Some proponents of federal policies to combat climate change are arguing for a federal carbon tax (or similar type of “carbon price”). Within conservative and libertarian circles, some proponents claim that a revenue-neutral carbon tax “swap” could deliver a double dividend, reducing climate change while shifting some of the nation’s tax burden onto carbon emissions, which supposedly would spur the economy.

This analysis describes several serious problems with those claims. The actual economics of climate change — as summarized in the peer-reviewed literature as well as United Nations (UN) and Obama administration reports — reveal that the case for a U.S. carbon tax is weaker than the carbon tax proponents claim.

Future economic damages from carbon dioxide emissions can only be estimated in conjunction with forecasts of climate change. But recent history shows those forecasts are in flux, with an increasing number of forecasts of less warming appearing in the scientific literature in the last four years. Additionally, we show some rather stark evidence that the family of models used by the UN’s Intergovernmental Panel on Climate Change (IPCC) is experiencing a profound failure that greatly reduces their forecast utility.

If the case for emission cutbacks is weaker than the public has been led to believe, the claim of a double dividend is on even shakier ground. There really is a consensus in this literature, and it is that carbon taxes cause more economic damage than generic taxes do on labor or capital, so that in general even a revenue-neutral carbon tax swap would probably reduce economic growth.

When moving from academic theory to historical experience, we see that carbon taxes have not lived up to the promises of their supporters. In Australia, the carbon tax was quickly removed after the public recoiled against electricity price hikes and a faltering economy. Even in British Columbia (BC), Canada — touted as having the world’s finest example of a carbon tax — the experience has been underwhelming. After an initial (but temporary) drop, the BC carbon tax has not yielded significant reductions in gasoline purchases, and it has arguably reduced the BC economy’s performance relative to the rest of Canada.

Both in theory and in practice, economic analysis shows that the case for a U.S. carbon tax is weaker than its most vocal supporters have led the public to believe. At the same time, there is mounting evidence in the physical science of climate change to suggest that human emissions of carbon dioxide do not cause as much warming as is assumed in the current suite of official models. Policymakers and the general public must not confuse the confidence of carbon tax proponents with the actual strength of their case.

Introduction

Over the years, Americans have been subject to the growing drumbeat of a putatively urgent need for aggressive government action on climate change. After two failed attempts at a U.S. federal cap-and-trade program, those wishing to curb emissions have switched their focus to a carbon tax.

Although environmental regulation and taxes are traditionally associated with the political left, in recent years several vocal intellectuals and political officials on the right have begun pitching a carbon tax to libertarians and conservatives. They argue that climate science respects no ideology and that a carbon tax is a market solution far preferable to the top-down regulations that the left will otherwise implement. In particular, advocates of a carbon tax claim that if it is “revenue neutral”—that is, it does not increase the overall tax burden on the economy—then a “tax swap” deal involving reductions in corporate and personal income tax rates might both deliver stronger economic growth and reduce putative harm from climate change—a double dividend.

Although they often claim to be merely repeating the findings of consensus science on the need to combat climate change now, advocates of aggressive government intervention stand on very shaky ground. Using standard results from the economics of climate change—as codified in the peer-reviewed literature and published reports from the UN and the Obama administration—we can show that the case for a carbon tax is weaker than the public has been led to believe. Furthermore, the real-world experiences of carbon taxes in Australia and British Columbia, Canada, cast serious doubt on the promises of a market-friendly carbon tax in the United States.

The present study will summarize some of the key issues in the climate policy debate, showing that a U.S. carbon tax is a dubious proposal in both theory and practice.

The Social Cost of Carbon

The social cost of carbon (SCC) is a key concept in the economics of climate change and related policy discussions of a carbon tax. The SCC is defined as the present value of the net future external damages from an additional unit of carbon dioxide (CO2) emissions. In terms of economic theory, the SCC measures the negative externalities from emitting CO2 and other greenhouse gases (expressed in CO2-equivalents) and helps quantify the market failure where consumers and firms do not fully take into account the true costs of their carbon-intensive activities. As a first approximation, the optimal carbon tax would reflect the SCC. In practice, the Obama administration has issued estimates of the SCC that are being used in the cost-benefit evaluation of federal regulations (such as minimum energy efficiency standards) that aim to reduce emissions relative to the baseline.1

It is important to note that the SCC reflects the estimated damages of climate change in the entire world. This means that, if the SCC is used in federal cost-benefit analyses, the analyst is contrasting benefits accruing mostly to non-Americans with costs borne mostly by Americans. Whether the reader thinks such an arrangement is appropriate or not, it is clearly an important issue that has not been made clear in the U.S. debate on climate change policy. In any event, the federal Office of Management and Budget (OMB), in its Circular A‑4, clearly states that federal regulatory analyses should focus on domestic effects:

Your analysis should focus on benefits and costs that accrue to citizens and residents of the United States. Where you choose to evaluate a regulation that is likely to have effects beyond the borders of the United States, these effects should be reported separately.2

However, when the Obama administration’s Interagency Working Group (IWG) calculated the SCC, it ignored that clear OMB guideline and reported only a global value of the SCC. Thus, if a U.S. regulation (or carbon tax) is thought to reduce CO2 emissions, then the estimated benefits (calculated using the SCC) will vastly overstate the benefits to Americans.

As an affluent nation, the United States is economically much less vulnerable than other nations to the vagaries of weather and climate. Using two different approaches, the IWG in 2010 “determined that a range of values from 7 to 23 percent should be used to adjust the global SCC to calculate domestic effects. Reported domestic values should use this range.”3 Therefore, following OMB’s clear guideline on reporting the domestic effects of proposed regulations, the SCC value would need to be reduced anywhere from 77 to 93 percent to show the benefit to Americans from stipulated reductions in their CO2 emissions.

To repeat, those figures all derive from the Obama administration’s own IWG report. Whether or not Americans should consider any potential effects of their actions that accrue outside of the United States is outside the scope of this Policy Analysis, but it is important to recognize that the SCC does include such foreign benefits when used to assess the cost-benefit of federal actions, estimate the efficiency of carbon pricing mechanisms, or both.

SCC Calculations

In addition to such procedural problems with the use of the SCC in federal policy, there are deeper conceptual concerns. The average layperson may have the belief that the SCC is an empirical fact of nature that scientists in white lab coats measure with their equipment. However, in reality the SCC is a malleable concept that is entirely driven by analysts’ (largely arbitrary) initial assumptions. The estimated SCC can be quite large, small, or even negative—the latter meaning that greenhouse gas emissions should arguably be subsidized because they benefit humanity—depending on defensible adjustments of the inputs to the analysis.

But the possibility of such negative SCC values is rarely, if ever, reported. A recent study assessed the scientific literature on the SCC and determined that there exists a large and significant publication bias toward reporting only those results that indicated a positive SCC.4 The authors calculated that the selection bias resulted in a three- to four-times overestimate of the mean SCC value in the current mainstream economics literature. Such selective reporting of results can build upon itself to further enhance the biases in the literature, for example when future studies are developed from extant findings.

The most popular current approach used by U.S. policymakers to estimate the SCC involves the use of computer-based integrated assessment models (IAMs), which are complex simulations of the entire global economy and climate system over hundreds of years. Officially, the IAMs are supposed to rely on the latest results in the physical science of climate change, as well as on economic analyses of the effects of climate change on human welfare. Such effects are measured in monetary units but include a wide range of nonmarket categories (such as flooding and loss of ecosystem services). With particular assumptions about the path of emissions, the physical sensitivity of the climate system to atmospheric CO2 changes, and the effect on humans from changing climate conditions, the IAMs estimate the flow of incremental damages occurring centuries into the future as a result of an additional unit of CO2 emissions in some particular year. Then this flow of additional dollar damages (over the centuries) can be turned into an equivalent present value expressed in the dollars at the date of the emission, using a discount rate chosen by the analyst. The rate typically is not derived from observations of market rates of interest, but is instead picked (quite openly) by the analyst according to the analyst’s ethical views on how future generations should be treated.

In May 2013, the IWG produced an updated SCC value by incorporating revisions to the underlying three IAMs that the IWG used in its initial 2010 SCC determination.5 But at that time, the IWG did not update the equilibrium climate sensitivity (ECS) employed in the IAMs. The ECS is a critical concept in the physical science of climate change. Loosely speaking, it refers to the long-run (after taking into account certain feedbacks) warming in response to a doubling of CO2 concentrations. It is incredibly significant that the published estimates of the ECS have been trending downward, yet the IWG did not adjust this key input into the computer models. Specifically, the IWG made no adjustment in this parameter in its May 2013 update despite there having been, since January 1, 2011, at least 15 new studies and 24 experiments, involving 50 scientists, that examined the ECS, each lowering the best estimate and tightening the error distribution about that estimate.

Although it is not universally accepted that both the median estimate of the ECS and the risk of higher-than-anticipated warming are falling, such findings have come to dominate the contemporary scientific literature on the topic. The new, lower sensitivity findings are largely derived from improved estimates of the historical changes in climate forcings and temperatures over timespans ranging from centuries6 to millennia.7 In many cases, the new findings have supplanted earlier estimates that were based on poor assumptions and older parameter estimates.8 The few published findings in support of the status quo for sensitivity estimates have been met with methodological critique9 or exhibit a poor match to current evolution of global surface temperature patterns.10

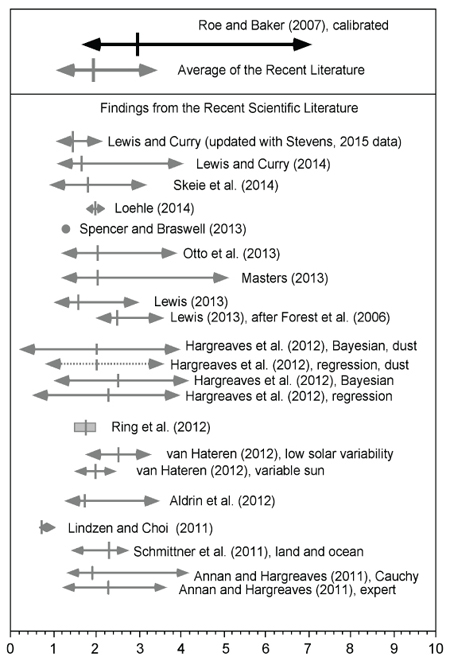

The dramatically lowered sensitivity estimates found in the recent literature are graphically shown in Figure 1. The range used by the IWG is clearly outdated; it was calibrated using findings through 2007,11 a calibration that no longer best describes the existing scientific literature.

Figure 1. Low Climate Sensitivity Estimates from the Recent Scientific Literature Compared with Roe and Baker Calibration Used by the Interagency Working Group

Note: The median (indicated by the small vertical line) and 90 percent confidence range (indicated by the horizontal line with arrowheads) of the climate sensitivity estimate used by the Interagency Working Group on the Social Cost of Carbon Climate (Roe and Baker 2007) is indicated by the top black arrowed line. The average of the similar values derived from 21 different determinations reported in the recent scientific literature is given by the gray arrowed line (second line from the top). The sensitivity estimates from the 21 individual determinations of the Equilibrium Climate Sensitivity (ECS) as derived from new research published after January 1, 2011, are indicated by the arrowed lines in the lower portion of the chart. The arrows indicate the 5 to 95 percent confidence bounds for each estimate along with the best estimate (median of each probability density function; or the mean of multiple estimates; short vertical line). M. J. Ring et al. present four estimates of the climate sensitivity and the box encompasses those estimates. See M. J. Ring et al., “Causes of the Global Warming Observed since the 19th Century,” Atmospheric and Climate Sciences2 (2012): 401–15, doi: 10.4236/acs.2012.24035. Spencer and Braswell produce a single ECS value best matched to ocean heat content observations and internal radiative forcing.

Roe and Baker 2007 = G. H. Roe and M. B. Baker, “Why is Climate Sensitivity So Unpredictable?,” Science 318 (2007): 629–32; Lewis and Curry 2014 = N. Lewis and J. A. Curry, “The Implications for Climate Sensitivity of AR5 Forcing and Heat Uptake Estimates,” Climate Dynamics 45 (2014): 1009–23; Stevens 2015 = B. Stevens, “Rethinking the Lower Bound on Aerosol Radiative Forcing,” Journal of Climate 28 (2015): 4794–819; Skeie et al. 2014 = R. B. Skeie et al., “A Lower and More Constrained Estimate of Climate Sensitivity Using Updated Observations and Detailed Radiative Forcing Time Series,” Earth System Dynamics 5 (2014): 139–75; Loehle 2014 = C. Loehle, “A Minimal Model for Estimating Climate Sensitivity,” Ecological Modelling 276 (2014): 80–84; Spencer and Braswell 2013 = R. W. Spencer and W. D. Braswell, “The Role of ENSO in Global Ocean Temperature Changes during 1955–2011 Simulated with a 1D Climate Model,” Asia-Pacific Journal of Atmospheric Science 50 (2013): 229–37; Otto et al. 2013 = A. Otto et al., “Energy Budget Constraints on Climate Response,” Nature Geoscience 6 (2013): 415–16; Masters 2013 = T. Masters, “Observational Estimates of Climate Sensitivity from Changes in the Rate of Ocean Heat Uptake and Comparison to CMIP5 Models,” Climate Dynamics 42 (2013): 2173–81; Lewis 2013 = N. Lewis, “An Objective Bayesian Improved Approach for Applying Optimal Fingerprint Techniques to Estimate Climate Sensitivity,” Journal of Climate 26 (2013): 7414–29; Forest et al. 2006 = C. E. Forest et al., “Estimated PDFs of Climate System Properties Including Natural and Anthropogenic Forcings,” Geophysical Research Letters 33 (2006): L01705; Hargreaves et al. 2012 = J. C. Hargreaves et al., “Can the Last Glacial Maximum Constrain Climate Sensitivity?” Geophysical Research Letters 39 (2012): 24702; Ring et al. 2012 = M. J. Ring et al., “Causes of the Global Warming Observed since the 19th Century,” Atmospheric and Climate Sciences 2 (2012): 401–15; van Hateren 2012 = J. H. van Hateren, “A Fractal Climate Response Function Can Simulate Global Average Temperature Trends of the Modern Era and the Past Millennium,” Climate Dynamic 40 (2012): 2651–70; Aldrin et al. 2012 = M. Aldrin et al., “Bayesian Estimation of Climate Sensitivity Based on a Simple Climate Model Fitted to Observations of Hemispheric Temperature and Global Ocean Heat Content,” Environmetrics 23 (2012): 253–71; Lindzen and Choi 2011 = R. S. Lindzen and Y‑S. Choi, “On the Observational Determination of Climate Sensitivity and Its Implications,” Asia-Pacific Journal of Atmospheric Science 47 (2011): 377–90; Schmittner et al. 2011 = A. Schmittner et al., “Climate Sensitivity Estimated from Temperature Reconstructions of the Last Glacial Maximum,” Science 334 (2011): 1385–88; Annan and Hargreaves 2011 = J. D. Annan and J.C Hargreaves, “On the Generation and Interpretation of Probabilistic Estimates of Climate Sensitivity,” Climatic Change 104 (2011): 324–436.

The abundance of literature supporting a lower climate sensitivity was at least partially reflected in the latest (2013) IPCC assessment:

Equilibrium climate sensitivity is likely in the range 1.5°C to 4.5°C (high confidence), extremely unlikely less than 1°C (high confidence), and very unlikely greater than 6°C (medium confidence). The lower temperature limit of the assessed likely range is thus less than the 2°C in the [Fourth Assessment Report].12

Given the consensus of recent literature, we believe that the IWG’s assessment of the low end of the probability density function is indefensible and the IWG’s estimate of the shape of the high end of the ECS distribution is increasingly questionable.13

The findings of Otto and others,14 which were available at the time of the IWG’s 2013 revision, are particularly noteworthy in that 15 of the paper’s 17 authors were also lead authors of the 2013 IPCC report. The authors estimate a mean sensitivity of 2.0°C and a 5–95 percent confidence interval of 1.1 to 3.9°C. If the IPCC truly defined the consensus, that consensus is different from what the IWG claims. Instead of a 95th percentile value of 7.14°C, as used by the IWG, a survey of the recent scientific literature suggests a value of 3.5°C—more than 50 percent lower. That is a very important difference because the high end of the ECS distribution has a large effect on the SCC determination—a fact frequently noted by the IWG.

Chapters 17–19 of Michaels and Knappenberger give an extensive discussion of the lower sensitivity research, including some new and paradigm-shifting research by Bjorn Stevens and Nic Lewis.15

Discount Rates

The problem with the SCC as a tool in policy analysis goes beyond quibbles over the proper parameter values. At least the ECS is an objectively defined (in principle) feature of nature. In contrast, other parameters are needed to calculate the SCC that by their very essence are subjective, such as the analyst’s view on the proper weight to be given to the welfare of future generations. Needless to say, that approach to “measuring” the SCC is hardly the way physicists estimate the mass of the moon or the charge on an electron. To quote Massachusetts Institute of Technology economist Robert Pindyck (who favors a U.S. carbon tax) in a scathing Journal of Economic Literature article:

And here we see a major problem with IAM-based climate policy analysis: The modeler has a great deal of freedom in choosing functional forms, parameter values, and other inputs, and different choices can give wildly different estimates of the SCC and the optimal amount of abatement. You might think that some input choices are more reasonable or defensible than others, but no, “reasonable” is very much in the eye of the modeler. Thus these models can be used to obtain almost any result one desires. [Emphasis added]16

To see just how significant some of the apparently innocuous assumptions can be, consider the latest IWG estimates of the SCC. For an additional ton of emissions in the year 2015, using a 3 percent discount rate, the SCC is $36. However, if we use a 2.5 percent discount rate, the SCC rises to $56 per ton, whereas a 5 percent discount rate yields an SCC of only $11 per ton.17 Note that that huge swing relies on the same underlying models of climate change and economic growth; the only change is in adjustments of the discount rate, and the values used are quite plausible. Indeed, the IWG came under harsh criticism because it ignored explicit OMB guidance to include a 7 percent discount rate in all federal cost-benefit analyses, presumably because the SCC at such a discount rate would be close to $0 per ton or even negative.18

The reason the IWG estimates of the SCC are so heavily dependent on the discount rate is that the three underlying computer models all show relatively modest damages from climate change in the early decades. Indeed, one model (Richard Tol’s FUND model) actually exhibits net benefitsfrom global warming through about 3°C of warming relative to preindustrial temperatures.19 The higher the discount rate, the more weight is placed on earlier time periods (when global warming is not as destructive or is even beneficial) and the less important are the large damages that will not occur in the computer simulations for centuries. Economists do not agree on the appropriate discount rate to use in such settings because the usual arguments in favor of market-based measures (which would yield a very low SCC) are not as compelling when current policy decisions do not bind future policymakers.20 Such are the difficulties in making public policy on the basis of threats that might not fully manifest themselves for another two generations.

If the economic models were updated to more accurately reflect the latest developments from the physical and biological sciences, the estimated SCC would likewise decline between one-third and two-thirds21 because lower temperature increases would translate into reduced climate change damages. That is a sizeable and significant reduction.

Model Design and Inputs

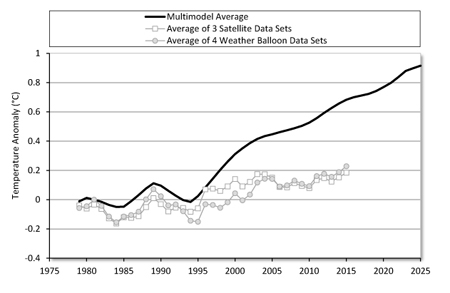

Then there are problems with the climate models themselves. Clearly, a large and growing discrepancy exists between their predictions and what is being observed, as shown in Figure 2.

Figure 2. A Comparison of Observed and Modeled Temperatures in the Lower Atmosphere

Source: Adapted from John Christy’s February 2, 2016, testimony to the U.S. House Committee on Science, Space, and Technology.

Note: Centered five-year running means of 102 individual model projections (black) used in the 2013 IPCC report for the middle troposphere versus both weather balloon (gray circles) and satellite observations (open squares). The linear trend (based on 1979–2014) of all times series intersects zero at 1979. Note that the five-year running means are shown for periods containing at least three nonmissing values.

Our illustration, developed from recent U.S. House of Representatives testimony by John Christy of the University of Alabama, Huntsville,22 dramatically shows the climate modeling problem in a nutshell. It shows model-predicted and observed temperatures in the middle troposphere rather than at the surface, with maximum sampling at about 13,000 feet. Those are less compromised by Earth’s complicated surface and humanity’s role in altering it. More important, though, is that the vertical profile of temperature is what determines atmospheric stability. When the lapse rate—the difference between the lowest layers and higher levels—is large, the atmosphere is unstable. Instability is the principal source for global precipitation. Although models can be (and are) tuned to mimic changes in surface temperatures, the same can’t be done as easily for the vertical profile of temperature changes.

As the figure indicates, the air in the middle troposphere is warming far more slowly than has been predicted, even more slowly than the torpid surface is warming. Consequently, the difference between the surface and the middle troposphere has become slightly greater, a condition which should produce a very slight increase in average precipitation. On the other hand, the models forecast that the difference between the surface and the middle troposphere should become less, a condition which would add pressure to decrease global precipitation.

The models are therefore making systematic errors in their precipitation projections. That has a dramatic effect on the resultant climate change projections. When the surface is wet, which is what occurs after rain, the sun’s energy is directed toward the evaporation of that moisture rather than to directly heating the surface. In other words, much of what is called “sensible weather” (the kind of weather a person can sense) is determined by the vertical distribution of temperature. If the popular climate models get that wrong (which is what is happening), then all the subsidiary weather may also be incorrectly specified.

Therefore, problems and arbitrariness arise not just from the economic assumptions but also from the physical models that are used as inputs to the SCC calculations. The situation is even worse than described by Pindyck.

Although the modeled sensitivities are dropping, there are still indications that the models themselves are too hot. None of the current batch of official SCC calculations accounts for this.

Shifting Emissions

Another problem with use of the SCC as a guide to setting carbon taxes is the problem of “leakage”—carbon emitting activities in a regulated jurisdiction relocating to a less-regulated jurisdiction. Strictly speaking, it would make sense (even in textbook theory) to calibrate only a worldwide and uniformly enforced carbon tax to the SCC. If a carbon tax were applied only to certain jurisdictions, then emission cutbacks in the affected region would be partially offset by increased emissions (relative to the baseline) in the nonregulated regions. Depending on the specifics, that leakage could greatly increase the economic costs of achieving a desired climate goal. Thus the optimal carbon tax is lower if applied unilaterally in limited jurisdictions.

To get a sense of the magnitude of the problems of leakage, consider the results from William Nordhaus, a pioneer in the economics of climate change, creator of the DICE model (one of the three used by the IWG), and an advocate for a carbon tax.23 After studying his 2007 model runs, Nordhaus reported that, with regard to a globally enforced carbon tax, achieving a given environmental objective (such as a temperature ceiling or atmospheric concentration) with only 50 percent of planetary emissions covered would involve an economic abatement cost penalty of 250 percent. Even if the top 15 countries (by emissions) participated in the carbon tax program, covering three-quarters of the globe’s emissions, compliance costs for a given objective would still be 70 percent higher than for the full-coverage baseline case, according to Nordhaus’s estimates.24

To see the tremendous problem of limited participation from a different perspective, one can use the same model that the U.S. Environmental Protection Agency (EPA) uses to calculate the effect of various policy proposals. The Model for the Assessment of Greenhouse Gas Induced Climate Change (MAGICC) is available in an easy-to-use form on the Cato Institute website.25 This model shows that, even if the United States linearly reduced its emissions to zero by the year 2050, the average global temperature in the year 2100 would be just 0.1°C—that’s one-tenth of a degree—lower than would otherwise be the case. Note that that calculation does not even take into account leakage, that is, the fact that complete cessation of U.S. emissions could induce other nations to increase their economic activities and hence emissions. Our point in using those results from the MAGICC modeling is not to christen them as confident projections but rather to show that, even on their own terms and using an EPA-endorsed model, American policymakers have much less control over global climate change than they often imply.

UN Reports Can’t Justify Popular Climate Goal

Advocates of government intervention to mitigate climate change have broadly settled on a minimum goal of limiting global warming (relative to preindustrial times) to 2°C, with many pushing for much more stringent objectives (such as limiting atmospheric greenhouse gas concentrations to 350 ppm [parts per million] of CO2, or the temperature rise to 1.5°C). The question is, why that goal and not 0˚C or 4˚C?

The reason is not because the IPCC, the most commonly recognized authority on climate change, specifically endorses 2˚C. According to IPCC’s 2013 report (often referred to as AR5 for Fifth Assessment Report), limiting global warming to 2°C would likely require stabilizing atmospheric concentrations between 430 and 480 ppm by the year 2100.26 The report estimates that this would require a reduction in consumption of 4.8 percent (relative to the baseline projection).27 Those are the costs of achieving the popular 2°C goal.

To determine the benefits of the 2°C goal, we would need to know the reduction in climate change damages that would result under a business-as-usual scenario versus the mitigation scenario (with the 2°C temperature ceiling). Even under the most pessimistic emissions scenario with no government controls (report scenario RCP8.5), by 2100 the AR5’s central estimate of global warming is about 4.5°C.28 A more realistic business-as-usual scenario (between RCP6 and RCP8.5) would involve warming by 2100 of less than 4°C. Therefore, the gross benefits of the stipulated mitigation policy are the climate change damages from 4°C warming minus the climate change damages from 2°C warming.

Unfortunately, the AR5 report does not allow us to compute such figures because just about all of the comprehensive analyses of the effects of global warming consider ranges of 2.5–3°C. The AR5 does contain a table29 summarizing some of the estimates in the literature, out of which the most promising (for our task) are two results from Roson and van der Mensbrugghe.30 They estimate that 2.3°C warming would reduce global economic output by 1.8 percent, whereas 4.9°C warming would reduce output by 4.6 percent. (Note that that particular estimate was the only one in the AR5 table that estimated the effect of warming higher than 3.2°C.)

Therefore, using ballpark figures, we could conclude that limiting climate change to 2°C rather than an unrestricted 4°C would mean that the Earth in the year 2100 would be spared about (4.6 – 1.8 =) 2.8 percent of output loss in climate change damages. In contrast, the report claims that the economic compliance costs of the mitigation goal would be 4.8 percent of consumption in the year 2100. In other words, we would spend 4.8 percent of economic output to avoid a 2.8 percent output loss.

So, if we take the IPCC’s numbers at face value and assume away the practical problems that would prevent mitigation policies from reaching the theoretical ideal, the popular climate goal of limiting global warming to 2°C would most likely entail greater economic damages than it would deliver in benefits (in the form of reduced climate change damages). The pursuit of more aggressive goals and the use of imperfectly designed policy tools to achieve them would, of course, only make the mismatch between costs and benefits even worse.

“Fat Tails” and Carbon Taxes as Insurance?

As a postscript to those observations, we note that the leaders in the pro–carbon tax camp are abandoning traditional cost-benefit analysis, claiming its use is inappropriate in the context of climate change. One reason given for this is concern over “fat tails”—concern that climate change could result in damages far greater than what is currently considered likely. Worries about fat tails lead some carbon tax proponents, like Harvard economist Martin Weitzman, to argue that, instead of treating a carbon tax as a policy response to a given (and known) negative externality, it should be considered a form of insurance pertaining to a catastrophe that might happen but with unknown likelihood.31

But that argument poses some serious problems. The most obvious is that the utility of such “insurance” is declining, given the emerging evidence that very large warming is unlikely. Beyond that, the whole purpose of the periodic IPCC reports was to produce a compilation of the consensus research to guide policymakers. But Weitzman and others argue that policymakers should be concerned about what we don’t know.32 That argument certainly has some merit, but, as economist David R. Henderson points out, broad-based uncertainty cuts both ways in the climate change policy debate. For example, it is possible that the Earth is headed into a period of prolonged cooling, in which case offsetting anthropogenic warming would be beneficial—meaning that a carbon tax would be undesirable.33 So why should one unlikely but troubling scenario shape our policy thinking but another unlikely but troubling scenario be ignored?

Another problem with Weitzman’s approach—as Nordhaus, among other critics, has pointed out34—is that it could be used to justify aggressive and costly policies against several low-probability catastrophic risks, including asteroid strikes, rogue artificial intelligence developments, and bioweapons. After all, we can’t rule out humanity’s destruction from a genetically engineered virus in the year 2100, and what’s worse we are not even sure how to construct the probability distribution on such events. Yet few people would argue that we should forfeit 5 percent of global output to reduce the likelihood of one of the latter improbable catastrophes. Why then do some people make that argument about climate change?

That question leads to another problem with the insurance analogy. With actual insurance, the risks are well known and quantifiable, and competition among insurers provides rates that are reasonable for the damages involved. Furthermore, for all practical purposes, buying insurance eliminates the (financial) risk. Yet, to be analogous to the type of insurance that Weitzman and others are advocating, a homeowner would be told that a roving gang of arsonists might, decades from now, set his home on fire, that a fire policy would cost 5 percent of income every year until then, and that, even if the house were struck by the arsonists, the company would indemnify the owner for only some of the damages. Who would buy such an insurance policy?

Carbon Tax Reform “Win-Wins”? The Elusive “Double Dividend”

Some proponents of a carbon tax have tried to decouple it entirely from the climate change debate. They argue that, if the receipts from a carbon tax were devoted to reductions in taxes on labor or capital, then the economic cost of the carbon tax would be reduced and might even be negative. In other words, they claim that, by “taxing bads, not goods,” the United States might experience a double dividend in which we tackle climate change and boost conventional economic growth.

Such claims of a double dividend are emphasized in appeals to libertarians and conservatives to embrace a carbon tax-swap deal. For example, in a 2008 New York Times op-ed calling for a revenue-neutral carbon tax swap, Arthur Laffer and Bob Inglis wrote, “Conservatives do not have to agree that humans are causing climate change to recognize a sensible energy solution.”35 For another example, in his 2015 study titled “The Conservative Case for a Carbon Tax,” Niskanen Center president Jerry Taylor writes, “Even if conservative narratives about climate change science and public policy are to some extent correct, conservatives should say ‘yes’ to a revenue-neutral carbon tax.”36

As a practical matter, it is tempting to dismiss the idea of revenue-neutral, “pro-growth” carbon tax reform as a red herring because it is very unlikely that any national politically feasible deal would respect revenue neutrality. Revenue neutrality has certainly not happened at other levels of government. California governor Jerry Brown, for example, wanted to use revenue from California’s cap-and-trade program to subsidize a high-speed rail network.37 The Regional Greenhouse Gas Initiative—which is the cap-and-trade program for power plants in participating Northeast and Mid-Atlantic states—uses its revenue to subsidize renewables, energy efficiency projects, and other green investments.38 In Washington State, Governor Jay Inslee wants to install a new state-level cap-and-trade levy on carbon emissions to fund a $12.2 billion transportation plan.39

Even Taylor, in his paper, advocates a non–revenue-neutral carbon tax that would impose a net tax hike of at least $695 billion in its first 20 years.40 It is possible that this support was a mere oversight (i.e., that in his study Taylor genuinely believed he was pushing a revenue-neutral plan but failed to appreciate its details), but he did later write on the Niskanen Center blog: “But what if a tax-for-regulation swap were to come up in an attempt to address budget deficits and the looming fiscal imbalance? . . . But even were those fears realized, conservatives should take heart: using carbon tax revenues to reduce the deficit makes good economic sense.”41

With progressives enumerating the various green investments that could be funded by a carbon tax, and, with even one of the leaders in the conservative pro–carbon tax camp laying the intellectual foundation for a net tax hike, it should be clear that a revenue-neutral deal at the federal level is very unlikely.

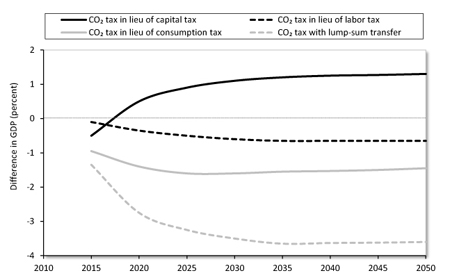

Putting aside that practical concern, there are economic reasons to be skeptical of the idea. For example, a 2013 Resources for the Future (RFF) study42 considered the different effects on gross domestic product (GDP) of various methods of implementing a revenue-neutral carbon tax at varying levels. Figure 3 reproduces their findings for the case of a $30 per ton tax on CO2 (in 2012 dollars), which would be completely revenue neutral, with the funds being returned to citizens through one of four ways: (1) reductions in the corporate income tax rate and personal income tax rate on dividends, interest, and capital gains (solid black line); (2) reductions in the payroll tax rate and personal income tax rate on labor income (dotted black line); (3) reductions in state sales tax rates (solid gray line); or (4) a lump-sum payment made to each adult citizen (dotted gray line). The carbon tax is imposed in 2015 and revenue neutrality is maintained throughout the scenario. In only one of these scenarios (and only after a few years) does the economic dividend result.

Figure 3. Difference in GDP Relative to Baseline from Revenue-Neutral $30 per Ton Carbon Dioxide (CO2) Tax

Source: Adapted from Jared C. Carbone et al., “Deficit Reduction and Carbon Taxes: Budgetary, Economic, and Distributional Impacts,” Resources for the Future, August 2013, Figure 1.

Note: GDP = gross domestic product.

The results of the RFF modeling may surprise readers who are familiar with the pro-growth claims about a carbon tax swap deal. Further, to the extent that a U.S. carbon tax would not be fully revenue neutral, the reality would be much worse than is depicted in the theoretically ideal Figure 3. It should be stressed that RFF is a respected organization in this arena, and it’s fair to say that most of its scholars would endorse a (suitably designed) U.S. carbon tax.

RFF’s modeling results are quite consistent with the academic literature. In a 2013 review article in Energy Economics, Stanford economist Lawrence Goulder—one of the pioneers in the field of environmental tax analysis—surveyed the literature and concluded:

If, prior to introducing the environmental tax, capital is highly overtaxed (in efficiency terms) relative to labor, and if the revenue-neutral green tax reform shifts the burden of the overall tax system from capital to labor (a phenomenon that can be enhanced by using the green tax revenues exclusively to reduce capital income taxes), then the reform can improve (in efficiency terms) the relative taxation of these factors. If this beneficial impact is strong enough, it can overcome the inherent efficiency handicap that (narrow) environmental taxes have relative to income taxes as a source of revenue. . . .

The presence or absence of the double dividend thus depends on the nature of the prior tax system and on how environmental tax revenues are recycled. Empirical conditions are important. This does not mean that the double dividend is as likely to occur as not, however. The narrow base of green taxes constitutes an inherent efficiency handicap. . . . Although results vary, the bulk of existing research tends to indicate that even when revenues are recycled in ways conducive to a double dividend, the beneficial efficiency impact is not large enough to overcome the inherent handicap, and the double dividend does not arise. [Emphasis added]43

In short, Goulder is saying that the bulk of research finds that even a theoretically ideal revenue-neutral carbon tax would probably not promote conventional economic growth (in addition to curbing emissions). The only way such a result is even theoretically possible is if the original tax code is particularly distorted in a certain dimension (such as taxing capital much more than labor) and if the carbon tax revenues are then devoted to reducing that distortion.

It is important for libertarian and conservative readers concerned about the economic effects of a new carbon tax to understand what Goulder means when he explains that the “narrow base of green taxes constitutes an inherent efficiency handicap.”44 If we put aside for the moment concern about climate change, then generally speaking it would be foolish (on standard tax efficiency grounds) to raise revenue by taxing CO2 emissions rather than taxing labor or capital more broadly. The tax on CO2 would have a much narrower base, meaning that it would take a higher rate of taxation to yield a given dollar amount of revenue. Because standard analyses suggest that the economic harms of taxes (the deadweight losses) are proportional to the square of the tax rate, those considerations mean that even a dollar-for-dollar tax swap would nonetheless increase the economic drag of the overall tax code.45

The technical phenomenon in the literature driving such results is the tax interaction effect, in which a new green tax (such as a carbon tax) interacts with the preexisting, distortionary taxes on labor and capital and makes them more damaging. Note that the carbon tax raises consumer prices and effectively reduces the after-tax earnings of labor and capital, acting as its own (implicit) tax on labor and capital, but with the difference that it is concentrated in particular areas rather than spread uniformly over all labor and capital. This distortion is the intuition behind the results found in the literature: as a general rule, even a dollar-for-dollar carbon tax swap deal will hurt the conventional economy.

Thus we see that the typical pro-growth case for the carbon tax gets things exactly backward: generally speaking, to the extent that the U.S. tax code is already filled with distortions, the case for implementing a carbon tax of a particular magnitude is actually weaker, not stronger, even if we assume full revenue-recycling by reduction of those preexisting, distortionary taxes.

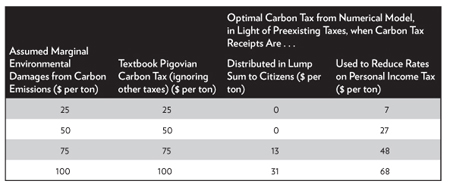

To illustrate those nuances, as well as to convey the magnitude of their importance, Table 1 shows the estimates from a numerical simulation of the economic effects of various carbon taxes. This table comes from a pioneering 1996 paper in the American Economic Review by Bovenberg and Goulder.46

Table 1. Textbook Carbon Tax versus Optimal Carbon Tax, with Presence of Prior U.S. Federal Tax Code Distortions

Source: Adapted from 1994 simulation in A. Lans Bovenberg and Lawrence H. Goulder, “Optimal Environmental Taxation in the Presence of Other Taxes: General Equilibrium Analyses,” American Economic Review 86 (1996): 985‑1000. Table 1 is adapted from Table 2 (in the appendix) from the 1994 NBER Working Paper No. 4897 version of the article, http://www.nber.org/papers/w4897. Note that our table uses their “realistic benchmark” personal income tax rate reduction and lump-sum scenarios.

Much of the contemporary U.S. policy debate on climate change restricts its attention to the first two columns in Table 1. Many analysts assume that, if the SCC is, say, $25 per ton, then the federal government should at least put a price on carbon (such as a carbon tax) at a level of $25 per ton, to reflect the negative externality. Then, to the extent that consideration is given to preexisting taxes, which are themselves distortionary, most analysts—particularly those urging libertarian or conservative readers to embrace a carbon tax—think it is self-evident that full revenue recycling can only enhance the case for a carbon tax, indeed perhaps making it sensible even if one neglects the environmental externality. Yet the third and fourth columns in Table 1 show that such common reasoning is backward,47 at least in typical models in this literature. Generally speaking, the presence of distortionary taxes reduces the case for a new carbon tax, meaning that (considering all economic and environmental aspects) the optimal carbon tax will end up being lower than the SCC.48

The effect of the tax interaction effect on policy design can be enormous. For example, as Table 1 indicates, in the case of a $50 SCC, if the carbon tax receipts are to be returned in lump-sum fashion, then the optimal carbon tax—with all feedback effects on the tax system taken into account—is zero. The outcome reflects the fact that introducing even a very modest carbon tax (such as a mere $1 per ton) would exacerbate the deadweight losses of the preexisting taxes so much that the marginal economic costs swamp the stipulated $50 per ton environmental benefits of the carbon tax, meaning that it would be better—all things considered—not to levy even the modest carbon tax in the first place. The policy wonks advocating a carbon tax almost never consider that type of possibility in their discussions with libertarians and conservatives.

It is true that, given a carbon tax, it is better to use the receipts to reduce tax rates rather than spend the money or return it in a lump sum to citizens. That is why Table 1 shows that, in the case of a $50 social cost of carbon, the optimal carbon tax with personal income tax rate reduction is $27. Thus, putting the U.S. policy debate in terms of Table 1, the analysts advocating a carbon tax have been focusing on the fact that $27 is more than $0 (i.e., it’s better to use carbon tax receipts to fund tax rate reductions than for other uses). But they generally overlook the fact that $27 is less than $50, meaning that carbon taxes make sense only if there are high environmental damages from emissions, and even in that case—and even with a fully revenue-neutral tax rate swap—we would still implement only a carbon tax much lower than the assumed SCC.

Are Carbon Taxes a Market Solution?

Advocates often refer to a carbon tax (and cap-and-trade programs) as a market solution to the problem of human-caused climate change. This is in contrast to the command-and-control mandates that have been used traditionally to limit various emissions. The virtues of market forces are a central plank in Taylor’s argument for a carbon tax.49

According to textbook theory, it is more efficient for society to achieve a desired emissions reduction by putting a price on carbon and letting individuals in the market determine the specific emissions cutbacks, rather than by having political officials mandate fuel economy standards, power plant rules, building insulation standards, and so on.

But that idea poses several problems. In the first place, even on its own terms, a carbon tax is hardly a genuine market solution analogous to other introductions of property rights. The classic tragedy of the commons conception of a negative externality involved animals overgrazing on English pastureland and the establishment of private property in real estate (enforced at low cost via barbed wire fencing).50 But if policymakers, instead of awarding property rights, had adopted a policy solution akin to a carbon tax, they would have fined only some ranchers and shepherds a certain number of guineas for every acre-year of grazing by their animals and adjusted that fine periodically for reasons that were often little more than whim. Meanwhile, other ranchers would not be assessed any penalty at all, even as their animals degraded the commons. Would that really be a market solution to the original tragedy of the commons?

Another problem with the idea of a carbon tax as a market solution is that left-leaning, progressive environmentalists would be, on their own terms, foolish to go along with such a bargain. Taylor, in an interview with Vox writer David Roberts, estimates that the true SCC (including fat-tail risk) ranges “anywhere from, say, $70 to $80 a ton to a couple hundred dollars a ton.”51 Taylor further agrees with Roberts that any politically feasible U.S. carbon tax will be “almost certainly well south” of $70 per ton.52 Why then would any progressive give up direct regulatory tools if a U.S. carbon tax—especially in the beginning, when much of the world continues to emit without constraint—will be nowhere near the level needed to achieve the stipulated emissions cutbacks for a 2°C goal, let alone a more aggressive goal such as 350 ppm? In the interview, Taylor answers that even a modest carbon tax will achieve more emissions cutbacks than particular regulatory interventions. But how would that satisfy someone worried about catastrophic risks to future generations? It would simply underscore the need to pursue further command-and-control regulations in conjunction with the (inadequate) carbon tax.

Progressives want to use a carbon tax only to augment direct mandates, as they have made clear in public statements. In one of several examples, the group Clean Energy Canada in early 2015 published a pamphlet, “How to Adopt a Winning Carbon Price: Top Ten Takeaways from Interviews with the Architects of British Columbia’s Carbon Tax.” Here is takeaway #8: “A carbon tax can’t do everything; it needs to be just one component of a full suite of climate policies.”53 (A post on the U.S. progressive website Grist.com favorably covered the release of the pamphlet. The author of the post—the same David Roberts—commented, “I certainly hope [carbon] tax advocates take heed of No. 8!”54) We discuss British Columbia’s much-celebrated carbon tax later in this study, but for now we note that the proposal to replace top-down regulations with a carbon tax is a fantasy. Progressives aren’t even agreeing to that in principle. How, then, can we expect them to go along with such a deal in practice?

Finally, to link the discussion in the preceding section with this one, we note that a 2010 RFF analysis by Parry and Williams concluded that the tax interaction effect could be so powerful as to dominate the textbook advantages of a market-based approach. In their words:

The increase in energy prices caused by market-based climate policies causes higher production costs throughout the economy, which in turn leads to a slight contraction in the overall level of economic activity, employment, and investment. As a result, distortions in labor and capital markets due to preexisting taxes are increased, producing an economic cost. This cost is larger for market-based instruments because they tend to have a much greater impact on energy prices than emissions standards, for envisioned CO2 reductions over the medium term. [Emphasis added]55

To be sure, the RFF analysis still favored a carbon tax with full revenue recycling through other tax rate reductions as the best policy. But, if forced to choose between a direct kilowatt-hour emissions mandate on the power sector versus a politically realistic cap-and-trade program containing substantial amounts of free allowances to ease the burdens on certain special interests, the RFF study actually rejected the cap-and-trade market solution as having economic costs 200 percent higher than the command-and-control mandates. Such an outcome doesn’t occur in a simplistic textbook analysis that disregards the existing tax code, but in the real world all market solutions—whether cap-and-trade or a carbon tax—raise energy prices and thus render preexisting taxes much more destructive.

Case Studies: Carbon Taxes in Action

As of November 2014, at least 39 distinct programs were in place around the world to price some portion of CO2 emissions, whether using a carbon tax, a cap-and-trade program, or a hybrid of the two. Those policies have been implemented over a period spanning three decades, ranging from Finland’s carbon price, which became effective as of 1990, to new policies in Chile that will take effect in 2017. Effective carbon prices range from $1 per ton up to $168 per ton (the last being in Sweden, which does offer major exemptions and rebates for certain businesses).56 In the interest of brevity, this study will explore the history of two prominent examples of real-world carbon taxes, in Australia and British Columbia.

Australia

On July 1, 2012, the Australian government instituted a carbon tax of $23 (Australian dollars) per ton of CO2-equivalent, and raised it to $24.15 per ton a year later. The tax proved so unpopular that, in the September 2013 elections, the Liberal Party/National Party coalition took control of the government from the Labor Party in a campaign that Liberal leader (and new prime minister) Tony Abbott explicitly billed as a referendum on the carbon tax. The carbon-pricing scheme was formally ended in July 2014.57

Alex Robson, an economics professor from Griffith University in Brisbane, Australia, who has published peer-reviewed papers on the interaction of fiscal and environmental policies,58 authored a 2013 study critical of the Australian carbon tax.59 Robson’s study shows that the introduction of the Australian carbon tax went hand in hand with a spike in household electricity prices (the “highest quarterly increase on record”) and unemployment, and that many Australian business owners anecdotally reported that the carbon tax was a key factor in their decision to lay off workers or shut down entirely. 60

Beyond those drawbacks—which help to explain the Liberal/National victory in 2013—Robson’s study reveals that none of the pillars in the market case for a U.S. carbon tax swap proved reliable in Australia. For example, contrary to the notion that a carbon tax could be used to provide pro-growth tax reform, in Australia the carbon tax was accompanied by so many giveaways (to mitigate negative effects on various special interests) that the Australian government had to raise effective marginal income tax rates on 2.2 million taxpayers. (Income taxes were reduced for 560,000 taxpayers.)

In the same vein, rather than reducing distortionary environmental policies, the Australian carbon tax was not accompanied by any reform of the government’s inefficient wind and solar subsidies, or Renewable Energy Target mandates. On the contrary, Australia’s carbon tax was instituted along with the creation of a Clean Energy Finance Corporation.

Finally, instead of establishing a predictable price for carbon that firms could incorporate into their long-term investment plans, the Australian carbon policy proved to be almost comically unstable. Originally the government promised during the 2010 campaign that it would not implement a carbon tax in the next three-year cycle, but then the carbon tax was introduced in July 2012, with a planned transition to a cap-and-trade scheme in 2015. Later, the government proposed to move to the cap-and-trade scheme in 2014, but this step was never formalized, leaving the business community uncertain. And, of course, with the September 2013 election of Abbott, the policy was upended again, with the abolition of Australia’s carbon tax in July 2014. The real-world case of Australia shows that achieving a carbon tax does not provide policy certainty to allow businesses to make long-term decisions with confidence.

British Columbia

The Canadian province of British Columbia (BC) established a carbon tax of 10 Canadian dollars (C$) per ton of carbon in 2008, which was ramped up gradually until maxing out at C$30 per ton (roughly equal to $24 per ton in U.S. dollars using current exchange rates) in July 2012.61 This works out to about 6.7 Canadian cents per liter62 of gasoline (about 21 U.S. cents per gallon). The tax is quite broad, with the BC government claiming that its “carbon tax applies to virtually all emissions from burning fuels, which accounts for an estimated 70 per cent of total emissions in British Columbia.”63 Of special interest to the U.S. policy debate among conservatives and libertarians is that the BC carbon tax was explicitly designed to be revenue neutral, with the government periodically reporting on how the carbon tax receipts have been returned to BC residents via other tax cuts.64

Many proponents of a U.S. carbon tax point to the BC example as a model that (they claim) shows that a properly designed carbon tax can significantly reduce emissions while leaving the economy unscathed. For instance, economists Yoram Bauman65 and Shi-Ling Hsu 66 wrote in a 2012 New York Times op-ed:

On Sunday, the best climate policy in the world got even better: British Columbia’s carbon tax—a tax on the carbon content of all fossil fuels burned in the province—increased from $25 to $30 per metric ton of carbon dioxide, making it more expensive to pollute. . . .

A carbon tax makes sense whether you are a Republican or a Democrat, a climate change skeptic or a believer, a conservative or a conservationist (or both). We can move past the partisan fireworks over global warming by turning British Columbia’s carbon tax into a made-in-America solution. [Emphasis added.]67

Other examples could be cited of proponents claiming that British Columbia is one of the prime exhibits that shows that a revenue-neutral carbon tax can reduce emissions without impairing economic growth.68 Yet we challenge that claim.

One popular 2012 econometric analysis of the BC episode concluded that its carbon tax reduced emissions from gasoline about five times as much as would be expected from comparable, market-induced increases in gasoline prices.69 The authors hypothesize that the reduced emissions resulted because BC residents are willing to cut back on driving in an effort to mitigate climate change as long as their fellow BC residents can’t free-ride off their sacrifices. The problem with that notion is that it would indicate very poor reasoning on the part of BC residents: the rest of the world, which is not subject to BC’s carbon tax, can still free-ride off any BC cutbacks.

A much more plausible explanation for the econometric results is that BC residents are (at least partially) buying gasoline in other jurisdictions. Note that a market-induced rise in pump prices in British Columbia would not lead to that effect because, presumably, gas prices in neighboring Alberta or Washington State would also be affected by a change in world supply and demand. However, when BC residents see their gas prices rise because of the BC carbon tax, then (other things being equal) we would expect gasoline in other jurisdictions to become relatively more attractive.

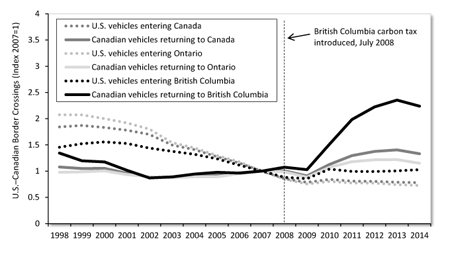

Although pro–carbon tax writers have tried to downplay the significance of that possibility, the data do indicate a sharp increase in cross-border traffic between British Columbia and Washington State after the BC carbon tax was implemented. Figure 4 shows various trends in cross-border vehicle traffic expressed as an index relative to year 2007 levels.

Figure 4. Select U.S.–Canadian Vehicle Border Crossings, Annual, 1998–2014

Source: Data are from Statistics Canada, Table 427‑0002, “Number of Vehicles Travelling between Canada and the United States,” http://www5.statcan.gc.ca/cansim/a26?lang=eng&id=4270002.

As Figure 4 indicates, a pronounced increase in Canadian vehicle crossings of the BC–Washington State border occurred after the carbon tax was introduced in July 2008. The surge cannot be due to, say, changes in the Canadian–U.S. dollar exchange rate because we don’t see nearly the same rise in Canadian vehicles returning to either Canada as a whole or Ontario in particular. Vehicles returning to British Columbia were up 136 percent in 2013 relative to 2007 levels, whereas in Ontario they were up only 22 percent. The actual number of returning BC vehicles was 3.2 million in 2007 and 7.6 million in 2013, compared with a total BC population of about 4.6 million in 2013.70 Furthermore, the surge can’t be due to changes in border flexibility, as some have suggested, because we don’t see nearly as much of a relative surge in U.S. traffic at the BC border relative to other checkpoints.

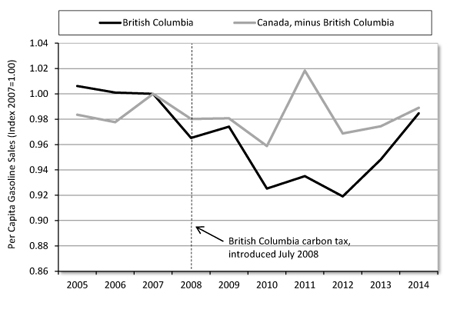

Another significant point is that, even if not a statistical artifact, the apparently large reduction in BC emissions proved to be temporary. The studies trumpeting the potency of BC’s carbon tax went only through 2012 data. However, officially reported BC gasoline sales increased sharply in 2013 and 2014, such that as of 2014 annual per capita BC gasoline sales were down only 2 percent compared with 2007, only a percentage point lower than the rest of Canada.71 See Figure 5. On this criterion it seems British Columbia’s carbon tax had a very weak long-term effect on gasoline consumption, even if we ignore the significant leakage problem.

Figure 5. Per capita Official Gasoline Sales in British Columbia vs. Rest of Canada, Annual, 2005–14

Source: Data are from Statistics Canada, Table 134‑0004, “Supply and Disposition of Refined Petroleum Products,” http://www5.statcan.gc.ca/cansim/a26?lang=eng&id=1340004.

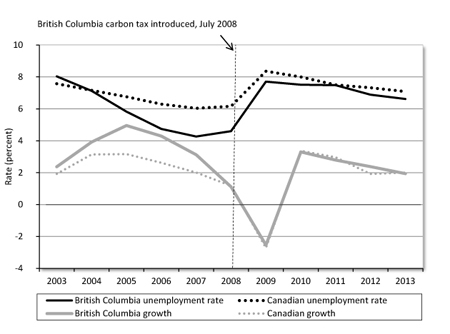

The claim that British Columbia’s carbon tax did not harm the conventional economy—because BC growth has matched overall Canadian growth since 2008—ignores the fact that the BC economy was outperforming the rest of Canada before the carbon tax. Specifically, from 2003 to 2008, BC real output grew by a cumulative 18.6 percent, whereas Canadian real GDP grew by only 12.7 percent. In contrast, from 2008 to 2013 (the latest annual figure available), BC output grew by 8.0 percent, whereas Canadian output grew by 7.7 percent.72

We see a similar pattern in the labor market. In the five years before introduction of the BC carbon tax, the average unemployment rate in British Columbia was 5.6 percent, compared with a Canadian average of 6.6 percent. But, in the five years after the BC carbon tax began, the average unemployment rate in British Columbia was 7.1 percent compared to 7.6 percent in Canada overall.73 Thus the labor market advantage of British Columbia versus Canada was cut in half if we look at the five-year periods before and after introduction of the BC carbon tax. See Figure 6.74

Figure 6. Unemployment and Real Growth Rates, Annual Averages, British Columbia vs. Canada, 2003–13

Source: Unemployment data are from Statistics Canada, Table 282–008, “Labour Force Survey Estimates (LFS), by North American Industry Classification System (NAICS), Sex and Age Group,” http://www5.statcan.gc.ca/cansim/a26?lang=eng&id=2820008; economic data are from Statistics Canada, Table 384‑0038, “Gross Domestic Product, Expenditure-based, Provincial and Territorial,” http://www5.statcan.gc.ca/cansim/a26?lang=eng&id=3840038.

As a final twist, we note that BC authorities report that they actually (and apparently unintentionally) provided net tax cuts in conjunction with the revenue-neutral carbon tax, presumably because they did not anticipate the sharp fall in gasoline sales in the region.75 In other words, they gave too-generous tax cuts because they assumed the carbon tax receipts would be higher than those ultimately realized. The BC tax cuts took the form of rate reductions and lump-sum payments (the latter directed to low-income groups that would be especially harmed by rising energy prices). Proponents note that the BC carbon tax swap has yielded the lowest personal income tax rates in Canada, but that describes the average effective rates. What really matters is the marginal tax rate, which indicates how much a taxpayer is assessed for an additional unit of labor or income. In 2014 British Columbia had six income tax brackets, ranging up to 16.8 percent, whereas neighboring Alberta had a flat income tax of 10 percent.76 The notion that British Columbia is now an economic powerhouse because of its carbon tax and offsetting adjustments to the tax code is far from reality.

In summary, when we look at British Columbia—the hands-down best real-world example of a carbon tax swap, according to proponents—we find that even the official figures show that British Columbia has had only a modest reduction in gasoline consumption relative to the rest of Canada, and those official figures appear to show significant leakage into other jurisdictions. That may have led authorities to provide larger tax cuts than they had intended. Furthermore, British Columbia’s offsetting tax cuts were not designed solely to encourage labor and economic growth because they included lump-sum transfers to low-income groups. Indeed, in practice the evidence suggests that, even with the associated net tax cuts, BC unemployment and real economic growth rates suffered after the carbon tax was enacted. Inasmuch as any U.S. carbon tax will not be revenue neutral—let alone be phased in with net tax cuts—the BC example leads us to expect modest changes in gas consumption in exchange for a weaker economy.

Conclusion

Many Americans believe that the U.S. government must adopt aggressive policies to slow greenhouse gas emissions. A handful of vocal intellectuals and political officials are now encouraging libertarians and conservatives to consider a win-win tax-swap deal that ostensibly would give them desired reductions in other taxes and regulations in exchange for conceding to a carbon tax.

This study has shown just how dubious that popular narrative is. Indeed, many proponents of a carbon tax are denying a growing body of low-sensitivity findings as well as a large and growing discrepancy between climate model predictions and temperature observations in the lower atmosphere. Furthermore, relying on standard results in the economics of climate change literature, we have shown serious problems in the estimation of the SCC. We have also shown that, even if we knew the SCC, other considerations would imply a significantly lower optimal carbon tax.

Of particular relevance to libertarians and conservatives, we have further shown that the tax interaction effect suggests no double-dividend boost to conventional economic growth, even if a carbon tax were fully refunded through payroll tax cuts or lump-sum payments. In the more realistic scenario in which a carbon tax would be only partially refunded, the results aren’t even close: such a tax would clearly hurt the conventional economy, meaning that it could be justified only on environmental grounds.

Finally, critical analysis of the real-world carbon tax experiences in Australia and British Columbia show that the promises of a market-friendly U.S. carbon tax were violated in both scenarios. Even in the case of British Columbia—hailed by carbon tax advocates as the best example to date of such a policy—after an initial drop the tax has not yielded significant reductions in gasoline purchases, whereas it has apparently reduced the BC economy’s performance relative to Canada.

Libertarians and conservatives in particular should not simply trust the assurances from the advocates of a carbon tax but should instead read the relevant literature themselves. In both theory and practice, a U.S. carbon tax remains a very dubious policy proposal.

NOTES

The authors gratefully acknowledge David R. Henderson and Jeffrey Miron for comments on an early draft, and Jim Manzi and Philip Cross for providing references.

1. The original social cost of carbon estimates from the Obama administration were published in Interagency Working Group on Social Cost of Carbon, “Technical Support Document: Social Cost of Carbon for Regulatory Impact Analysis—Under Executive Order 12866,” February 2010, http://www.epa.gov/oms/climate/regulations/scc-tsd.pdf. A major update to the estimates was issued in May 2013, “Technical Support Document: Technical Update of the Social Cost of Carbon for Regulatory Impact Analysis Under Executive Order 12866,” https://www.whitehouse.gov/sites/default/files/omb/inforeg/social_cost_of_carbon_for_ria_2013_update.pdf. As of this writing, the latest estimates were released on July 2015: “Technical Support Document: Technical Update of the Social Cost of Carbon for Regulatory Impact Analysis under Executive Order 12866,” https://www.whitehouse.gov/sites/default/files/omb/inforeg/scc-tsd-final-july-2015.pdf.

2. See the Office of Management and Budget Circular A‑4 (September 17, 2003) regarding regulatory analysis.

3. Interagency Working Group on Social Cost of Carbon, “Technical Support Document: Social Cost of Carbon for Regulatory Impact Analysis—Under Executive Order 12866,” p. 11.

4. T. Havranek et al., “Selective Reporting and the Social Cost of Carbon,” Energy Economics (2015), doi:10.1016/j.eneco.2015.08.009.

5. Interagency Working Group, “Technical Support Document,” May 2013 revision, https://www.whitehouse.gov/sites/default/files/omb/inforeg/social_cost_of_carbon_for_ria_2013_update.pdf.

6. For example, N. Lewis and J. A. Curry, “The Implications for Climate Sensitivity of AR5 Forcing and Heat Uptake Estimates,” Climate Dynamics 45 (2014): 1009–23, doi:10.1007/s00382-014‑2342‑y. See also A. Otto et al., “Energy Budget Constraints on Climate Response,” Nature Geoscience 6 (2013): 415–16.

7. For example, A. Schmittner et al., “Climate Sensitivity Estimated from Temperature Reconstructions of the Last Glacial Maximum,” Science 334 (2011): 1385–88, doi:10.1126/science.1203513; J. C. Hargreaves et al., “Can the Last Glacial Maximum Constrain Climate Sensitivity?” Geophysical Research Letters 39 (2012): 24702, doi:10.1029/2012GL053872.

8. J. D. Annan and J. C. Hargreaves, “On the Generation and Interpretation of Probabilistic Estimates of Climate Sensitivity,” Climatic Change 104 (2011): 324–436.

9. For example, N. Lewis, “Does ‘Inhomogeneous Forcing and Transient Climate Sensitivity’ by Drew Shindell Make Sense?” Climate Audit, March 10, 2014, http://climateaudit.org/2014/03/10/does-inhomogeneous-forcing-and-transient-climate-sensitivity-by-drew-shindell-make-sense/; T. Masters, “On Forcing Enhancement, Efficacy, and Kummer and Dessler,” Troy’s Scratchpad, May 9, 2014, https://troyca.wordpress.com/2014/05/09/on-forcing-enhancement-efficacy-and-kummer-and-dessler-2014/; N. Lewis, “Marotzke and Forster’s Circular Attribution of CMIP5 Intermodel Warming Differences,” Climate Audit, February 5, 2015, https://climateaudit.org/2015/02/05/marotzke-and-forsters-circular-attribution-of-cmip5-intermodel-warming-differences/.

10. P. J. Michaels and P. C. Knappenberger, “‘Worse than We Thought’ Rears Its Ugly Head Again,” Cato at Liberty, January 6, 2013, http://www.cato.org/blog/worse-we-thought-rears-ugly-head-again.

11. G. H. Roe and M. B. Baker, “Why is Climate Sensitivity So Unpredictable?” Science 318 (2007): 629–32.

12. “Summary for Policymakers,” Climate Change 2013: The Physical Science Basis. Contribution of Working Group I to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change, eds. T. F. Stocker et al. (Cambridge, UK, and New York: Cambridge University Press, 2013), p. 16, http://www.ipcc.ch/pdf/assessment-report/ar5/wg1/WG1AR5_SPM_FINAL.pdf.

13. N. Lewis and M. Crok, “A Sensitive Matter: How the IPCC Buried Evidence Showing Good News about Global Warming,” Global Warming Policy Foundation, 2014, http://www.thegwpf.org/content/uploads/2014/02/A-Sensitive-Matter-Foreword-inc.pdf.

14. A. Otto et al., “Energy Budget Constraints on Climate Response.”

15. P. J. Michaels and P. C. Knappenberger, Lukewarming: The New Climate Science That Changes Everything (Washington: Cato Institute, 2015); B. Stevens, “Rethinking the Lower Bound on Aerosol Radiative Forcing,” Journal of Climate 28 (2015): 4794–4819; N. Lewis, “Implications of Lower Aerosol Forcing for Climate Sensitivity,” Climate Etc., March 19, 2015, https://judithcurry.com/2015/03/19/implications-of-lower-aerosol-forcing-for-climate-sensitivity/.

16. Robert Pindyck, “Climate Change Policy: What Do the Models Tell Us?” Journal of Economic Literature 51 (2013): 5, http://web.mit.edu/rpindyck/www/Papers/Climate-Change-Policy-What-Do-the-Models-Tell-Us.pdf.

17. Interagency Working Group, “Technical Support Document,” July 2015 revision, https://www.whitehouse.gov/sites/default/files/omb/inforeg/scc-tsd-final-july-2015.pdf.

18. For a comprehensive discussion of the SCC and discount rates, see the Institute for Energy Research’s “Comment on the Technical Support Document,” submitted to the Office of Management and Budget in February 2014, http://instituteforenergyresearch.org/wp-content/uploads/2014/02/IER-Comment-on-SCC.pdf.

19. For example, Interagency Working Group, “Technical Support Document: Social Cost of Carbon for Regulatory Impact Analysis under Executive Order 12866,” February 2010, Figure 1A, https://www3.epa.gov/otaq/climate/regulations/scc-tsd.pdf.

20. Some standard references showcasing various perspectives in the discounting literature are Robert C. Lind, ed., Discounting for Time and Risk in Energy Policy (Washington: Resources for the Future, 1982); and Paul R. Portney and John P. Weyant, eds., Discounting and Intergenerational Equity (New York: Resources for the Future, 1999).

21. S. Waldhoff et al., “The Marginal Damage Costs of Different Greenhouse Gases: An Application of FUND,” Economics: The Open-Access E‑Journal, no. 2014–31 (2014), http://www.economics-ejournal.org/economics/journalarticles/2014–31.

22. John Christy, University of Alabama, Huntsville, Testimony before the Committee on Science, Space, and Technology, U.S. House of Representatives, February 2, 2016.

23. It is true that, in the text to this point, we have seriously questioned the accuracy of IAMs such as Nordhaus’s DICE model. However, we are merely illustrating the quantitative significance of “leakage” in terms of the standard models themselves, to show that even on its own merits, the case for a U.S. carbon tax is weaker than the public has been led to believe.

24. William Nordhaus, A Question of Balance: Weighing the Options on Global Warming Policies (New Haven, CT: Yale University Press, 2008), p. 19.

25. The calculator is available at http://www.cato.org/blog/current-wisdom-we-calculate-you-decide-handy-dandy-carbon-tax-temperature-savings-calculator. The estimate relies on a 3°C climate sensitivity assumption.

26. See O. Edenhofer et al., “Technical Summary,” in Climate Change 2014: Mitigation of Climate Change. Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change, ed. O. Edenhofer et al. (Cambridge, UK, and New York: Cambridge University Press, 2014), p. 25, http://www.ipcc.ch/pdf/assessment-report/ar5/wg3/ipcc_wg3_ar5_technical-summary.pdf.

27. See Intergovernmental Panel on Climate Change, “2014: Summary for Policymakers,” in Climate Change 2014: Mitigation of Climate Change. Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change, eds. O. Edenhofer et al. (Cambridge, UK, and New York: Cambridge University Press, 2014), Table SPM.2, p. 15, http://www.ipcc.ch/pdf/assessment-report/ar5/wg3/ipcc_wg3_ar5_summary-for-policymakers.pdf.

28. See Figure 12–40, M. Collins et al., “Long-term Climate Change: Projections, Commitments and Irreversibility,” Climate Change 2013: The Physical Science Basis. Contribution of Working Group I to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change, eds. T. F. Stocker et al. (Cambridge, UK: Cambridge University Press, 2013), p. 1100, http://www.ipcc.ch/pdf/assessment-report/ar5/wg1/WG1AR5_Chapter12_FINAL.pdf.

29. See D. J. Arent et al., “Key Economic Sectors and Services, Supplementary Material,” in Climate Change 2014: Impacts, Adaptation, and Vulnerability. Part A: Global and Sectoral Aspects. Contribution of Working Group II to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change, eds. C. B. Field et al., Table SM10.2 (2014), http://www.ipcc.ch/pdf/assessment-report/ar5/wg2/supplementary/WGIIAR5-Chap10_OLSM.pdf; and “Errata in the Working Group II contribution to the AR5,” http://www.ipcc.ch/pdf/assessment-report/ar5/wg2/WGIIAR5_Errata.pdf.

30. Roberto Roson and Dominique van der Mensbrugghe, “Climate Change and Economic Growth: Impacts and Interactions,” International Journal of Sustainable Economy 4 (2012): 270–85.

31. Martin L. Weitzman, “On Modeling and Interpreting the Economics of Catastrophic Climate Change,” Review of Economics and Statistics 91 (2009): 1–19, http://www.mitpressjournals.org/doi/pdf/10.1162/rest.91.1.1.

32. Ibid.

33. David R. Henderson, “Uncertainty Can Go Both Ways,” Regulation 36 (2013): 50–51, http://object.cato.org/sites/cato.org/files/serials/files/regulation/2013/6/regulation-v36n2-1-5.pdf.

34. William Nordhaus, “An Analysis of the Dismal Theorem,” Cowles Foundation Discussion Paper No. 1686, January 20, 2009.

35. Bob Inglis and Arthur Laffer, “An Emissions Plan Conservatives Could Warm To,” New York Times, December 28, 2008, http://www.nytimes.com/2008/12/28/opinion/28inglis.html.

36. Jerry Taylor, “The Conservative Case for a Carbon Tax,” Niskanen Center, March 23, 2015, p. 2, http://niskanencenter.org/wp-content/uploads/2015/03/The-Conservative-Case-for-a-Carbon-Tax1.pdf.

37. See David Siders, “Jerry Brown Eyes Cap-and-Trade Money for High-Speed Rail,” Sacramento Bee, January 6, 2014, http://blogs.sacbee.com/capitolalertlatest/2014/01/jerry-brown-eyes-cap-and-trade-money-for-high-speed-rail.html.

38. See “RGGI Benefits,” Regional Greenhouse Gas Initiative website, http://www.rggi.org/rggi_benefits.

39. See John Stang, “Inslee Wants to Fund Transportation with a Carbon Tax,” Crosscut, http://crosscut.com/2014/12/inslee-carbon-tax-fund-transportation-john-stang/.

40. The details of this apparent $695 billion oversight are explained in Robert P. Murphy, “Jerry Taylor Strikes Out (Again) on Carbon Tax,” Institute for Energy Research, http://instituteforenergyresearch.org/analysis/jerry-taylor-strikes-out-again-on-carbon-tax/.