s budget.

The next section discusses the highest-scoring governors and some differences between the two political parties. After that, the report examines fiscal trends in the states, including spending growth rates and new sources of revenue that states are tapping.

Subsequent sections look at ways that states can reduce budget gaps during the current downturn and better prepare for future downturns. States can legalize and tax marijuana to raise revenues. States can end public-sector collective bargaining to reduce costs. States can begin building large rainy day funds when the economy returns to growth. And states can reform their tax codes to create stable revenue bases less susceptible to declines during recessions.

Appendix A discusses the methodology used to grade the governors. Appendix B provides summaries of the fiscal records of the 47 governors included in the report.

Main Results

Table 1 presents the overall grades for the governors. Scores ranging from 0 to 100 were calculated for each governor on the basis of seven tax and spending variables. Scores closer to 100 indicate governors who favored smaller-government policies. The numerical scores were converted to the letter grades A to F.

The following four governors received grades of A:

- Chris Sununu has led New Hampshire as governor since 2017 after a career as an engineer and business owner. Sununu has defended New Hampshire’s status as a low-tax state and kept general funding spending close to flat in recent years. While neighboring Massachusetts imposed a costly payroll tax to fund a new paid leave program, Sununu has twice vetoed such a plan in his state. He said a payroll tax is “an effective income tax,” which would “destroy the New Hampshire advantage.”2 Sununu also cut the rates of the state’s two main business taxes and defended the cuts from legislative efforts to undo them. The governor is proud that New Hampshire is top-rated on economic freedom and has worked hard to keep it that way.3

- Kim Reynolds was a state senator and lieutenant governor of Iowa before assuming office as governor in 2017. She has translated her stated beliefs in limited government and personal responsibility into fairly lean state budgeting and the pursuit of tax reform. She signed into law a major reform in 2018 that cut corporate and individual income tax rates, broadened online sales tax collections, and reduced taxes overall by more than $300 million a year. Reynolds proposed further tax-rate cuts in 2020, but the recession and health crisis have put those reforms on hold.

- Pete Ricketts is an entrepreneur and former corporate executive. Since taking office as Nebraska governor in 2015, he has pursued income tax reforms, fended off tax-increase proposals, and held general fund spending to 2.8 percent annual average growth. Ricketts signed into law an income tax cut in 2018 that will save Nebraskans more than $250 million a year. He has proposed further reforms to cut individual and corporate income tax rates and signed into law property tax relief legislation in 2020.

- Mark Gordon experienced the boom-bust pattern of Wyoming finances as state treasurer, and he now manages the state budget as governor since 2019. Even before the nationwide recession, Gordon began trimming state spending as revenues in the energy-dependent state fell. He has not supported efforts in the legislature to impose a corporate income tax, which would undermine Wyoming’s ability to rebuild its economy by attracting people and businesses as a haven free from income taxation.

All the governors receiving a grade of A in this year’s report are Republicans, and all the governors receiving an F are Democrats. There have been some high-scoring Democrats in past Cato fiscal reports, but Republican governors tend to focus more on tax cuts and spending restraint than do Democrats.

The biennial Cato report has used the same grading method since 2008. Republican and Democratic governors, respectively, have had average scores of 55 and 46 (2008), 55 and 47 (2010), 57 and 43 (2012), 57 and 42 (2014), 54 and 43 (2016), and 55 and 41 (2018).

The pattern continues in the 2020 report. This time, Republican and Democratic governors had average scores of 56 and 45. Republicans received higher scores than Democrats, on average, on both spending and taxes, although the Republican advantage on taxes was greater than on spending, which was also the case in prior reports.

When the economy is growing and state coffers are filling up, Democrats tend to increase spending, while Republicans tend to both increase spending and cut taxes. During economic downturns, Democratic governors often pursue tax increases to balance their budgets, while Republicans put greater focus on spending restraint. We will see whether that pattern holds as governors and legislatures face tough decisions as they work to close large budget gaps in the months ahead.

Related Event

Focus on Fiscal Leadership: Release of the 2020 Fiscal Report Card on America’s Governors

Going into 2020, the United States was in its 11th year of economic expansion and state governments were enjoying robust revenue and spending growth. Then COVID-19 hit and triggered a deep recession, which has created new budget challenges for the nation’s governors. That is the backdrop to this year’s 15th biennial Fiscal Report Card on America’s Governors, which grades them based on their tax and spending policies. Please join us for a conversation with New Hampshire Governor Chris Sununu about this year’s report and the importance of fiscal restraint in state government.

Fiscal Policy Developments

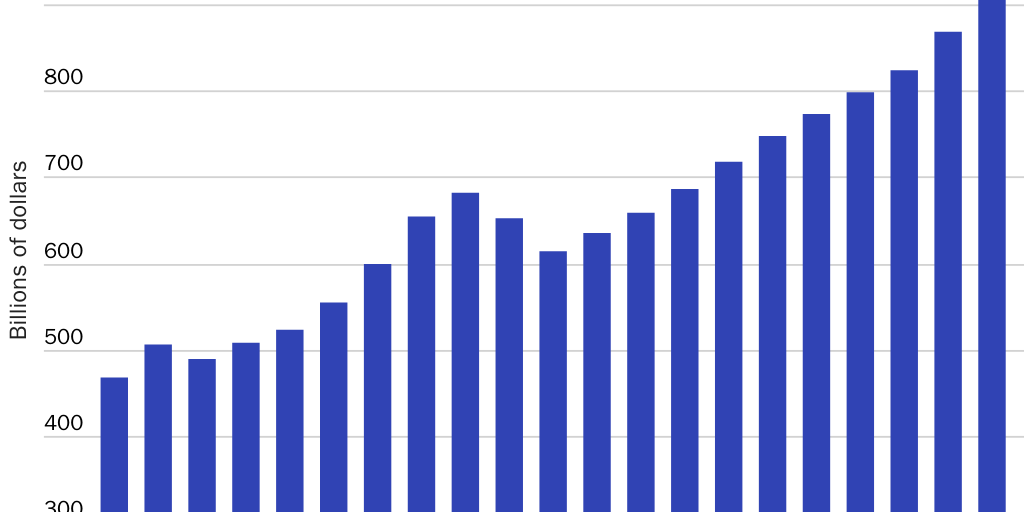

Figure 1 shows state general fund spending since 2000, based on data from the National Association of State Budget Officers (NASBO).4 After spending fell during the recession a decade ago, state budgets grew strongly until earlier this year. General fund spending grew at an annual average rate of 4.1 percent between 2010 and 2020, including increases of 5.5 percent in 2019 and 5.8 percent in 2020. The largest shares of general fund spending are for K–12 education (36 percent), Medicaid (20 percent), and higher education (10 percent).

NASBO’s most recent state survey in June found that the nation’s governors had proposed to increase spending in fiscal 2021 a combined 2.8 percent. We used the June data in this report because they are comparable across the states and reflect parallel actions taken by the governors in proposing budgets for the coming fiscal year. Note that for 46 of the 50 states, fiscal years run July to June.5

However, the recession has reduced projected revenues, prompting many states to adjust spending downward for 2021. Governors and legislators have begun taking tax and spending actions to rebalance their budgets and will continue to do so in coming months. During the last recession, states passed a slew of tax increases and they cut general fund spending 10 percent between 2008 and 2010.

A September survey of 37 states by the National Conference of State Legislatures found that revenues are estimated to be down 10 percent in 2021 compared with pre-crisis projections.6 Projections by the Tax Foundation and Tax Policy Center show similar projected declines.7 Note that the percentage declines would be less when compared with the 2019 revenue totals.

To relieve budget pressures, the states have started tapping their rainy day funds, and they have received hundreds of billions of dollars in emergency aid from the federal government. State policymakers should also cut spending and rescind planned spending increases. They should view the downturn as an opportunity to prune excesses after a decade of growth and to find ways to increase efficiency, as private businesses do during recessions.

Some states will likely pursue tax increases in coming months, as many states did during the last recession. Indeed, even during the recent expansion, state governments enacted net overall tax increases every year from 2016 to 2020.8 Cigarette tax increases have been popular with legislators, although the pace of increases has slowed as tax rates have reached high levels.9 Gasoline tax increases also continue to be popular with legislators, with 31 states increasing their rates since 2013.10

State governments are turning to new sources of revenue. Prior to 2018, businesses were generally not required to collect online sales taxes unless they had a physical presence in a customer’s state. But a U.S. Supreme Court ruling that year, South Dakota v. Wayfair, eliminated the physical presence rule, paving the way for states to aggressively expand sales tax collections from out-of-state, or remote, sellers. Nearly all states now require remote sales tax collections, although they have typically created a $100,000 exemption for sellers with limited sales in a state.11 Online sales are currently 16 percent of overall U.S. retail sales.12

A few states are considering “digital advertising taxes,” which would land on the estimated gross revenues of online advertisers in a state. Such taxes would be complex and are of dubious legality.13 Maryland Governor Larry Hogan vetoed such a tax earlier this year, which would have raised about $250 million.14 Policymakers in Nebraska and New York have also considered imposing these taxes.15

Gambling is a growing source of tax revenue. In 2018, the Supreme Court in Murphy v. National Collegiate Athletic Association overturned a 1992 federal law that had banned sports betting except in a few states.16 Today, at least 20 states have enacted laws allowing sports betting and taxing it.17 In 2020, for example, Michigan legalized sports betting and imposed a tax of 8.4 percent on gross betting receipts, and it also legalized internet gaming and imposed a tax on gross receipts of up to 28 percent.18 In July, Louisiana enacted a law allowing parishes to impose an 8 percent tax on the net revenue of online fantasy sports betting contests, which had recently been legalized.19

A growing number of states are mandating that private employers provide paid leave, including California, Connecticut, Massachusetts, New Jersey, New York, Oregon, Rhode Island, and Washington State.20 The new programs are all financed by payroll taxes on either employers or employees, but both approaches reduce after-tax wages over the long term. Three governors have signed these expensive programs into law since 2018—Ned Lamont of Connecticut, Charlie Baker of Massachusetts, and Kate Brown of Oregon—and their scores suffered on this report because of the large tax increases they imposed.

We take all tax actions into account in grading the governors in this report. Some actions broaden tax bases in sensible ways that improve neutrality, but governors should use the resulting revenue increases to reduce marginal tax rates and further improve economic efficiency. Revenue-neutral tax reforms that include reductions in top income and sales tax rates are scored favorably in this report.

In the following subsections, we discuss some of the tax and revenue options that state policymakers can pursue to balance their budgets during the current downturn, and we examine reforms to make state finances more stable over the longer term.

Legalize and Tax Marijuana

Recreational marijuana is now legal in Alaska, California, Colorado, Illinois, Maine, Massachusetts, Michigan, Nevada, Oregon, Vermont, Washington State, and the District of Columbia. Four other states—Arizona, Montana, New Jersey, and South Dakota—have measures on the ballot in November to legalize recreational marijuana. Virginia under Governor Ralph Northam decriminalized marijuana in 2020 and may soon legalize it.21 Rhode Island’s Governor Gina Raimondo has proposed legalizing marijuana in her state.22 In Canada, recreational marijuana has been legal since 2018.

One incentive for states to legalize marijuana is to raise tax revenues. Most of the states with legal recreational markets impose excise taxes on the retail price, which range from 10 percent to 37 percent.23 Numerous states impose taxes on growers, usually in addition to retail taxes. California, for example, imposes a 15 percent tax on the retail sales price plus taxes on growers based on plant weight. Illinois taxes marijuana based on THC content. Some states impose their regular retail sales taxes on top of these product-specific taxes.

Colorado has the longest experience with a legal recreational marijuana market. It imposes a 15 percent retail tax and a 15 percent wholesale tax on the product. In 2019, the state raised $263 million, which was 2.1 percent of the state’s general fund revenues.24 Total general fund revenues for the 50 states in 2020 were $913 billion, so if all states legalize recreational marijuana and raise relatively the same amount as Colorado, the total would be about $19 billion annually.25

However, states should be careful not to impose heavy taxes or regulations on marijuana because that would harm industry entrepreneurs, suppress government revenues, and encourage the survival of a large black market.26 Marijuana demand is responsive to taxation. One empirical study found that the “medium-run elasticity of demand for marijuana is higher than the consensus estimates for cigarettes or gasoline.”27 Unfortunately, a number of states appear to be imposing excessive taxes and regulations, and raising only a fraction of expected revenues while fueling black market sales.28

How should marijuana tax revenues be used? One option is to use them to reduce corporate income taxes, which are highly inefficient sources of revenue.29 Another option during the recession is to use marijuana tax revenues to help close state budget gaps. Then, as the economy recovers, states could channel marijuana taxes into rainy day funds to help prepare for the next downturn. If a state raised about 2 percent of its general fund revenues from marijuana taxes, it could build a hefty rainy day fund over the next economic expansion. Currently, Nevada’s 10 percent retail sales tax on marijuana goes into its rainy day fund, but other states use the revenues to fund new spending.30

The federal government should take steps to normalize marijuana markets by removing the product from the list of Schedule 1 drugs, legalizing interstate commerce in the product, allowing for normal banking transactions for the industry, and allowing marijuana businesses to deduct expenses on tax returns as other businesses do. By legalizing the industry, the federal government would help state governments convert black markets to normal markets and boost state tax revenues.

Ban Collective Bargaining to Cut Costs

The government workforce is heavily unionized. In 2019, 35 percent of state and local government workers were members of labor unions, which was far higher than the private-sector union share of 6 percent.31 Most public school teachers and a large majority of officers in big city police departments are covered by collective bargaining agreements.32

The union share in state and local government workforces varies widely—from less than 10 percent in North Carolina to 73 percent in New York.33 Union shares are related to state rules on collective bargaining. Three-quarters of the states have compulsory collective bargaining for at least some state and local workers, usually police, teachers, and firefighters.34 At the other end of the spectrum, North Carolina prohibits collective bargaining in government altogether, as did Virginia until recently.35 The rest of the states either prohibit collective bargaining in some parts of government or have no statewide mandates.

Union rules for public employees changed in 2018 when the U.S. Supreme Court decided Janus v. American Federation of State, County, and Municipal Employees (AFSCME). The court found that public employees cannot be forced to pay agency fees to a workplace union as a condition of employment. However, governments can still impose collective bargaining agreements, which are monopoly structures that restrict worker freedom and undermine efficiency and accountability.36

Government labor unions are in the spotlight in 2020 because of concerns about police misconduct. The killing of George Floyd by a Minneapolis police officer with a history of misconduct highlights how collective bargaining creates barriers to disciplining and firing bad officers. In the wake of Floyd’s killing, the mayor of Minneapolis said that the “elephant in the room” on police reform is “the police union, the contract associated with that union, and then the arbitration that ultimately is necessary.”37

Even when bad officers are fired, a Wall Street Journal analysis found that it is common under collective bargaining for arbitrators to reinstate them.38 In Minnesota, “officers who are fired for misconduct or charged with criminal behavior often end up back on the force,” the Journal found.39 Numerous studies have found that collective bargaining is associated with higher rates of police misconduct and with rules that undermine accountability.40 Similar problems are found in other unionized public-sector jobs. The layoff and firing rate of state and local workers is only about one-third the rate in the private sector.41

Labor unions also raise government costs, which policymakers should consider as they struggle to close budget gaps.42 Half of the $3 trillion in total state and local government spending in 2019 was for employee compensation, so cutting these costs would go a long way to balancing state budgets.43 Note that 29 percent of state spending consists of grants to local governments for schools and other activities, so labor cost savings in local governments would also reduce state government costs.44

In state governments nationwide, union member wages averaged 19 percent more than nonmember wages in 2019, while in local governments union wages averaged 30 percent more, according to the Bureau of Labor Statistics.45 However, the states and their workforces differ in numerous ways that should be accounted for in comparing union and nonunion compensation.

Kevin O’Brien analyzed police and fire department pay data across the country, and controlling for various factors he found that departments with collective bargaining paid about 13 percent higher wages.46 In another study, Bahman Bahrami, John Bitzan, and Jay Leitch found that unionized workers in local governments made about 15 percent higher wages than nonunionized workers in local governments, while unionized state workers made about 11 percent more.47

Sarah Anzia and Terry Moe studied the effects of collective bargaining on fire and police compensation.48 They found for the 1992 to 2010 period that collective bargaining increased wages for fire department employees by 9 percent and benefits by 25 percent, while collective bargaining increased wages of police department employees by 10 percent and benefits by 21 percent.

Finally, Thom Reilly and Mark Reed surveyed 134 large local governments after the last recession to see how collective bargaining had affected government budget gaps.49 They found that governments with collective bargaining were more likely to have raised compensation during the recession than other governments.

Aside from putting upward pressure on compensation, labor unions can raise costs by pushing for larger staffing levels, resisting the introduction of new technologies, and creating more rule-laden workplaces. Labor unions are also a lobby group inside government pushing for higher spending in general.

In a 2016 analysis, Heritage Foundation analysts using a variety of statistical methods found that states that had widespread collective bargaining for state and local employees spend $600 or more a year per capita than states that did not.50 This suggests that if, say, New York adopted North Carolina’s ban on collective bargaining, it would save about $10 billion a year, which is more than 10 percent of New York’s general fund budget.

When workers have a choice, they tend to reject unions, which is why unionization in the U.S. private sector has plunged from more than 30 percent in the 1950s to 6 percent today. In the public sector, labor union shares have declined in recent years in a few states, such as Michigan and Wisconsin, that have narrowed union powers.

In sum, state governments facing budget challenges should reduce costs by repealing collective bargaining in the public sector. Government workers should be free to join voluntary associations of teachers, police officers, and other professional groups. However, repealing collective bargaining would give government agencies the flexibility they need to reduce workforce spending in today’s tough budgeting environment.

Build Rainy Day Funds

Economic downturns are a blow to the private sector and to governments. As the sales, profits, and incomes of businesses and individuals fall, government tax revenues are undermined. While the federal government can easily increase borrowing when its tax revenues decline, state governments operate within statutory and constitutional rules that require them to balance their general fund budgets.51 When a recession hits, state governments often need to rebalance their budgets by raising taxes or reducing planned spending.

Another option for states during recessions is to tap their rainy day or budget stabilization funds. During boom years, the states typically save a portion of incoming tax revenues in such funds to be available in a downturn or crisis. All the states have rainy day funds, but they use a wide variety of rules and mechanisms for deposits into the funds and withdrawals.52 Large rainy day funds are viewed favorably by bond rating agencies, which boosts state credit ratings and reduces borrowing costs.53

Going into the recession in 2020, rainy day fund balances totaled 8.7 percent of annual general fund spending for the states as a whole, which is substantially higher than the 4.8 percent going into the last recession in 2008.54 Rainy day funds are a portion of “total balances,” which are the accumulated state funds left over after expenditures. Total balances are a broader cushion for state budgets, and they averaged 12.1 percent of annual spending going into this recession.

The size of rainy day funds varies widely. In 2020, they totaled 10 percent or more of annual spending in 20 states, but they totaled less than 5 percent in 12 states.55 Among these less-prudent states, New Jersey, Pennsylvania, Illinois, and Kansas had saved virtually nothing in their rainy day funds going into 2020, and that was after a decade-long economic expansion.

Some states learned a tough lesson from the recession a decade ago and adopted rules to beef up rainy day funds. California has a volatile tax base and suffered a 13.9 percent drop in state tax revenues in 2009 compared with the average drop across all states of 8.5 percent.56 A California government report noted, “The personal income tax is highly volatile, which has in the past led to large increases in spending in good economic times and the need to make large cuts in bad economic times.”57 California voters recognized the problem and approved a ballot question in 2014 (Proposition 2) that created a more robust structure for the rainy day fund.58 The report noted the double advantage of rainy day funds: “Proposition 2 takes volatile revenues off the table in good economic years so that they can be used to reduce the need for cuts in bad economic years.”59 The California rainy fund grew from 4.6 percent of annual spending in 2014 to 13.7 percent by 2020.60 The state is in a better place today both because the reserve fund is available during the crisis and because additions to the fund during the boom years reduced spending.

Energy-producing states have also learned from experience. Those states tend to have boom-bust economies and rely on severance taxes (on resource extraction) for revenues, which makes governments vulnerable. Alaska, North Dakota, Texas, and Wyoming knew their vulnerability to downturns, planned ahead, and went into 2020 with robust rainy day funds.

In recent months, states have begun taking actions to rebalance their budgets for 2021, including freezing hiring, reducing wage increases, and postponing new initiatives. Many states have also begun tapping their rainy day funds. States that were prudent and built large rainy days will have an easier time budgeting over the next year or two. This year’s crisis shows that states should plan ahead because recessions usually happen without warning.

Reform Taxes to Increase Stability

State governments raised $1.09 trillion in tax revenues in 2019. Individual income taxes were 38 percent of the total, general sales taxes were 31 percent, selective sales taxes were 16 percent, corporate income taxes were 5 percent, and other taxes were 10 percent.61 To reduce the boom-bust pattern in their budgets as the economy fluctuates, state policymakers should move toward sources of tax revenue that are more stable across cycles.

Income tax revenues are generally more volatile than sales tax revenues.62 During the last recession, from 2007 to 2009, state personal income tax revenues fell 12 percent, state corporate tax revenues fell 18 percent, and state sales and excise tax revenues fell 6 percent.63

An Urban Institute study looking at state revenues over recent decades found that “the corporate income tax tends to be the most volatile source of tax revenue; the personal income tax, which includes the highly unpredictable capital gains tax, is a close second.”64 A related problem is that forecasts of future income tax revenues are more error-prone than forecasts of sales tax revenues, and thus more problematic for states in planning their budgets.65

Examining state data from 1994 to 2019, economists Christos Makridis and Robert McNab estimated that a 1 percentage point change in employment changes sales taxes 1.19 percentage points, individual income taxes 1.63 percentage points, and corporate income taxes 4.13 percentage points.66

The Urban Institute study noted that states have become more dependent on volatile revenue sources since the 1970s as the share of revenues from income taxes has risen and the share from sales taxes has fallen.67 A Federal Reserve study noted the same, and it also found that within the income tax base, investment income (dividends, interest, and capital gains) is more volatile than wage income.68 In New York State, for example, “personal income tax volatility is attributable largely to the volatility of capital gains—a major source of income for top earners.”69

Progressive personal income taxes that have higher rates on top earners can be more volatile than proportional or flat-rate systems. That is because a large share of top incomes is investment and business income, which fluctuates strongly with economic ups and downs. During the last recession, federal adjusted gross income of the top 1 percent of highest earners fell 34 percent between 2007 and 2009, compared with a 6 percent drop in adjusted gross income for the other 99 percent of taxpayers.70

The volatility of high-end incomes creates major problems for states that have progressive income tax structures. In California, the top 1 percent pays about 50 percent of state income taxes.71 In 2019, income taxes accounted for 61 percent of California’s overall state tax revenue, so when the investment and business income of the top 1 percent drops, it generates a major budget crisis.

In 2009, California’s personal income tax revenues plunged 20 percent compared with a 9 percent fall in the other 49 states.72 California’s top personal income tax rate of 13.3 percent is the highest in the nation. An analysis by California’s legislature found that the state’s personal income tax revenues are about five times more volatile than overall personal income because of the income tax system’s progressive rate structure and other tax design features.73 Within income taxes, capital gains taxes are particularly volatile.74

Pew Charitable Trusts examined tax revenue volatility between 1998 and 2017 and found that California had the fifth highest volatility among the 50 states.75 The three states with the most volatile tax revenues were energy producers that rely heavily on severance taxes. The state with the least volatility according to Pew was South Dakota, which does not have a personal income tax and relies on sales taxes for 83 percent of state tax revenues.76 During the last recession, South Dakota’s total state tax revenues dipped less than 2 percent and then started rising again.

Governor J. B. Pritzker spearheaded the effort to put a question on the Illinois ballot in November 2020 to change the state constitution and replace the state’s single-rate 4.95 percent individual income tax with a system with six rates topping out at 7.99 percent.77 An Illinois think tank modeled how this multirate system would have performed in previous years and found that it would have produced substantially more volatile revenues than a flat-rate system.78

To increase tax stability, states should transition away from individual and corporate income taxes and rely more on general retail sales taxes. It is true, however, that the current recession is somewhat different than past recessions because of the direct hit to retail sales created by virus-related business shutdowns. For 2021, the Tax Policy Center estimated that sales tax revenues will fall about the same percentage as individual income tax revenues, although the Tax Foundation estimated that income tax revenues would fall more.79 Corporate tax revenues are very likely to fall more sharply than either individual income tax or sales tax revenues.

Aside from being a generally more stable revenue source, sales taxes are less harmful to economic growth than income taxes because they do not create a tax bias against saving and investment.80 The Tax Cuts and Jobs Act of 2017 (TCJA) created a further incentive to move away from individual income taxes, particularly systems with progressive structures. The law capped the federal deduction for state and local taxes at $10,000, which increased taxes on many middle and higher earners living in high-tax states. The reform means that millions of households have more of an incentive to move to lower-tax states. As explored in a separate Cato study, state policymakers should rethink their tax codes because of today’s heightened interstate tax competition.81

In sum, corporate income taxes and high-rate individual income taxes make less sense than sales taxes because of the greater volatility, larger economic harm, and increased threat from tax-driven interstate mobility.

Appendix A: Report Card Methodology

This study computes a fiscal policy grade for each governor based on his or her success at restraining taxes and spending since 2018, or since 2019 for governors who entered office that year. The spending data used in this study come from NASBO and, in some cases, from the budget documents of individual states. The data on proposed, enacted, and vetoed tax changes come from NASBO, the National Conference of State Legislatures, state budgets, and news articles.82 Tax rate data come from the Tax Foundation and other sources.

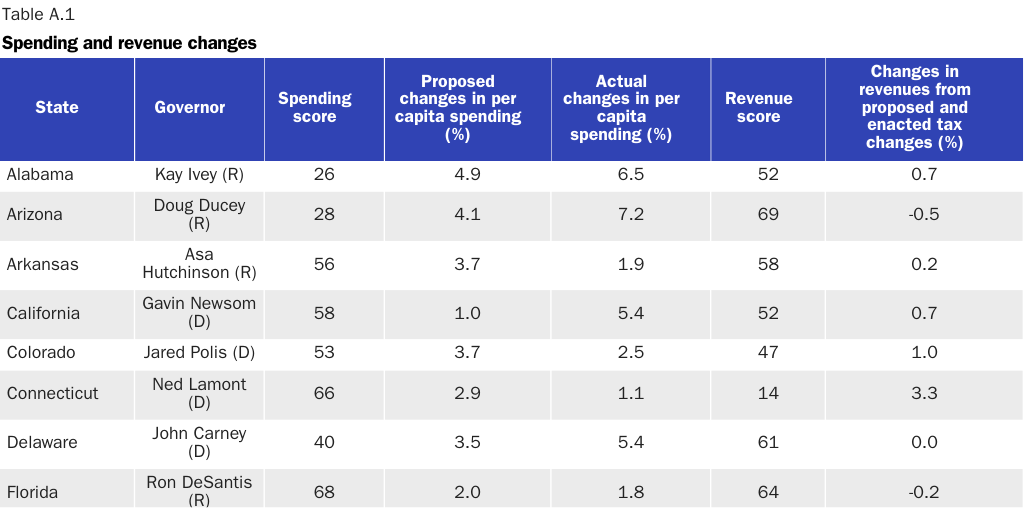

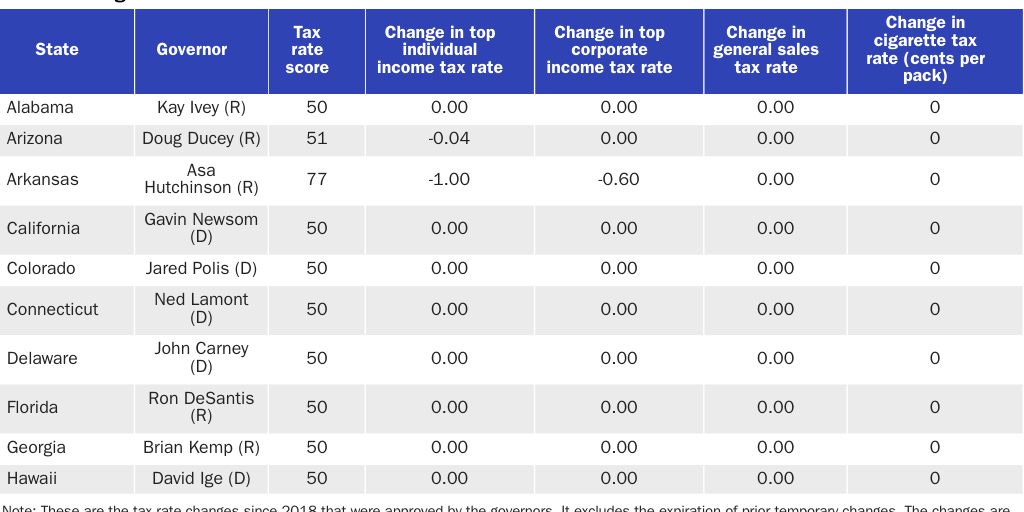

This year’s report uses the same methodology as the 2008, 2010, 2012, 2014, 2016, and 2018 Cato fiscal reports. The report focuses on short-term taxing and spending actions to judge whether governors take a small-government or a big-government approach to fiscal policy. Each governor’s performance is measured using seven variables: two for spending, one for revenue, and four for tax rates. Their overall score is calculated as the average of their scores in these three categories. Tables A.1 and A.2 summarize the governors’ scores.

Spending Variables

- Average annual percent change in per capita general fund spending proposed by the governor

- Average annual percent change in per capita general fund spending enacted

Revenue Variable

- Average annual dollar value of proposed, enacted, and vetoed tax changes. This variable is measured by summing the reported estimates of the annual dollar effects of tax changes as a percentage of a state’s total tax revenues. For example, vetoing a $50 million tax increase would boost a governor’s score the same amount as signing into law a $50 million tax cut. This is an important variable, and it is compiled from many news articles, budget documents, and reports.83

Tax Rate Variables

- Change in the top personal income tax rate approved by the governor

- Change in the top corporate income tax rate approved by the governor

- Change in the general sales tax rate approved by the governor

- Change in the cigarette tax rate approved by the governor

The two spending variables are measured on a per capita basis to adjust for state populations that are growing at different rates. Also, the spending variables measure only the changes in general fund budgets, which is the portion of state budgets that governors have most control over. Variable 1 is measured through fiscal year 2021 and variable 2 is measured through fiscal 2020. Variables 3 through 7 cover changes from January 2018 to August 2020, or from January 2019 to August 2020 for governors who entered office in 2019.

For each variable, the results are standardized so that the worst scores are near 0 and the best scores are near 100. The scores for each of the three categories—spending, revenue, and tax rates—are calculated as the average score of the variables within the category, with one exception: the cigarette tax rate variable is quarter-weighted because that tax is a smaller source of state revenue than the other taxes measured in its category. The average of the scores for the three categories produces the overall grade for each governor.

Measurement Caveats

This report uses publicly available data to measure the fiscal performance of the governors from a small-government perspective, but there are imprecisions in such grading. The report cannot fully isolate the policy impact of governors from state legislatures, but to help separate the impact, variables 1 and 3 measure the effects of each governor’s proposed, although not necessarily enacted, policies.

Another factor to consider is that the states grant governors differing amounts of authority over budget processes. For example, most governors can use a line-item veto to trim spending, but some governors do not have that power. Another example is that the supermajority voting requirement to override a veto varies among the states. Such factors give governors different levels of budget control that are not accounted for in this study.

Nonetheless, the results presented here should reflect each governor’s fiscal approach. Governors who received a grade of A have focused on reducing tax burdens and restraining spending. Governors who received a grade of F have pursued government expansion. In the middle are many governors who oscillate between different fiscal approaches from one year to the next.

Appendix B: Fiscal Notes on the Governors

This section discusses the fiscal records of the 47 governors covered in the report. The discussions are based on the tax and spending data used to grade the governors as well as other information that sheds light on each governor’s fiscal approach. All spending data discussed are from NASBO unless otherwise noted.84 The grades are calculated based on each governor’s record since 2018, or since 2019 if that year was the governor’s first in office.

Alabama

Kay Ivey, Republican

Legislature: Republican

Grade: D

Took office: April 2017

Kay Ivey has been in Alabama government a long time. She was a reading clerk in the Alabama House of Representatives, an assistant director of the Alabama Development Office, the state treasurer, and the lieutenant governor. She was sworn in as governor in 2017 after the resignation of her predecessor, Robert Bentley, in a scandal.

Running for a full term in 2018, Ivey said she opposed tax increases.85 Nonetheless, Ivey has raised some taxes, including by signing a bill in 2019 increasing Alabama’s gas tax by 10 cents per gallon.

Ivey scored poorly on spending in this report. General fund spending increased 4.1 percent in 2019 and 9.7 percent in 2020. Ivey initially proposed a 6.5 percent spending increase for 2021, although the enacted increase was lower. Ivey has supported large increases in the state education budget but has opposed expanding Medicaid under the Affordable Care Act (ACA).86

Arizona

Doug Ducey, Republican

Legislature: Republican

Grade: D

Took office: January 2015

Doug Ducey has a background in business and finance and was the head of Cold Stone Creamery. Ducey has pro-market instincts on many policy issues. He has approved occupational licensing reforms, placed a moratorium on new regulatory rulemaking, and pushed back against minimum wage increases. However, Ducey scores poorly on this report because of large spending increases.

General fund spending increased 6.6 percent in 2019, and Ducey proposed increasing spending 8.7 percent for 2020, including spending on more than half a billion dollars of “new initiatives.”87 Ultimately, the governor approved an 11.5 percent spending increase for 2020.

Ducey has approved numerous tax cuts, including ending sales taxes on some business purchases, reducing insurance premium taxes, and indexing income tax brackets for inflation. In 2019, he signed into law income tax reductions that conformed the state’s tax code to changes in the 2017 federal Tax Cuts and Jobs Act, while increasing the standard deduction, reducing the number of tax brackets, and trimming income tax rates. In 2020, Ducey called for eliminating taxes on military pensions.

Ducey has also increased taxes. The governor approved an extension of a sales tax surcharge to fund education in 2018.88 He also imposed a new vehicle registration fee on Arizona drivers. The Arizona Capitol Times noted, “Ducey, who promised not to raise taxes while in office, maintains that it is a fee and not a tax,” but that is a distinction with little difference.89

Arizonans are scheduled to decide on a ballot initiative in November (Proposition 208) that would raise income taxes 3.5 percentage points on high earners.90 Ducey opposes the increase. Arizona voters will also have an opportunity to vote for Proposition 207, which would legalize and tax recreational marijuana. Ducey also opposes this measure.

Arkansas

Asa Hutchinson, Republican

Legislature: Republican

Grade: B

Took office: January 2015

Former U.S. congressman and federal official Asa Hutchinson entered the governor’s office in 2015. He campaigned on tax cuts and has delivered.91 The governor said in 2015, “Arkansas has been an island of high taxation for too long, and I’m pleased that we are doing something about that.”92

Hutchinson approved income tax cuts in 2015 and 2017, mainly for lower- and middle-income taxpayers. In 2018, Hutchinson proposed further cuts including reducing the top individual income tax rate and offsetting the revenue losses with budget surpluses and closing narrow tax breaks.

In 2019, Hutchinson approved a series of tax reforms. The top individual income tax rate was cut from 6.9 percent to 6.6 percent, and the rate is scheduled to fall to 5.9 percent in 2021.93 Six income tax brackets were consolidated into four. The corporate income tax rate is set to fall from 6.5 percent to 6.2 percent in 2021 and then to 5.9 percent in 2022.94 The savings for taxpayers were partly offset in 2019 by a gas tax increase and base broadening in the sales tax.

California

Gavin Newsom, Democrat

Legislature: Democratic

Grade: C

Took office: January 2019

Gavin Newsom is a former lieutenant governor of California and mayor of San Francisco. Newsom received a middling grade, but he did better than prior governor Jerry Brown who scored poorly on past Cato fiscal reports. The pace of spending growth has fallen under Newsom, compared with the 13.7 percent increase in Brown’s final year. In Newsom’s first year as governor, general fund spending increased 5.6 percent.

Newsom raised business taxes by more than $1 billion in 2019, including by limiting loss deductions. He signed into law additional large business tax increases in 2020, including sharply limiting the use of business tax credits and loss deductions for three years.95 Imposing higher taxes on businesses during a recession is the wrong way to revive growth and get Californians back to work.96

Rather than raising taxes, California should reform its tax system to create greater revenue stability. During the last recession, state tax revenues fell 13.9 percent in 2009 compared with the average drop across all states of 8.5 percent.97 A California government report noted, “The personal income tax is highly volatile, which has in the past led to large increases in spending in good economic times and the need to make large cuts in bad economic times.”98 One problem is that the state’s top 1 percent of earners pay about 50 percent of all state income and capital gains taxes, but these tax revenues are highly variable.99 California should move toward greater reliance on sales taxes and less reliance on income and capital gains taxes.

Fortunately, California entered the current recession in a better position than the last one. In 2014, voters approved Proposition 2, which created a more robust funding structure for the state’s rainy day fund. The rainy day fund balance has grown from 4.6 percent of annual spending in 2014 to 13.7 percent by 2020.100

In November, voters will decide on a ballot initiative to raise taxes on commercial properties. If passed, the initiative (Proposition 15) will amend the state constitution to impose property taxes on commercial and industrial properties above $3 million in value using current market prices rather than purchase prices adjusted by a capped annual growth rate. The change would raise taxes up to $12 billion per year.101 In September, the governor endorsed the huge tax hike, although this action came too late to be scored in this report.

Colorado

Jared Polis, Democrat

Legislature: Democratic

Grade: C

Took office: January 2019

Jared Polis is a former U.S. House member from Colorado. He has a reputation as a moderate Democrat, and he scores about average on taxes and spending in this report.

General fund spending increased 3.7 percent in 2020, with the budget including initiatives to streamline programs and beef up the rainy day fund. The budget for 2021, passed in June, trims general fund spending by 3 percent and relies on one-time measures and tax increases to close a substantial budget gap.102

Polis has taken varying positions on the state’s Taxpayer Bill of Rights (TABOR), which includes a mechanism that distributes surplus revenues back to taxpayers. In 2019, Polis supported retaining excess revenues and using them to boost spending on education and highways. However, voters rejected that idea at the ballot box in November 2019 (Proposition CC).103

Conversely, Polis celebrated a TABOR-triggered tax cut that temporarily reduced the individual income tax rate from 4.63 percent to 4.5 percent. He said, “As governor, I hope to deliver an economy next year and the years beyond that produces tax cut refunds more regularly.”104 Polis says that he supports reforming the tax code by eliminating loopholes and reducing income tax rates.

In 2020, Polis approved a bill (HB 1420) that increased business taxes, despite TABOR’s requirement that voters need to approve tax increases.105 Polis compromised on a version of the bill that will raise taxes about $100 million in 2021 after opposing a larger tax increase favored by Democrats in the legislature.106

Polis is also supporting an initiative on the November 2020 ballot to increase taxes on tobacco. If approved, the measure will phase in a cigarette tax increase of $1.80 per pack and raise $450 million over the first two and a half years.107 Colorado voters rejected a tobacco tax increase at the ballot box in 2016 (Amendment 72).

Colorado voters will have a chance to vote on a tax cut in November 2020. If approved, Initiative 306 on the ballot would cut the state’s flat individual and business income tax rate from 4.63 percent to 4.55 percent.

Connecticut

Ned Lamont, Democrat

Legislature: Democratic

Grade: D

Took office: January 2019

Ned Lamont is a former cable television executive who has been active in state politics for years, including a failed run against Joe Lieberman for the U.S. Senate in 2006. Lamont’s poor grade of D matches the poor grades of his predecessor, Dan Malloy, who never scored above a D on prior Cato fiscal reports.

Lamont scored well on spending but very poorly on taxes. Connecticut’s economy has been sluggish for years, and with slow revenue growth Lamont and the legislature have had to restrain spending. Adding to Connecticut’s problems is that pension and debt servicing costs “eat up nearly 30% of the General Fund—about three times what they consume in other state budgets.”108

Lamont has opposed raising individual income tax rates, which is wise because Connecticut has been losing high-earning households to other states for years. Internal Revenue Service (IRS) data show that the state loses four taxpayers earning more than $200,000 to other states for every three that it gains.109

However, Lamont signed into law a mandatory paid leave program in 2019 that imposes a new wage tax on private employers in the state. The tax will raise more than $400 million a year beginning in 2021.110 Lamont has approved numerous other tax increases, including extending an expiring corporate tax surcharge, increasing taxes on prepared foods, broadening the sales tax base, and imposing taxes on plastic bags. He also proposed higher sales taxes from broadening the tax base and a new tax on soda that would have raised about $160 million a year.111

Lamont has voiced his support for legalizing and taxing marijuana. In his 2020 state of the state address, he said, “like it or not, legalized marijuana is a short drive away in Massachusetts and New York is soon to follow.”112 He said he would support a proposal to legalize the drug and impose “a fair tax structure that will provide meaningful new state and municipal revenues.”113

Delaware

John Carney, Democrat

Legislature: Democratic

Grade: C

Took office: January 2017

John Carney has had a long political career. Before entering office as governor, he was a member of the U.S. Congress, Delaware’s lieutenant governor, and Delaware’s secretary of finance. He also served on the staff of Joe Biden in the U.S. Senate.

On the last Cato fiscal report, Carney scored a D because of his support for tax increases, including increases on corporations, alcohol, and cigarettes. Carney also proposed a plan to raise individual income taxes, but that plan did not pass.

Carney has been more restrained on the tax front in recent years and only a few small tax changes have passed, thus boosting the governor’s score on this report. However, Carney scored poorly on spending. Delaware’s general fund budget rose 6.7 percent in 2019 and 6.3 percent in 2020.

Florida

Ron DeSantis, Republican

Legislature: Republican

Grade: B

Took office: January 2019

Ron DeSantis served in the U.S. House from 2013 to 2018. His predecessor in the governor’s office, Rick Scott, earned high grades on prior Cato fiscal reports, and DeSantis has continued Florida’s fiscally conservative record.

DeSantis has been a lean budgeter. General fund spending rose just 3 percent in 2020, and in response to the recession this year, DeSantis vetoed $1 billion in spending from the legislature’s original 2021 budget.114

DeSantis scored above average on taxes because of his support of numerous modest tax cuts. He signed legislation to extend a corporate tax cut that reduced the rate from 5.5 percent to 4.5 percent, and he approved a bill to avoid business tax increases related to changes in the federal TCJA. The governor has approved other breaks including sales tax holidays and a reduction in the state tax rate on commercial leases.

Georgia

Brian Kemp, Republican

Legislature: Republican

Grade: B

Took office: January 2019

Brian Kemp is an entrepreneur who has owned and invested in companies involved in agriculture, banking, manufacturing, and real estate. He was a state senator from 2003 to 2007 and Georgia’s secretary of state from 2010 to 2018.

Kemp scored highly on spending in this report. Even with the growing economy last year, Kemp issued a directive for state agencies to come up with substantial budget cuts, saying, “I have instructed all state government offices to reduce expenditures and streamline operations through proactive leadership. By reducing waste and ending duplication in government, we can keep Georgia the best place to live, work, and raise a family.”115 The Atlanta Journal-Constitution noted, “Georgia’s economy is still growing, but state agencies will have to look for ways to cut their budgets under a directive the Kemp administration sent out Tuesday. It is the first time budget cut proposals have been requested from agencies since the state was hammered by the aftereffects of the Great Recession nearly a decade ago.”116

With this leadership, Kemp was able to restrain general fund budget growth to just 1 percent in 2020. That restraint has put the state in a better position this year because the recession has reduced available revenues. In June, Kemp announced that the 2021 budget will contain substantial across-the-board spending reductions.117

Regarding state revenues, Kemp expressed concern about scheduled reductions to the individual income tax rate, and the cut has been put off for now. The rate was cut from 6.0 percent to 5.75 in 2018 and was scheduled to fall to 5.375 percent in 2021.118

Hawaii

David Ige, Democrat

Legislature: Democratic

Grade: D

Took office: December 2014

David Ige pulled up his grade to a D this year after earning an F on the last Cato fiscal report. Prior to entering the governor’s office, Ige was a state legislator and a manager in the telecommunications industry.

In his first few years in office, Ige proposed and signed into law increases in income taxes, sales taxes, gas taxes, hotel room taxes, and other charges. Since 2018, Ige has both raised taxes and vetoed tax increases. He approved a bill that created a higher estate tax rate bracket for the largest estates, and he also increased travel-related taxes.

In 2019, Ige vetoed two bills that would have raised taxes more than $50 million annually. One would have increased taxes on real estate investment trusts, which Ige argued would have discouraged investment. The other would have raised taxes on vacation rentals such as Airbnb.

Hawaii’s general fund spending rose a hefty 5.7 percent in 2020, thus reducing the governor’s score in this report.

Idaho

Brad Little, Republican

Legislature: Republican

Grade: C

Took office: January 2019

Brad Little had a career in ranching, and he has served as state senator and Idaho’s lieutenant governor.

Little received a C on this report. His grade was pushed down by a 7 percent increase in general fund spending in 2020. In 2018, Medicaid expansion was approved by voters at the ballot box as Proposition 2. At the time, Little took no position on the matter even though he was running for governor, and since expansion passed he has enthusiastically supported it.119

On taxes, Little has supported both cuts and increases, including expanding online sales taxes. Recently, Little and state legislators used $200 million of federal coronavirus relief funds to pay for local property tax cuts, which illustrates how states did not need some of the crisis-related cash they received from Washington.120

Illinois

J. B. Pritzker, Democrat

Legislature: Democratic

Grade: F

Took office: January 2019

Billionaire J. B. Pritzker has been long involved in Democratic politics and is a member of the family that owns the Hyatt hotel chain. Governor Pritzker earns one of the lowest grades on this study due to his large tax increases.

Pritzker signed into law $2.7 billion in net annual tax increases last year. He increased the gas tax from 19 cents to 38 cents per gallon, hiked vehicle registration fees, increased the cigarette tax from $1.98 per pack to $2.98, and expanded online sales taxes. One good move, however, was enacting a phaseout of the state’s corporate franchise tax, which is an unneeded burden on businesses in addition to the state’s corporate income tax.

The big issue looming for Illinois taxation is whether voters this November will amend the state constitution to convert the state’s flat individual income tax to a multirate (progressive) system. Pritzker is pushing hard in favor of the change.

The current income tax has a flat rate of 4.95 percent, and, if the amendment passes, legislation is in place to replace it with a six-rate system with a top rate of 7.99 percent. The plan to increase taxes on higher earners threatens to erode the tax base as people move out of Illinois to lower-tax states. IRS data show that Illinois loses two taxpayers earning more than $200,000 per year to other states for each one moving in.121

The tax-increase plan would also raise the corporate income tax rate from 9.5 percent to 10.49 percent.122 Overall, the individual and corporate income plans would raise taxes by an enormous $3.9 billion a year.123

Even with all the state’s budget woes—including high debt, unfunded obligations, and the lowest bond rating in the nation—Pritzker’s 2021 budget proposed to increase general fund spending by 5.7 percent. Funding for the budget partly depends on borrowing funds from a Federal Reserve emergency program, which would put the state even further into debt.

Indiana

Eric Holcomb, Republican

Legislature: Republican

Grade: B

Took office: January 2017

Eric Holcomb entered office in 2017 after a career in the U.S. Navy and numerous public positions, including being an adviser to former Indiana governor Mitch Daniels.

Holcomb scored poorly on the 2018 Cato fiscal report, mainly because of his support for tax increases. In 2017, he signed a transportation bill that increased the state’s gas tax from 18 cents to 28 cents per gallon and imposed new fees on vehicle owners. Since then, Holcomb has approved further modest tax increases, including expanding taxes on online sales.

However, Holcomb scored well on spending. He has proposed lean budgets, and general fund spending rose an average of just 3.4 percent annually the past two years.

Iowa

Kim Reynolds, Republican

Legislature: Republican

Grade: A

Took office: May 2017

Kim Reynolds started her career in public service as a county treasurer. She also served as a state senator and lieutenant governor of Iowa, and then became governor after Terry Branstad stepped down to become the U.S. Ambassador to China.

Reynolds says that her politics are based on the ideas of limited government, personal responsibility, and individual initiative.124 As governor, she has translated those beliefs into fairly lean budgeting and the pursuit of tax reform, earning her the second highest score on this report.

Reynolds signed into law a major tax reform in 2018. The legislation cut the top individual income tax rate from 8.98 percent to 8.53 percent. Contingent on revenue goals being met, the legislation drops the top rate to 6.5 percent in 2023 and collapses a nine-bracket system to four brackets. The law also cuts the top corporate income tax rate from 12 percent to 9.8 percent starting in 2021, while raising revenue from broadening online sales taxes. All in all, the cuts will initially save Iowans about $300 million a year and then rising amounts after that.125

In January 2020, Reynolds proposed a second round of tax reforms that would raise the retail sales tax rate by 1 percentage point and use the revenues to further cut income tax rates across the board. The reform would have amounted to a small overall tax reduction and would bring the top individual income tax rate down to 5.5 percent by 2023. Shifting away from a high-rate income tax to sales taxation would enhance revenue stability and support economic growth.

Unfortunately, the recession has shelved Reynolds’ latest tax reform plan for now, as Iowa policymakers have changed their focus to spending restraint and the health crisis.126

Kansas

Laura Kelly, Democrat

Legislature: Republican

Grade: D

Took office: Jan 2019

Laura Kelly served as the executive director of the Kansas Recreation and Park Association and has worked in mental health services. She served in the Kansas Senate and was the ranking member on the Ways and Means Committee.

Kelly came into the governor’s office saying that she would stabilize the budget after her predecessor, Sam Brownback, had “wrecked” it.127 Yet in her first year in office, Kelly oversaw a huge increase in general fund spending of 10.3 percent, which included increases on education, public safety, and infrastructure.128 Those increases were ill-timed because the economic downturn in 2020 has made her program expansions less affordable. To rebalance the budget this year, Kelly has proposed to delay debt payments, use federal aid, and pursue one-time spending cuts.129

The 2017 federal tax reform (the TCJA) broadened the income tax base and boosted state revenues in states such as Kansas that automatically conform to changes in the federal code.130 Republicans in the legislature called for offsetting the higher state tax revenues with adjustments to the Kansas tax code. But Kelly has resisted these measures, and she twice vetoed bills to offset the tax increases, even though she had campaigned in 2018 promising not to raise taxes.131

Louisiana

John Bel Edwards, Democrat

Legislature: Republican

Grade: C

Took office: January 2016

John Bel Edwards is a graduate of the U.S. Military Academy at West Point, and he served eight years with the U.S. Army as an airborne ranger. Edwards also served in the state legislature before being elected governor in 2015.

Edwards scored an F on the last Cato fiscal report because of his support for large tax increases, including a higher sales tax rate and higher taxes on alcohol, cigarettes, health care providers, vehicle rentals, and other items. In 2017, Edwards proposed a new gross receipts tax for the state, but fortunately the legislature shot that idea down.132

Edwards signed into law an extension of a higher sales tax rate in 2018, and he has approved an expansion in online sales tax collections. In July, Edwards approved a range of narrow business tax breaks designed to aid recovery from the recession.

Maine

Janet Mills, Democrat

Legislature: Democratic

Grade: D

Took office: January 2019

Janet Mills served as attorney general for Maine before running for governor in 2018. Mills has a tough act to follow because her predecessor, Paul LePage, earned an A all four times he was graded on the Cato fiscal report.

Governor Mills scores poorly because of her support for substantial spending increases. The general fund budget rose 5.8 percent in 2020, with large increases for education and health care. On her first day in office, Mills approved the expansion of Medicaid under the ACA, which LePage had resisted agreeing to. Medicaid expansion will cost about $146 million over the first two years.133

Maryland

Larry Hogan, Republican

Legislature: Democratic

Grade: C

Took office: January 2015

Larry Hogan has enjoyed high favorability ratings in polls, and he has nudged Democrats in the legislature toward tax relief. Hogan scores well on taxes but poorly on spending.

Hogan has signed into law numerous modest tax cuts and resisted tax increases pursued by the legislature. In 2018, Hogan approved tax cuts to offset automatic tax increases created by the federal TCJA. In 2020, he proposed eliminating income taxes for retirees earning less than $50,000 and cutting taxes for retirees earning less than $100,000. Hogan noted: “We’re losing many of our best citizens.… People who have been lifelong Marylanders, who have contributed so much and still have so much to offer, are moving to other states for one simple reason: our state’s sky-high retirement taxes.”134 Hogan is correct that Maryland is, on net, losing seniors to other states.135

Hogan has vetoed a number of tax hikes passed by the legislature, including a new digital advertising tax and a $1.75 per pack increase in cigarette taxes. The downside of Hogan’s tax policy approach is that he favors narrow breaks for individuals and businesses rather than pursuing major reforms aimed at simplifying the tax base and reducing overall rates.136

Hogan’s grade was dragged down by his spending increases. Maryland general fund spending increased 9.7 percent in fiscal 2020. Much of the increased spending has gone to education and Medicaid expansion.

Massachusetts

Charlie Baker, Republican

Legislature: Democratic

Grade: D

Took office: January 2015

After a career in the health care industry and state government, Charlie Baker was elected governor in 2014. He scored poorly on this report mainly because of his support for a large payroll tax to fund a new paid leave program.

In originally running for office, Baker said that he would not raise taxes, but he has broken that promise many times. Baker signed into law a tax on short-term rentals, such as Airbnb, and he has approved increases in online sales taxes. He has proposed increasing taxes on ride-sharing services, such as Uber. And in 2020, Baker proposed “real-time” sales tax remittance to boost state revenues $300 million while raising compliance costs on businesses.137

Baker’s largest tax increase came in July 2018, when he approved a 0.63 percent payroll tax on private employers to fund a new paid leave benefit.138 The law increased taxes on workers in the state by $750 million or more a year.139

Michigan

Gretchen Whitmer, Democrat

Legislature: Republican

Grade: F

Took office: January 2019

Gretchen Whitmer served in the Michigan House and the Michigan Senate before being elected governor in 2018. Whitmer scores poorly on this report because of her support for large tax increases.

When campaigning in 2018, Whitmer “scoffed at the idea” that she supported a gas tax hike in a televised debate, calling the accusation “ridiculous.”140 Despite that dismissal, Whitmer pushed hard for a gas tax increase her first year in office. Her plan would have increased the 26 cents per gallon tax by 45 cents over time to raise $2 billion annually. Polls found large-scale public opposition, and the plan did not pass the legislature.141

It is not clear why Michigan would need higher road funding. In 2015, lawmakers approved a huge tax-increase package to fund roads, and Michigan’s population has been static at 10 million people for two decades. A Reason Foundation study ranked Michigan in the bottom half of states in highway spending efficiency, so Whitmer should focus on using current highway funds more efficiently.142

Whitmer approved an increase in online sales taxes and she proposed increasing taxes on passthrough businesses. In a flip-flop that is angering retirees in the state, Whitmer campaigned in 2018 on repealing a pension tax imposed by the prior governor, but now she seems to have dropped the idea.143

Minnesota

Tim Walz, Democratic-Farmer-Labor

Legislature: Divided

Grade: D

Took office: January 2019

Tim Walz is a former member of the U.S. House and served in the Army National Guard. He was elected governor in 2018.

Walz entered office when Minnesota was projected to have large budget surpluses going forward. Rather than save the excess or give it back to taxpayers, Walz planned to spend it and then increase taxes to fund even more spending.145 But Walz had to compromise with the legislature and the final tax increase passed last year was about $330 million annually, mainly consisting of base broadening related to the federal TCJA.

Walz also pushed for higher gas taxes and vehicle fees to raise about $1 billion annually for transportation.146 Fortunately for Minnesota taxpayers, the final budget abandoned those increases.

With the recession in 2020 and lower projected revenues, surpluses have switched to deficits. Lawmakers are now looking at a deficit of $4.7 billion for the 2022–2023 biennium.147 Walz has had difficulty agreeing with the legislature on budget restraint and other important issues, such as police reforms in the wake of the George Floyd killing by a Minneapolis police officer in May 2020.148

Missouri

Mike Parson, Republican

Legislature: Republican

Grade: C

Took office: June 2018

Mike Parson is a veteran who served 6 years in the U.S. Army, followed by 22 years in law enforcement as a county sheriff. He served in the Missouri House and the Missouri Senate. He was the lieutenant governor, and was then sworn in as governor after his predecessor, Eric Greitens, resigned.

Soon after being sworn in, Parson signed into law a major tax reform. The reform, which was roughly revenue neutral overall, broadened the income tax base and reduced the top individual income tax rate from 5.9 percent to 5.4 percent.149 Before he resigned, Greitens had signed into law a bill reducing Missouri’s corporate tax rate from 6.25 percent to 4.0 percent.

Parson was less successful with another tax project in 2018. He argued in favor of a ballot initiative to increase the state gas tax by 10 cents per gallon. In November 2018, voters struck down the measure by a 54–46 margin.

General fund spending increased a robust 5.9 percent in 2020, but state leaders have shifted course to trim spending for 2021 because of the recession. Parson announced hundreds of millions of dollars in cuts to planned spending as revenue projections have fallen.150

Montana

Steve Bullock, Democrat

Legislature: Republican

Grade: C

Took office: January 2013

Steve Bullock is a long-time governor who received middling grades on previous Cato fiscal reports. He received a C in 2018, a C in 2016, and a D in 2014. In this report, Bullock scored above average on spending but below average on taxes.

In 2018, Bullock was a strong supporter of a ballot initiative (I‑185) to increase cigarette taxes from $1.70 per pack to $3.70 per pack.151 If it had passed, the increased revenue would have been used to fund the state’s Medicaid expansion. Montana voters shot down the tax increase by a 53–47 margin, but Medicaid expansion has gone ahead nonetheless.152

Nebraska

Pete Ricketts, Republican

Legislature: Nonpartisan

Grade: A

Took office: January 2015

Pete Ricketts is an entrepreneur and a former executive with TD Ameritrade. He is a consistent fiscal conservative and earns the third highest score on this report. Since taking office in 2015, Ricketts’ proposed budgets have been lean and general fund spending has risen at a modest 2.8 percent annual average rate.

Ricketts has pursued numerous tax cuts and tried to fend off tax increases, but he has been often stymied by the legislature. In 2015, Ricketts vetoed a gas tax hike, but the legislature overrode him to enact it. In 2017, Ricketts supported a tax overhaul that would have cut the top individual and corporate income tax rates. In his state of the state speech that year, the governor said, “If we want to outpace other Midwestern states, we have to be competitive on taxes.”153 Unfortunately, the legislature did not pass the plan.

In 2018, Ricketts proposed another plan to cut individual and corporate income tax rates, as well as limit local property taxes. The top individual tax rate would fall from 6.84 percent to 6.69 percent, while the corporate tax rate would fall from 7.81 percent to 6.69 percent. Again, the plan did not pass the legislature.

However, Ricketts did sign into law a major tax cut in 2018. The bill offset the tax-raising effects of the federal TCJA and provided Nebraskans with about $250 million in annual income tax relief.154

This year, Governor Ricketts approved a bill that exempts half of military retirees’ benefits from state taxes. Ricketts has also been pursuing property tax relief, and this year he signed into law a package of income and franchise tax credits to offset property taxes for homeowners and businesses. That provides a partial solution to the state’s problem of high property taxes, but the governor is right that the real long-term solution is local spending control.155

Nevada

Steve Sisolak, Democrat

Legislature: Democratic

Grade: B

Took office: January 2019

Steve Sisolak chaired the Clark County Commission before running for Nevada governor in 2018. He is the highest-scoring Democrat in this report based on his record of keeping spending flat and avoiding major tax increases.

However, Sisolak did extend a higher rate for Nevada’s modified business tax (MBT) in 2019, rather than allowing the rate to decline as scheduled. The MBT is complex, it creates uneven taxation across industries, and it is hidden from view of most voters since it is collected from businesses. It is a poor way for the state to raise revenues.

The MBT extension created a battle with Republicans in the legislature. Sisolak and the Democrats contended that the extension was not a tax increase and thus was not subject to Nevada’s constitutional requirement of a two-thirds supermajority vote.156 The Republicans argued that the tax extension was indeed unconstitutional.

In 2020, Sisolak supported a plan to make up for budget shortfalls by reducing the amount that mining companies can deduct from their taxes. The measure would raise about $55 million annually and hit businesses when they are already suffering from the downturn.

Finally, while Sisolak’s spending score was higher than average, he signed a law in 2019 imposing collective bargaining in state government, which had previously been prohibited. That action will likely boost state spending for employee compensation in coming years.

New Hampshire

Chris Sununu, Republican

Legislature: Democratic

Grade: A

Took office: January 2017

Chris Sununu is a former business owner and executive, as well as a former member of the New Hampshire Executive Council. With his record of spending restraint and tax cuts, Sununu receives the highest score on this report.

Throughout his tenure, Sununu has resisted pressure to increase taxes and spending, and he has defended New Hampshire’s status as a low-tax state with no individual income tax. A battle in recent years has been over a legislative plan to create a paid leave program funded by a new payroll tax. The payroll tax would be essentially an income tax, and its imposition would undermine New Hampshire’s unique tax-friendly status in the Northeast. Republican Governor Charlie Baker in neighboring Massachusetts signed into law a paid leave program funded by a payroll tax in 2018.

In a gubernatorial debate in 2018, Sununu explained his opposition to a mandatory paid leave program and payroll tax: “It was an effective income tax.… I can’t think of anything that would destroy the New Hampshire advantage more.”157 In 2019, Sununu vetoed a paid leave bill passed by the legislature that would have been funded by a 0.5 percent payroll tax. Sununu vetoed another version of the plan in 2020. Sununu supports reducing barriers for private provision of paid leave, but he is against a mandatory tax-funded program.158

While New Hampshire is free of an individual income tax, it does impose two major business taxes, the Business Profits Tax (BPT) and Business Enterprise Tax (BET). In 2017, Sununu signed legislation to cut the rates of both taxes. Over several years, the BPT rate was phased down from 8.2 percent to 7.7 percent and the BET phased down from 0.72 percent to 0.6 percent.

In 2019, the legislature passed a bill to halt the phased-in tax cuts. Sununu vetoed it, arguing that the move would “hurt our family-run small businesses, the lifeblood of our economy.”159

New Jersey

Phil Murphy, Democrat

Legislature: Democratic

Grade: F

Took office: January 2018

Phil Murphy worked at Goldman Sachs for more than 20 years and has been a major political donor.160 He has served as finance chair of the Democratic National Committee and as U.S. ambassador to Germany. Unlike his predecessor in the governor’s office, Chris Christie, who rejected tax hikes, Murphy has embraced them and receives one of the lowest scores on this report.

Murphy criticized the sales tax rate cut approved by Christie. He said that revenue losses from that cut prevented him from boosting funding for mass transit, college tuition, and other initiatives.161 His first budget pushed to raise the sales tax rate to bring in more than $500 million a year, but the legislature rejected the plan.

In 2018, Murphy signed into law a surtax on corporations with incomes above $1 million. The surtax is 2.5 percent for 2018 and 2019, and then it drops to 1.5 percent for 2020 and 2021. At the higher rate, the surtax drained more than $400 million a year out of New Jersey businesses. In September, Murphy and the legislature were making a deal to extend the corporate surtax.