Mr. Chairman, thank you for this opportunity to express my views on “Venezuela’s Tragic Meltdown.” A great deal of the commentary on the topic is polemical, and more-or-less political and ideological self-justifications of one sort or another. In consequence, the discourse is often confused and confusing. In an attempt to bring some clarity to the topic, I will focus on the one necessary condition that must be satisfied before the Venezuelan economy can be turned around. Inflation must be stopped before stability can be established. Stability might not be everything, but everything is nothing without stability.

ON THE MELTDOWN

Venezuela's economy, today, resembles that of the former Soviet Union before it collapsed. Venezuela has the largest proven oil reserves in the world, and not surprisingly produces one major product, oil. Oil production is carried out by a state-owned oil company, Petróleos de Venezuela, S.A. (PDVSA). PDVSA is so poorly run and its proven oil reserves are exploited so slowly as to render the value of its reserves worthless (Hanke, 2017). Venezuela's economy is also burdened by socialist-interventionist structure (Hanke and Yin, 2017). In consequence, economic life is heavily politicized and very uncertain.

Venezuela's economy is collapsing. This is the result of years of socialism, incompetence, and corruption, among other things. An important element that mirrors the economy's collapse is Venezuela's currency, the bolivar. It is not trustworthy. Venezuela's exchange rate regime provides no discipline. It only produces instability and poverty. Currently, Venezuela is experiencing one of the highest inflation rates in the world: 150% per year.

I observed much of Venezuela's economic dysfunction first-hand during the 1995-96 period, when I acted as President Rafael Caldera's adviser (Hanke, 2016). For an excellent analysis of the state of economic dysfunction in Venezuela during the pre-Chavez years, there is no better read than Moises Naim's book: Paper Tigers & Minotaurs: The Politics of Venezuela's Economic Reforms (Naim, 1993).

In 1999, Hugo Chavez was installed as president. It was then that the socialist seeds of Venezuela's meltdown started to be planted. As the seeds sprouted, Venezuela began to enter what has become a death spiral. For a most edifying read — one that gives a real feel for the bizarre state of economic affairs in Venezuela — I recommend Raul Gallegos' book: Crude Nation: How Oil Riches Ruined Venezuela (Gallegos, 2016).

To put Venezuela on a sound, sustained economic path will require massive economic reforms. Sound economies require sound institutions, even in oil-rich countries (Kaznacheev, 2017). Venezuela, like the former Soviet Union, has none. So, the task ahead will be great. But, as we learned in the communist countries of the former Soviet Union, inflation had to be snuffed out and economic stability established before successful economic reforms could be introduced.

ON VENEZUELA'S SYSTEMIC INFLATION

Venezuela suffered from an unstable currency and elevated inflation rates before the arrival of President Hugo Chavez, but with his ascendancy, fiscal and monetary discipline further deteriorated and inflation ratcheted up. By the time President Nicolas Maduro arrived in early 2013, inflation was in triple digits and rising.

With the acceleration of inflation, the Banco Central de Venezuela (BCV) became an unreliable source of inflation data. Indeed, from December 2014 until January 2016, the BCV did not report inflation statistics. To remedy this problem, the Johns Hopkins-Cato Institute Troubled Currencies Project, which I direct, began to measure inflation in 2013.

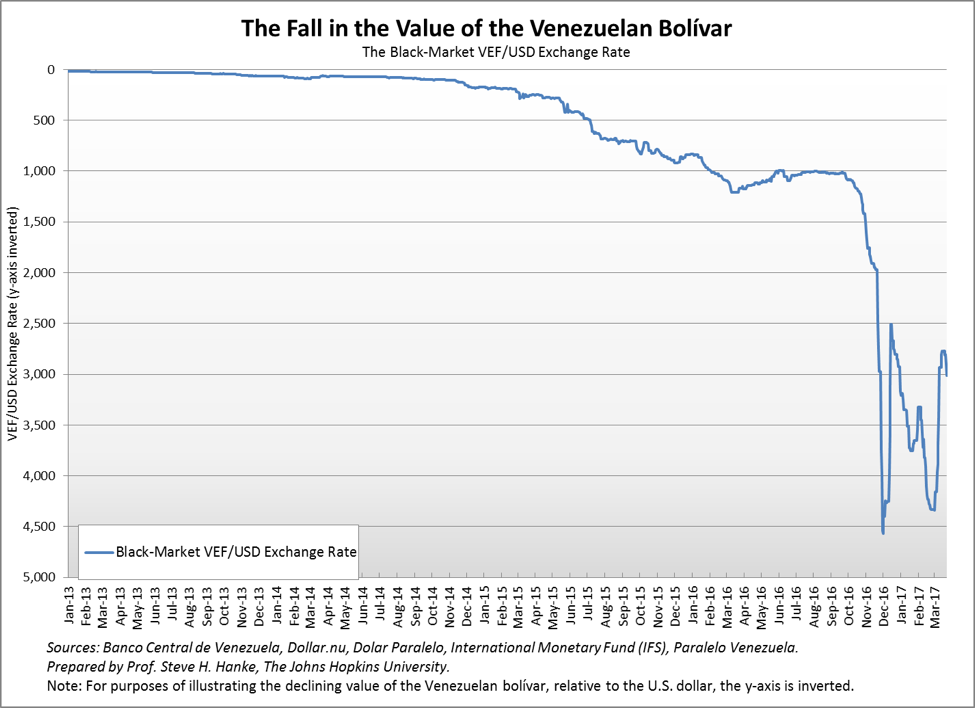

The most important price in an economy is the exchange rate between the local currency and the world's reserve currency — the U.S. dollar. As long as there is an active black market (read: free market) for currency and the black market data are available, changes in the black market exchange rate can be reliably transformed into accurate estimates of countrywide inflation rates. The economic principle of Purchasing Power Parity (PPP) allows for this transformation and the accurate estimates of countrywide inflation rates (Hanke and Bushnell, 2016).

Venezuela employs a multiple exchange-rate regime, coupled with exchange controls. In consequence, the official exchange rates are not free-market rates. To obtain the free-market exchange rates required for the application of PPP, we use black-market exchange rates. Black-market rates are efficient processors of information when political and economic circumstances make the official exchange rate unreliable or irrelevant. The course of the bolivar-U.S. dollar (VEF/USD) black-market rate is shown in the chart below. The value of the bolivar against the dollar has plunged, and with that, PPP suggests that Venezuela has experienced a dramatic inflation surge. And it has.

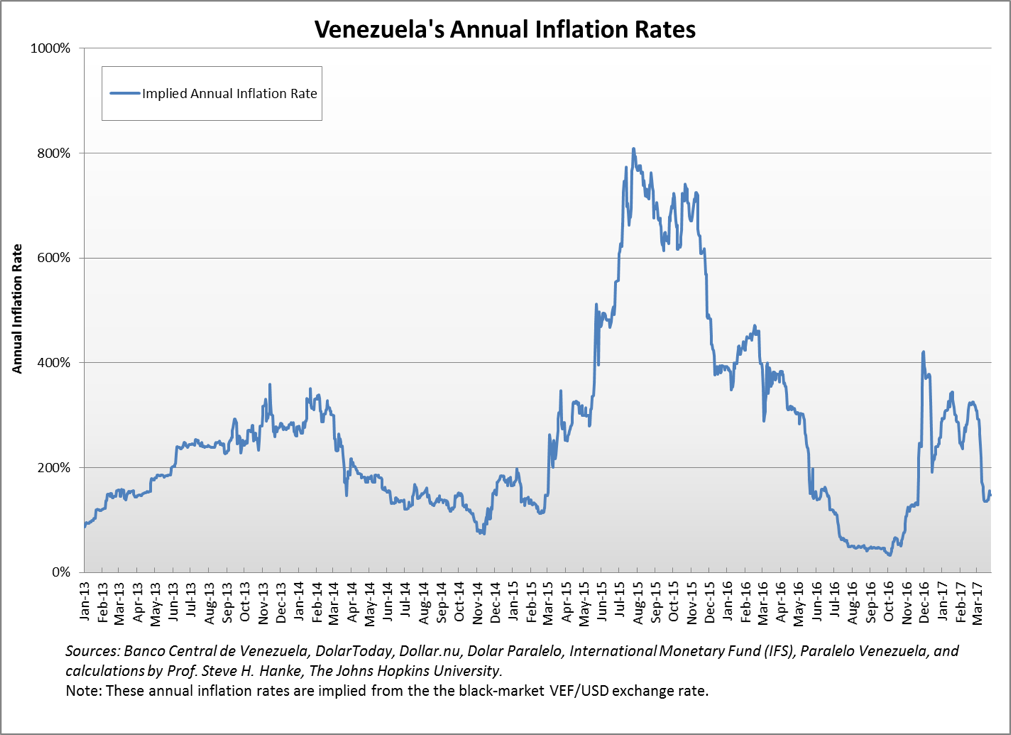

We compute the implied annual inflation rate on a daily basis by using PPP to translate changes in the VEF/USD exchange rate into an annual inflation rate (Hanke and Bushnell, 2016). The chart below shows the course of that annual rate, which peaked at 800% (yr/yr) in the summer of 2015.

It is worth mentioning that a bit later, in December 2016, Venezuela's inflation became the 57th official, verified episode of hyperinflation and was added to the Hanke-Krus World Hyperinflation Table, which is contained in the authoritative Routledge Handbook of Major Events in Economic History (2013).

An episode of hyperinflation occurs when the monthly inflation rate exceeds 50% for 30 consecutive days. Venezuela's monthly inflation rate exceeded 50% on November 3, 2016 and remained above 50% until December 14, 2016. The peak monthly inflation rate was 221%, which is relatively low in the context of hyperinflations (Hanke and Bushnell, 2016). Venezuela's hyperinflation episode is the 8th to occur in Latin America. Previous episodes in this region are: Argentina (1989), Bolivia (1984), Brazil (1989), Chile (1973), Nicaragua (1986), and Peru (1988 and 1990).

ON HOW TO STOP INFLATION AND ESTABLISH STABILITY

There are two proven ways to stop "high" inflations and establish stability. A country can install a currency board system in which its local currency becomes a clone of a reliable anchor currency. Alternatively, a country can abandon its local currency and adopt a reliable foreign currency (read: it can "dollarize"). I designed and implemented both currency board and "dollarized" systems in Latin America, the Baltics, and the Balkans (Hanke, 2016; Santos, 2015). I can attest to the fact that these currency reforms always work to stop inflation in its tracks and establish the stable conditions necessary to carry out economic reforms.

So just what is a currency board? An orthodox currency board issues notes and coins convertible on demand into a foreign anchor currency at a fixed rate of exchange. As reserves, it holds low-risk, interest-bearing bonds denominated in the anchor currency, and typically some gold. The reserve levels (both floors and ceilings) are set by law and are equal to 100%, or slightly more, of its monetary liabilities (notes, coins, and if permitted, deposits). A currency board's convertibility and foreign reserve cover requirements do not extend to deposits at commercial banks or to any other financial assets. A currency board generates profits from the difference between the interest it earns on its reserve assets and the expense of maintaining its liabilities (Hanke and Schuler, 2015).

By design, a currency board has no discretionary monetary powers and cannot engage in the fiduciary issue of money. It has an exchange rate policy (the exchange rate is fixed), but no monetary policy. A currency board's operations are passive and automatic. The sole function of a currency board is to exchange the domestic currency it issues for an anchor currency at a fixed rate. In consequence, the quantity of domestic currency in circulation is determined solely by market forces, namely the demand for domestic currency.

Several features of currency boards merit further elaboration. A currency board's balance sheet only contains foreign assets, which are set at a required level (or a tight range). If domestic assets are on the balance sheet, they are frozen. In consequence, a currency board cannot engage in the sterilization of foreign currency inflows or neutralization of outflows.

A second currency board feature that warrants attention is its inability to issue credit. A currency board cannot act as a lender of last resort or extend credit to the banking system. It also cannot make loans to the fiscal authorities and state-owned enterprises. In consequence, a currency board imposes a hard budget constraint and discipline on the economy.

A currency board requires no preconditions for monetary reform and can be installed rapidly. Government finances, state-owned enterprises, and trade need not be already reformed for a currency board to begin to issue currency.

Countries that have employed currency boards have delivered lower inflation rates, smaller fiscal deficits, lower debt levels relative to GDP, fewer banking crises, and higher real growth rates than comparable countries that have employed central banks.

No modern currency board has failed to maintain convertibility at their fixed exchange rate. Indeed, currency boards have an excellent record of maintaining their promised exchange rates, unlike central banks, and this includes Keynes' Russian currency board in Archangel. The so-called British ruble never deviated from its fixed exchange rate with the British pound. The board continued to redeem rubles for pounds in London until 1920, well after the civil war had concluded (Hanke and Schuler, 1991).

It is important to stress, particularly at these hearings, that the currency board idea became engulfed in controversy, thanks to Argentina. What Argentina termed "Convertibility" was introduced in April 1991 to stop inflation, which it did. The system had certain features of a currency board: a fixed exchange rate, full convertibility, and a minimum reserve cover for the peso of 100% of its anchor currency, the U.S. dollar. However, it had two major features which disqualified it from being an orthodox currency board. It had no ceiling on the amount of foreign assets held at the central bank relative to the central bank's monetary liabilities. So, the central bank could engage in sterilization and neutralization activities, which it did. In addition, it could hold and alter the level of domestic assets on its balance sheet. So, Argentina's monetary authority could engage in discretionary monetary policy, and it did so aggressively.

Because of these flaws, I penned an article which appeared in the Wall Street Journal shortly after the introduction of Convertibility. In that article, I concluded that, unless Argentina adopted orthodoxy and amended the Convertibility law, the system would eventually collapse (Hanke, 1991).

Since Argentina's Convertibility System allowed for both monetary and exchange rate policies, it was not a currency board (Hanke, 2008). Most economists fail to recognize this fact. Indeed, a scholarly survey of 100 leading economists who commented on the Convertibility System found that almost 97% incorrectly identified it as a currency board system (Schuler, 2005). In short, those that use the collapse of Argentina's Convertibility System to argue against currency boards are using a bogus argument. Indeed, they literally don't know what they are talking about.

The second proven alternative to stop "high" inflations and establish stability is "dollarization". It occurs when residents of a country use a foreign currency instead of the country's domestic currency. The term "dollarization" is used generically and covers all cases in which a foreign currency is used by local residents. Even though other foreign currencies, such as the euro and Swiss franc, are sometimes used instead of local currencies, it is the U.S. dollar that dominates. Hence, the use of the term "dollarization." At present, 33 countries are dollarized.

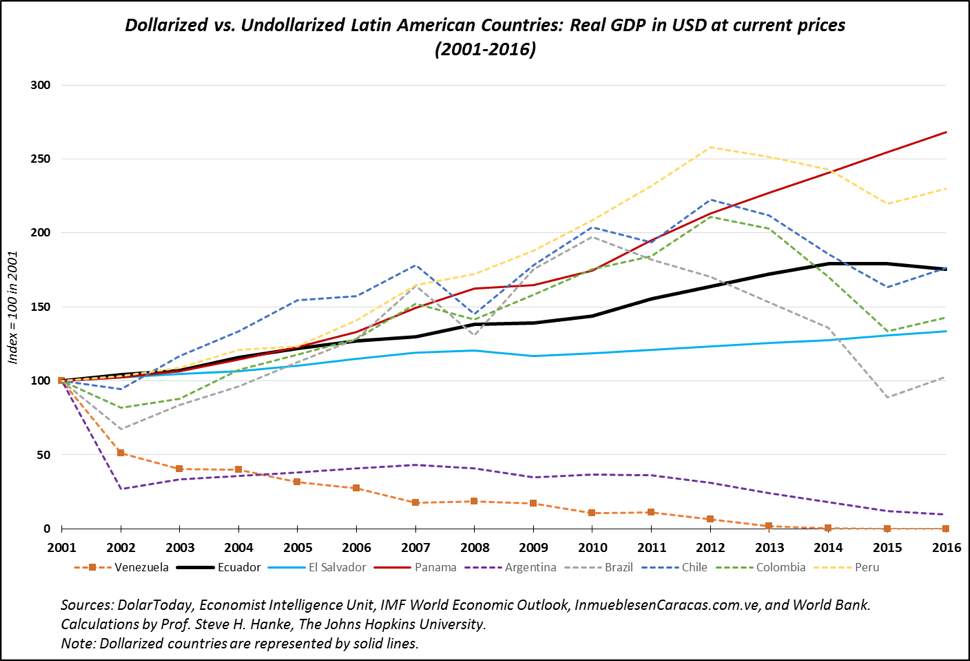

Countries that are officially dollarized produce lower, less variable inflation rates and higher, more stable economic growth rates than comparable countries with central banks that issue domestic currencies. Dollarization is, therefore, desirable. The accompanying chart shows the normalized values of real GDP in terms of U.S. dollars between 2001 (index value = 100) and 2016 for nine Latin American countries. Three — Panama, Ecuador, and El Salvador — are officially dollarized, while Peru is semiofficially dollarized. In the three officially dollarized countries, real GDP growth has been more stable and generally superior to growth in the countries that issue their own domestic currencies. While Peru's growth has only been surpassed by Panama's, it is less stable than growth in the three officially dollarized countries. The sharp changes in terms of trade, which were associated with the commodity cycle, affected the volatility of real GDP measured in U.S. dollar terms much more in the countries that issued their own domestic currencies than it did in those that were officially dollarized.

A U.S. POLICY RESPONSE TO VENEZUELA'S MELTDOWN?

The meltdown of Venezuela's economy is tragic and of Venezuela's own making. What to do? The U.S. government should avoid meddling directly in Venezuela's affairs. Forget the regime change mantra that has long been popular in certain circles within Washington, D.C. Proactive U.S. regime change policies have a long record of ending badly (Kinzer, 2013; Hanke, 2011; Hanke and Hanke, 2011).

So, should the U.S. adopt a "do nothing" policy towards Venezuela? No. The U.S. has international obligations. For example, the U.S. is a member of the Organisation of American States and the United Nations. These organizations, and others, provide an avenue for the U.S. to be engaged in the Venezuelan meltdown.

In addition, specific actions to address Venezuela's immediate inflation problem can be taken. These actions could encourage either the establishment of a currency board system or the adoption of dollarization. For example, in 1992, I worked with the leader of the U.S. Senate, Bob Dole, and Senators Steve Symms and Phil Gramm to draft U.S. legislation that would allow countries to use part of the U.S.'s quota contribution to the IMF for the establishment of currency boards. This legislation, (HR-5368, Law no. 102-391), was signed into law on October 6, 1992.

As for dollarization, it also has a U.S.-friendly history. For example, Senator Connie Mack worked tirelessly to promote dollarization and sound-money policies when he chaired the Joint Economic Committee of Congress (Schuler, 2000; Schuler and Stein, 2000).

It is gestures such as these that will provide the political opposition the courage to propose the only proven solutions to Venezuela's inflation problem — solutions that would immediately stop Venezuela's meltdown.

In closing, it is encouraging that a recent survey in Venezuela concluded that the public supports both currency boards (59% approve) and dollarization (62% approve). Even a large portion of those who support the current government don't support the central bank (50%) and want change, with 43% favoring a currency board and 31% favoring dollarization (DatinCorp, 2017).

REFERENCES

DatinCorp. "Venezuela: ¿Bolívar o Dólar?" Estudio de Coyuntura Económica. March 2017.

Gallegos, Raul. Crude Nation: How Oil Riches ruined Venezuela. Lincoln, Neb: Potomac Books, 2016.

Hanke, Steve H. "The Americas: Argentina Should Abolish Its Central Bank." Wall Street Journal [New York] 25 Oct. 1991, Eastern ed.: A15. WSJ.com. Wall Street Journal.

Hanke, Steve H. "Why Argentina did not have a currency board." Central Banking Journal, vol. 18, no. 3, 2008, pp. 56-58.

Hanke, Steve H. "On Democracy Versus Liberty." Globe Asia. February 2011.

Hanke, Steve H. "Remembrances of a Currency Reformer: Some Notes and Sketches from the Field" The Johns Hopkins Institute for Applied Economics, Global Health, and the Study of Business Enterprise, Studies in Applied Economics working paper no. 55. June 2016.

Hanke, Steve. "Venezuela's PDVSA: the World's Worst Oil Company." Forbes. Mar 6, 2017.

Hanke, Steve H, and Charles Bushnell. "Venezuela Enters the Record Book: The 57th Entry In The Hanke-Krus World Hyperinflation Table." The Johns Hopkins Institute for Applied Economics, Global Health, and the Study of Business Enterprise, Studies in Applied Economics working paper no. 69. December 2016.

Hanke, Steve H. and Liliane Hanke. "Démocratie versus liberté Les leçons tirées de la Constitution américaine " (Democracy versus Liberty: Lessons learned from the American Constitution). Commentaire, No. 135, 2011.

Hanke, Steve H., and Nicholas Krus. "World Hyperinflations." Routledge Handbook of Major Events in Economic History, Edited by Robert Whaples and Randall Parker. London, Routledge, 2013.

Hanke, Steve H., and Kurt Schuler. "Keynes's Russian Currency Board." in: Steve H. Hanke and Alan A. Walters, Capital Markets and Development. San Francisco: Institute for Contemporary Studies: 43-58. 1991.

Hanke, Steve H., and Kurt Schuler. Juntas Monetarias para países en desarrollo: Dinero, inflación y estabilidad económica. 2nd ed. Caracas: Cedice Libertad, 2015. The Johns Hopkins Institute for Applied Economics, Global Health, and the Study of Business Enterprise. International Center for Economic Growth, 2015.

Hanke, Steve H, and Jason Yin. "On Venezuela's Supply-Side Potential." The Johns Hopkins Institute for Applied Economics, Global Health, and the Study of Business Enterprise, Studies in Supply-Side Economics working paper no. 5. March 2017.

Kaznecheev, Peter. Curse or Blessing? How Institutions Determine Success in Resource-Rich Economies. Policy Analysis no. 808. Washington, D.C.: Cato Institute, 2017.

Kinzer, Stephen. The Brothers: John Foster Dulles, Allen Dulles, and their Secret World War. New York: Times Books Henry Holt and Company, 2013.

Naim, Moises. Paper Tigers and Minotaurs: the Politics of Venezuela's Economic Reforms. Washington, D.C: Carnegie Endowment for International Peace, 1993.

Santos, Tristana. "The Dollarizers." The Johns Hopkins Institute for Applied Economics, Global Health, and the Study of Business Enterprise, Studies in Applied Economics working paper no. 31. April 2015.

Schuler, Kurt. "Ignorance and Influence: U.S. Economists on Argentina's Depression of 1998-2002." Intellectual Tyranny of the Status Quo vol. 2, no.2, August 2005, Econ Journal Watch pp. 234-278.

Schuler, Kurt. "Basics of Dollarization." United States. Cong. Joint Economic Committee. 106th Cong., 2nd sess. Cong. Rept. Washington, D.C.: 349-94. 2000.

Schuler, Kurt and Robert Stein. "The Mack Dollarization Plan: An Analysis." Dollarization: A Common Currency for the Americas? March 6, 2000, Dallas, Federal Reserve Bank of Dallas.

About the Author