The transition from socialism to the market economy produced a divide between those who advocated rapid, or “big-bang” reforms, and those who advocated a gradual approach. More than 25 years have passed since the fall of the Berlin Wall in 1989, providing ample empirical data to test those approaches. Evidence shows that early and rapid reformers by far outperformed gradual reformers, both on economic measures such as GDP per capita and on social indicators such as the United Nations Human Development Index.

A key argument for gradualism was that too-rapid reforms would cause great social pain. In reality, rapid reformers experienced shorter recessions and recovered much earlier than gradual reformers. Indeed a much broader measure of well-being, the Human Development Index, points to the same conclusion: the social costs of transition in rapidly reforming countries were lower.

Moreover, the advocates of gradualism argued that institutional development should precede market liberalization, thus increasing the latter’s effectiveness. In a strict sense, it is impossible to disprove this argument, for no post-communist country followed that sequence of events. In all post-communist countries, institutional development lagged considerably behind economic reforms. Waiting for institutional development before implementing economic reforms could easily have become a prescription for no reforms at all.

However, after 25 years, rapid reformers ended up with better institutions than gradual reformers. This outcome is consistent with the hypothesis that political elites who were committed to economic liberalization were also committed to subsequent institutional development. Conversely, political elites that advocated gradual reforms often did so in order to extract maximum rents from the economy. One extreme consequence of gradualism was the formation of oligarchic classes.

When it comes to the speed and depth of reforms, the relative position of countries has remained largely unchanged. Most countries that moved ahead early are still farthest ahead.

Introduction

More than 25 years have passed since the fall of communism. That span of time provides researchers with an enormous amount of information about the transition experiences of nearly 30 countries. It also allows for a much fuller analysis of moves from authoritarianism and central planning to democracy and market economics than had been possible in the past. This paper looks at those experiences and addresses the following questions:

What happened?

- How far has the transition process come in different post-communist countries?

- How have post-communist countries performed along three main dimensions: economic, democratic, and social?

- Earlier reviews have generally agreed that different groups of countries followed different paths, with Central Europe and the Baltics (CEB) moving and staying ahead, while others lagged behind. Is that still true today? Or have any of the lagging countries managed to break out and join the leading group?

Why did the transition happen the way it did?

- To what extent was the performance of post-communist countries related to the strategy of transition? What other factors played an important role in determining the divergent outcomes?

- Does the evidence of 25 years answer any of the key questions that have been raised in the early debates about the best way forward? These questions include the choice between gradual and rapid reforms and the sequencing of financial stabilization, market liberalization, and institutional development.

- A particularly bitter debate that continues to the present day concerns the failure or success of the so-called Washington Consensus (WC). Does the evidence available today provide any insight into that dispute?

Whither transition in the future?

- For countries where transition remains incomplete — and some have fallen very far behind — what implications can we draw from the experience of a quarter century? Are there lessons to be learned, perhaps, for Cuba, North Korea, or other countries that may begin the transition away from command economies in the future?

Before proceeding, a few clarifying remarks are in order. First, it is important to be careful with oversimplified terminology. For obvious reasons, popular writings discuss transition as a change from socialism to capitalism. To understand what had to change, what did change, and the sequencing of different reforms, we must first consider the most important political and economic characteristics of the countries in the "socialist camp."

A socialist state is characterized by authoritarianism and one-party rule. National assets are almost entirely state-owned. There is a virtual prohibition on individual market activity (large-scale buying and selling is a criminal act labelled as "speculation" in the pejorative sense of the word) and the economy is run by central planners. Transition, therefore, means a change away from these characteristics. China, for example, moved extensively, but not fully, toward private ownership and market forces, while doing little in terms of democratization. At the other extreme are the CEB countries, which embraced both free markets and democracy. Russia, Ukraine, and others ended up somewhere in the middle — with partial democratization, considerable private ownership, and a very incomplete market competition.

While this complexity may seem to pose a problem for analysis, there exists a reasonable quantitative metric called the Transition Progress Index (TPI), produced by the European Bank for Reconstruction and Development (EBRD). The TPI is measured on a scale from 1 to 4.3, with 1 representing "little or no change from a rigid centrally planned economy and 4.3 represent[ing] the standards of an industrialized market economy."1

Second, many of the more judgmental writings on transition do not use the TPI or any other quantitative indicator, but oversimplify relevant terminologies and concepts. Perhaps the most surprising example of this oversimplification is the well-known critique of transition by the Nobel laureate economist Joseph Stiglitz, who argued in 1999 that early and rapid reforms greatly harmed the social fabric in Russia. The only yardstick that Stiglitz used to argue that Russia was indeed a rapid reformer was its deeply flawed process of privatization.2

As we show later, apart from privatization of state-owned assets, Russian reforms were far less rapid than those in the CEB — a fact consistent with alternative interpretations of the Russian transition. For example, Yegor Gaidar, the acting prime minister who presided over Russia's early moves toward the free market, argued that the huge social costs imposed on the Russian population were not due to rapid reforms, but due to slow or nonexistent reforms.3

In a similar vein, it is often claimed that the decline in the GDP and hence, standard of living, was larger than that during the Great Depression. Here statistics seem to show the GDP figures falling by huge percentages — between 25 percent and 50 percent from the pre-transition high in 1989. According to some estimates, in countries such as present-day Ukraine, GDP is supposed to be only about 90 percent of what it had been before the transition. Anyone who remembers Ukraine in 1989 and saw the country change over the next 25 years will not believe that for a moment.

There are two important reasons why GDP estimates exaggerate the post-communist decline and underestimate the subsequent growth. The Soviet measure of output (the so-called "Net Material Product") overstated real values due to the well-known distortions of the communist system of central planning. By contrast, current estimates understate GDP because they omit underground economic activities.4

Third, we must be aware of inertia in the transition literature. Many studies have tended to view the effects of transition in a relatively negative light, pointing to the decline of GDP, substantial deterioration of living standards, and a considerable widening of the income-distribution gap. The early and inevitable costs of transition were best described by the Hungarian economist Janos Kornai in 1994.5 As Kornai argued, a recession would be necessary before a new market system could deliver benefits because of the "soft-budget" system, whereby any factory losses were automatically paid for from the state budget. As a result of the soft-budget system, ex-communist economies were overindustrialized, highly inefficient, and subject to considerable overemployment in the form of nonproductive labor.

Kornai's views were widely discussed by scholars. Surely, therefore, a period of deterioration after the collapse of communism was thus to be expected. Researchers should have understood that studies covering only the early years of transition were bound to show only the "bad" part of Kornai's cycle. As time went on, economies in ex-communist countries improved, and comprehensive reviews of transition became more positive. By then, however, the transition process became less interesting to both the public and academics. Hence, rather unfortunately, the early writings remained better known and the somewhat negative perception of the transition process persists to the present day. Thus, Thomas Piketty of the Paris School of Economics writes in his Capital in the Twenty-First Century, "The Asian financial crisis . . . convinced many countries including Indonesia, Brazil and Russia that the policies known as ‘shock therapies' dictated by the international community were not always well advised."6

A major purpose of this paper is to correct misperceptions created by what were surely premature analyses of the early 1990s.

A Brief Review of the Literature on Transition So Far

Conclusions of earlier reviews, which began to appear in the mid-1990s, pointed to a sharp decline in GDP and were quite negative. In 1996, Peter Murrell of the University of Maryland noted the increased poverty in transition countries.7 In 1996, Mathias Dewatripont of the Université Libre de Bruxelles and Gérard Roland of the University of California — Berkeley, came to a similar conclusion.8 In 1998, Branko Milanovic from the World Bank wrote about the sharp widening of income distribution.9 Also in 1998, the United Nations Development Programme (UNDP) noted a decline in the overall standard of living.10 All were concerned that big-bang reforms were too harsh and caused massive social pain.

In 1999, Joseph Stiglitz, then chief economist at the World Bank, spearheaded this new criticism of the so-called Washington Consensus. The term "Washington Consensus" refers to a set of economic policy prescriptions for developing countries promoted by Washington, D.C.–based institutions, including the International Monetary Fund (IMF), the World Bank, and the U.S. Treasury Department. The policy prescriptions included macroeconomic stabilization, liberalization of trade and investment, and the expansion of competition within the domestic economy.11 As Stiglitz argued, "big-bang," or rapid and deep reforms, should give way to a more gradual liberalization that would ease the pain of transition. He further argued in favor of institutional development. He was particularly emphatic with regard to Russia, where he saw big-bang reforms leading to great political turmoil. However, it is significant that even he and other strong critics of the big-bang approach to reforms did accept the primacy of financial stabilization, which formed a major part of the International Monetary Fund's transition programs.12

Overall, studies done in the 1990s concluded that early and rapid reformers were causing undue social pain and that big-bang reforms needed to be reconsidered. In the following section, we will review those criticisms on the basis of 25 years' of evidence.

Following the start of the new millennium, new analyses began to tell a somewhat less negative story. Already in 1999, Milanovic noted that deteriorating income distribution and poverty rates were not nearly as bad in CEB as in the countries further to the east and south. In 2002, Jan Svejnar of Columbia University was also concerned about social pain in the early years of transition, but argued that it was far less severe in CEB.13 He concluded that the superior performance of the CEB countries may have been related to early and rapid reforms. Importantly, Svejnar also added that CEB's economic performance was much better than that in the former Soviet Union (FSU) countries. In many CEB countries, GDP recovered as early as 1993 and 1994. Foreign investments began to flow in by the mid-1990s, and export growth and diversification to Western Europe were both evident by that time as well.14

In 2003, Leszek Balcerowicz, who presided over the early Polish reforms as deputy prime minister and minister of finance, was among the first economists to argue that CEB performed better not because of luck, geographic location, or accession talks with the EU, but because the CEB undertook early financial stabilization and rapid and resolute market liberalization. In a word, CEB pursued the big-bang strategy.15 Another of the key architects of rapid reform, Václav Klaus, who was the minister of finance of Czechoslovakia and later prime minister and president of the Czech Republic, made a similar case in 2006.16 Analyzing 15 years of data, Havrylyshyn concluded in a study in 2007 that countries that undertook early and rapid reforms achieved the best results.17

The critics of the big-bang, however, remained unconvinced. By the middle of the first decade of the new millennium, transition was so close to completion (at least in the CEB countries) that the excitement among social scientists about this singularly unique historical experiment had waned. Thus, the audience for newer studies was quite small. Furthermore, some of the stars of the transition process, such as Estonia and Latvia, were hit hard by the Great Recession. And strangely, big-bang reforms in Poland were not credited for the fact that Poland emerged from the Great Recession unscathed.

Testing the Major Hypotheses on Transition

In spite of the availability of conventional statistics and the newer category of quantitative indicators of institutional quality (including ratings of democracy, corruption, and the rule of law), it is surprising and unfortunate how superficially quantitative indicators have been used in the literature. Sometimes, the literature even confuses quantitative indicators of progress toward a market economy with those of economic performance. To avoid similar misinterpretations, we make a clear distinction between "input" variables, or policies that moved countries from central planning to the market system, and "output" variables, or actual economic performance results. The correlation between input variables and output variables will allow for the most objective testing of various hypotheses about the optimal transition strategy.

Measuring the Inputs: Progress toward Market Democracy

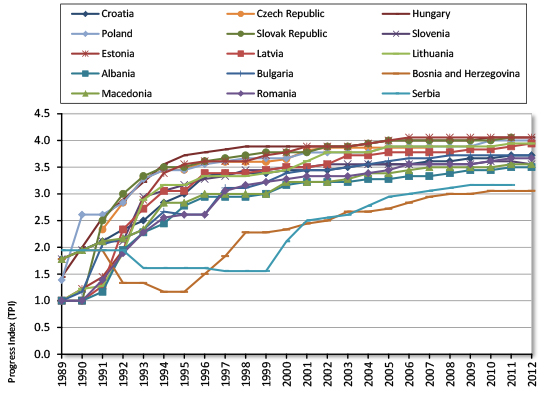

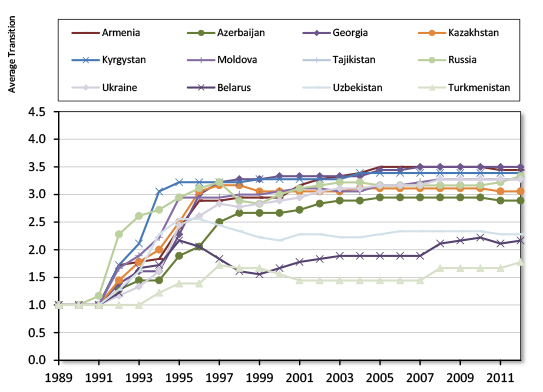

As discussed, the TPI measures progress toward a market economy in such areas as privatization of large-scale and small-scale enterprises, price liberalization, trade and foreign exchange liberalizations, interest-rate liberalization, banking and competition policies, and others.18 While imperfect, the TPI is broadly accepted by transition specialists as a reasonable indicator of the relative position of transition countries on the path toward the free market. Happily, the data goes back all the way to 1989 (see Figure 1).

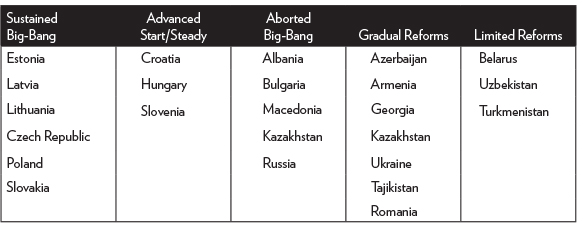

Since Figure 1 may be a little too busy to follow differences among countries, we have divided transition countries into groups. These groups are based on their speed of transition in the first few years after the collapse of communism (see Table 1, "Transition Countries Grouped by Early Reform Strategies" Table 1). Countries that increased their score by at least one point in the first three to four years are grouped as rapid reformers. Clearly, Poland, Czechoslovakia (later the Czech Republic and Slovakia), and Hungary belong in that group.

Croatia and Slovenia, which started from a more advanced position because of a lower level of centralization in the former Yugoslavia, did not increase their score as early as the four Central European countries, but caught up to the rapid reformers by 1995. Hence Croatia and Slovenia should also be considered rapid reformers.

Following the dissolution of the USSR in 1991, the three Baltic countries quickly caught up with Central Europe and should also be counted as rapid reformers. The other FSU countries reformed more slowly and at varying speeds. The EBRD score of the laggards (Belarus, Turkmenistan, and Uzbekistan), for example, has never exceeded 2.5.

A special case that has caused a lot of misunderstanding is Russia. Its huge leap forward between 1991 and 1994 approximates that of Poland, but Russia's transition was not sustained. Yegor Gaidar's 1992 reforms soon ran into opposition and he was removed from government. Some of his reforms were eventually reversed. For that reason, Russia is categorized in Table 1 as an "aborted big-bang" country. Unfortunately, much of the writing about Russia does not recognize that the big-bang reforms were short-lived and then reversed.

In Figure 1, the graph on the top indicates the transition progress of Central European, Southeast European, and Baltic countries. The graph on the bottom indicates the transition progress in the rest of the former USSR.19

Several characteristics of the transformation process are worth noting. First, there was a wide divergence among countries. Most countries started at the lowest level of 1.0 (with Hungary and Yugoslavia in slight lead because of a lower level of centralization). By 1995, the transition values spread widely and that widening tendency has continued to the present. While Poland's big-bang reforms were the first among transition countries, the rest of Central Europe and the Baltics caught up with Poland by the middle of the 1990s. Within the FSU, Ukraine stands out as an early laggard, delaying any reforms until 1994, although Georgia was also quite slow in starting its reforms. In contrast, Belarus under Prime Minister Vyacheslav Kebich started to reform earlier than Ukraine. In 1994, however, Alyaksandr Lukashenko became Belarusian president and led the country back to an essentially Soviet economic regime.

Figure 1. Progress toward a Market Economy in Ex-communist Countries

Source: European Bank for Reconstruction and Development, "Forecasts, Macro Data, Transition Indicators," http://www.ebrd.com/what-we-do/economic-research-and-data/data/forecast….

Despite some notable special cases, the broad pattern of transition for different groups of countries was established in the first years after the fall of communism and has largely held to the present day. This pattern is best reflected in Figure 2, where we have slightly modified the groupings from Table 1, "Transition Countries Grouped by Early Reform Strategies"Table 1. We separated Central European and Baltic countries because the Baltic countries were a part of the USSR and started the transition process slightly later than Central Europe. Apart from the two Yugoslav economies of Croatia and Slovenia, which we have grouped with Central Europe, the rest of South-East Europe started to transition much later. That was partly due to the Yugoslav wars and partly due to policy decisions.

Table 1. Transition Countries Grouped by Early Reform Strategies

Source: Oleh Havrylyshyn, Divrgent Paths in Post-Communist Transformation: Capitalism for All or Capitalism for the Few? (Houndmills, UK: Palgrave MacMillan, 2006), p. 10, Table 2.

Note: Slovakia underwent rapid economic reforms between 1990 and 1992, when it was a part of the Czechoslovak federation.

Figure 2. Transition Values by Country Groups between 1989 and 2013 Source: European Bank for Reconstruction and Development, "Forecasts, Macro Data, Transition Indicators,"

Source: European Bank for Reconstruction and Development, "Forecasts, Macro Data, Transition Indicators," http://www.ebrd.com/what-we-do/economic-research-and-data/data/forecasts-macro-data-transition-indicators.html.

Note: CE = Central European; SEE = Southeast European; FSUREF = Former Soviet Union, gradual reforms; FSULAG = Former Soviet Union, lagged reforms.

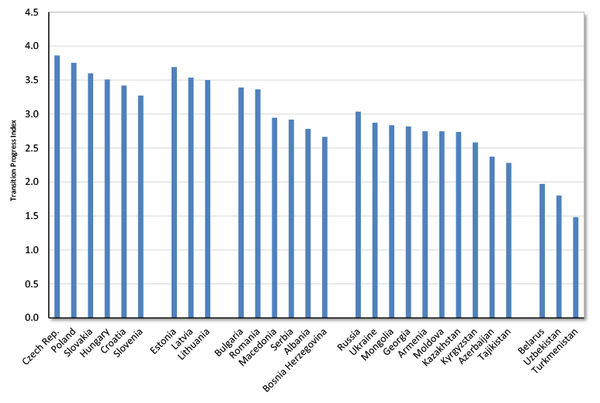

By 2013, as Figure 3 shows, Bulgaria and Romania improved greatly. That was probably because of the effects of the EU accession talks that we will discuss later. Figure 3 also confirms the distinction between the nine former Soviet republics that undertook gradual, but real, reforms (FSUREF), and those former Soviet republics where reforms lagged (FSULAG). One of the main conclusions of this paper is that speed and outcomes of transition were largely set in the early 1990s. Countries that started early generally continued to move forward. They remain leading achievers to this day.

Figure 3. Transition Scores of Countries by Group and Rank in 2013

Source: European Bank for Reconstruction and Development, "Forecasts, Macro Data, Transition Indicators,"

http://www.ebrd.com/what-we-do/economic-research-and-data/data/forecasts-macro-data-transition-indicators.html.Note: CE = Central European; SEE = Southeast European; FSUREF = Former Soviet Union, gradual reforms; FSULAG = Former Soviet Union, lagged reforms.

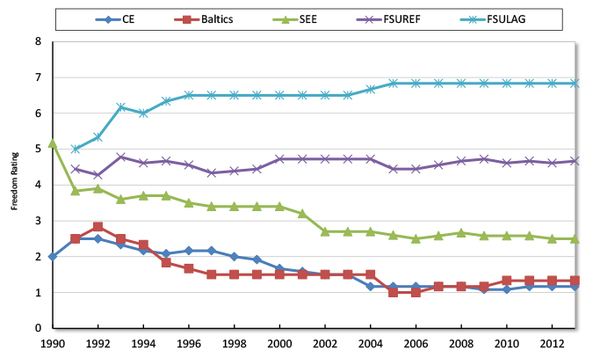

Let us now turn to democratization. There are many quantitative measures of democratization, but they all show similar patterns. Figure 4, for example, shows data from the American nongovernmental organization Freedom House, which ranks political freedom around the world on a scale from one (most free) to seven (least free). Two key observations merit attention. First, Central European and Baltic countries saw the most dramatic improvements in terms of political freedom. Conversely, political freedom in the laggard countries is worse than in the dying days of communism.

Figure 4. Freedom Rating by Country Groups, 1990–2013

Source: Freedom House Database,

https://freedomhouse.org/report-types/freedom-world.Note: CE = Central European; SEE = Southeast European; FSUREF = Former Soviet Union, gradual reforms; FSULAG = Former Soviet Union, lagged reforms.

Second, the ordering of country groups by democratization mirrors the ordering of country groups by market liberalization. As Gérard Roland and Daniel Treisman from the University of California–Los Angeles show, there is a close correlation between the two processes.20

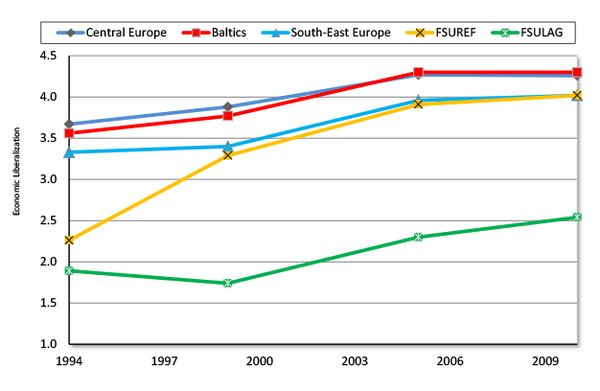

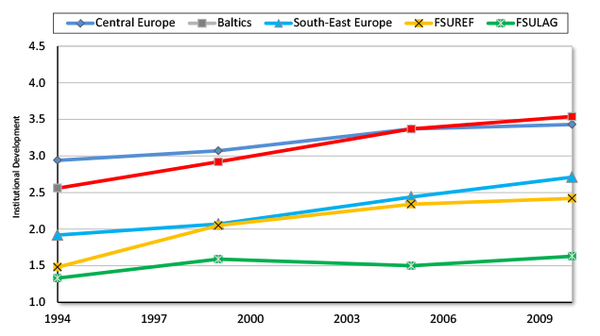

Let's now look at institutional development. The World Bank's World Governance Indicators and Doing Business Reports, and Transparency International's Corruption Perception Index, offer a full look at institutional development in transition countries. But the EBRD's data on institutional development has the great advantage of being available for a much longer period of time. Analysts might be comforted by the high correlation among all the indexes during the times when it can be measured. Using the EBRD data, therefore, we have constructed a comparison between market liberalization and institutional development.

In Figure 5, "Economic Liberalization" denotes progress made by ex-communist countries in the areas of small-scale privatization, price liberalization, and trade and foreign exchange liberalizations. "Institutional Development" denotes progress made by ex-communist countries in the areas of large-scale privatization, enterprise restructuring and governance, competition policy, banking reform, and reform of securities markets and nonbank financial institutions.

The critics of the big-bang approach to reform have often pointed to the lack of attention paid to institutional development. Many have gone further, saying that institutions should have come first to ensure that liberalized markets functioned most efficiently. We will look at that debate below.

In the meantime, data shows that even the leaders in institutional development have not come close to achieving scores in this area as impressive as they have achieved in the area of market liberalization. To give one example, in 2010 the Baltic countries, which performed the best in terms of economic liberalization out of all the ex-communist countries, scored the maximum 4.3. But that year the Baltics only scored 3.54 out of the possible 4.3 in terms of institutional development.

Figure 5. Comparison between Market Liberalization and Institutional Development

Source: European Bank for Reconstruction and Development, "Forecasts, Macro Data, Transition Indicators,"

http://www.ebrd.com/what-we-do/economic-research-and-data/data/forecasts-macro-data-transition-indicators.html.Note: CE = Central European; SEE = Southeast European; FSUREF = Former Soviet Union, gradual reforms; FSULAG = Former Soviet Union, lagged reforms.

Nonetheless, the countries that moved fastest on institutional reforms were the very same countries that also moved fastest on market liberalization, even if the two types of reform progressed at unequal rates. Importantly, countries that delayed market liberalization did not move faster in terms of institutional development. There was no apparent trade-off between them. Thus we continue to see the ordering of country groups established at the outset. Countries that led in terms of economic liberalization also led in terms of democratization and even institutional development.

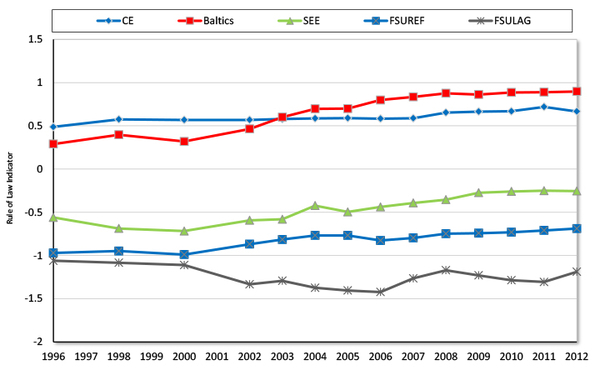

Today, a vast array of much more sophisticated institutional indicators exists. Let us look at some of them. Figures 6 and 7 show the average rule of law scores of our country groupings as measured by the World Bank's World Governance Indicators, and the extent of corruption as measured by Transparency International's Corruption Perception Index.

The corruption indicator is not an input per se. Rather, it is an output. However, corruption reflects a vast array of economic and legal changes — with good policies resulting in minimal corruption and bad policies leading to extensive corruption. As World Bank researchers have recognized, therefore, corruption is a good proxy for overall institutional quality.21

Once again, we find that early leaders in market liberalization performed better than other countries on measures of institutional quality. Within each group, we see some variation, of course. Thus Croatia scores far below the Central European average. That said, the country's overall trend is positive. In the 1990s, Croatia's institutional quality was similar to that of other Southeast European countries. By 2007, Croatia's institutional quality was far superior to that in the rest of Southeast Europe as well as the FSU countries.

When it comes to the Baltic countries, all were close to each other from the beginning of transition, even though Estonia was always in the lead. In the FSUREF group, Georgia has improved the most following the Rose Revolution in 2003. That was dramatically reflected in Georgia's rankings in the Doing Business and Corruption Perceptions Indexes. In the former, Georgia rose from 112th place in 2006 to 37th place the following year. In the latter, Georgia moved from 134th place in 2004 to 51st place in 2012 — ahead of some EU countries. Moldova had the second-most improved institutional environment.

Figure 6. World Bank's Rule of Law Indicator by Country Group, 1996–2010

Source: World Bank, "World Governance Indicators," http://databank.worldbank.org/data/reports.aspx?source=world-developmen….

Note: CE = Central European; SEE = Southeast European; FSUREF = Former Soviet Union, gradual reforms; FSULAG = Former Soviet Union, lagged reforms.

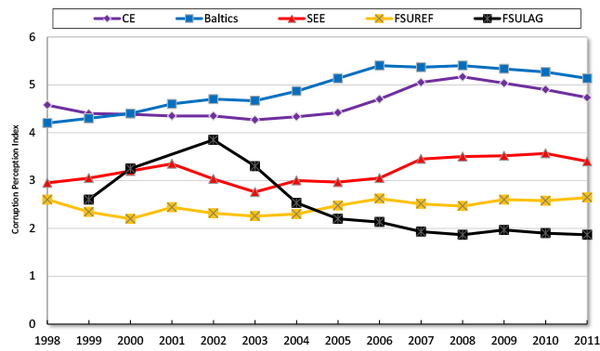

The Corruption Perception Index tells the same story. The CEB did much better from the start and continued to improve. The FSUREF countries show limited improvement throughout the transition period. Indeed, there was a slight tendency in some countries to worsen after 2000 (e.g., Russia and Ukraine). As for the FSULAG countries, Figure 7 shows an anomalous improvement between 1998 and 2002, but that improvement may have been due to a measurement error.22 Whatever the explanation, after 2000 these lagging and very authoritarian countries continued to score very poorly on corruption.

Figure 7. Transparency International's Corruption Perception Index by Country Group, 1998–2011

Source: Transparency International, "Corruption Perception Index,"

http://www.transparency.org/research/cpi/overview.Note: CE = Central European; SEE = Southeast European; FSUREF = Former Soviet Union, gradual reforms; FSULAG = Former Soviet Union, lagged reforms.

Measuring the Outputs: Economic and Social Performance

Here we start by looking at the change in GDP per capita for the entire sample of 29 transition countries.23 Some have argued that rising incomes do not tell the full story. Income inequality, for example, rose as well. As such, we will look at both income distribution and other proposed measures of social well-being.

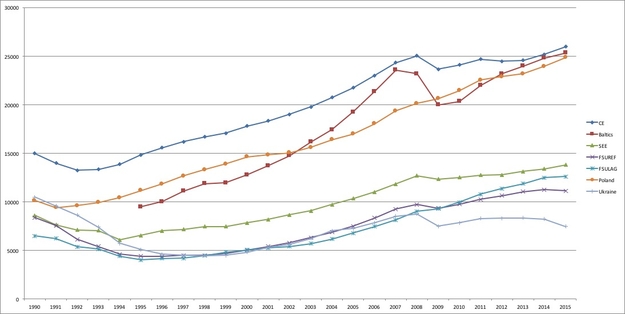

igure 8 shows the evolution of GDP per capita in constant 2011 U.S. dollars adjusted for purchasing power parity for different groups of transition countries between 1990 and 2015. The similarity between Figure 2, which traces market liberalization, and Figure 8, which traces income, is striking. Clearly, countries which moved early and rapidly on market liberalization (and we now know from Figure 5 that they also moved fastest on institutional development) also performed the best on GDP per capita. In addition to including Poland and Ukraine in their respective groups of countries, we have included them as standalone countries. The contrast between rapid and gradual reformers is striking. As we have already noted, Ukraine delayed any reforms for a number of years and then embraced only gradual change. As we explain later, postponement of reform proved to be an opening for rent-seeking and the rise of oligarchs. The Ukrainian example is significant not only because of the current visibility of Ukraine, but also because it shows what happens when reforms are postponed. As noted, Ukrainians (especially of the younger generation) see a big difference in performance between their country and the CEB group. They seem to relate Ukraine's poor performance to too few reforms, rather than to too many reforms.

Figure 8. GDP per Capita by Country Group, 1990–2015 (in 2011 U.S. Dollars Adjusted for Purchasing Power Parity)

Source: World Bank, "World Development Indicators," http://data.worldbank.org/indicator/NY.GDP.PCAP.PP.KD.

Note: CE = Central European; SEE = Southeast European; FSUREF = Former Soviet Union, gradual reforms; FSULAG = Former Soviet Union, lagged reforms.

In addition to including Poland and Ukraine in their respective groups of countries, we have included them as standalone countries. The contrast between rapid and gradual reformers is striking. As we have already noted, Ukraine delayed any reforms for a number of years and then embraced only gradual change. As we explain later, postponement of reform proved to be an opening for rent-seeking and the rise of oligarchs. The Ukrainian example is significant not only because of the current visibility of Ukraine, but also because it shows what happens when reforms are postponed. As noted, Ukrainians (especially of the younger generation) see a big difference in performance between their country and the CEB group. They seem to relate Ukraine's poor performance to too few reforms, rather than to too many reforms.

Of course, skeptics would not be incorrect to point out that so far we have only given a post hoc, ergo propter hoc argument in favor of rapid reforms. In fact, early econometric studies, including a 1996 paper by Stanley Fischer, Ratna Sahay, and Carlos Vegh of the International Monetary Fund, found that reforms had a strong effect on economic growth — as did good institutions.24 Treisman confirmed those early findings in 2014.25

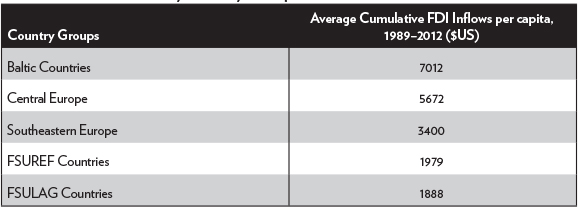

Let us now turn to foreign direct investment (FDI). Ordinarily, countries that attract more FDI per capita do so because of a better investment climate. Such countries will then benefit from higher economic growth and strong export performance. Table 2, "Cumulative FDI Inflows by Country Group, 1989–2012"Table 2 shows that the more reform-oriented country groups achieved much higher FDI inflows. The values shown are not annual. Instead, they show a cumulative total since the ex-communist countries opened up to global trade and investment. The differences between countries are overwhelming, with the two reformist blocs receiving much more than the rest of the ex-communist countries.

The similarity between the amount of FDI flowing into gradual reformers and laggards may seem surprising. A large part of the explanation rests with Turkmenistan's enormous gas reserves. As always, petroleum attracts large investments, notwithstanding the nature of the political regime. And that raised the FSULAG average. In a strange contrast, Russia has received little FDI, in spite of having large petroleum reserves. That happened because Russia has pursued a policy of maximizing state control over the oil reserves and also because Russia does not provide an attractive investment climate for its very large, and relatively advanced, manufacturing sectors.

Table 2. Cumulative FDI Inflows by Country Group, 1989–2012

Source: European Bank for Reconstruction and Development Transition Report 2009 and World Bank World Development Indicators,

http://www.ebrd.com/downloads/research/transition/TR09.pdf and http://data.worldbank.org/indicator/BX.KLT.DINV.CD.WD.

There is also a high degree of correlation between market liberalization and export performance. According to a 2005 study by Harry Broadman of the World Bank, rapid reformers were fastest in reaching "normal" trade-to-GDP ratios.26

Let us now turn to the social outcomes of transition. Observers of the transition process will recall the heated discussions about the social pain that rapid reforms were supposed to have caused and the soul-searching about the optimal transition strategy to follow. Thus Adam Przeworski, an expert on Latin American democracy, wrestled with what he saw as a potential inconsistency between democracy and rapid economic reforms. The Przeworski hypothesis stated that rapid economic reforms would inevitably cause a lot of pain to the population. Given the newly established democratic decisionmaking, the reformist governments, Przeworski reasoned, would lose in the next elections and economic reforms would be reversed or at least halted. As we explain in the next section of this paper, Przeworski's hypothesis was only half right.27

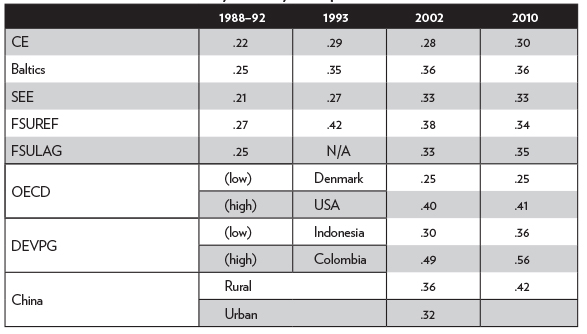

Now consider three specific social indicators: inequality, poverty ratios, and the United Nations' Human Development Index (HDI). Table 3 summarizes, by country groups, the trends in inequality as measured by the Gini coefficient. The Gini coefficient measures the income distribution among country's residents. The coefficient ranges from zero, which indicates complete equality (i.e., everyone's incomes are perfectly equal) to one, which indicates complete inequality (i.e., one person has all the income in the country). Note first that the Gini coefficient in the socialist camp was much lower than in most market economies — with a partial exception of the Nordic countries. But it is also notable that the Gini coefficient was higher in the FSU than in Central Europe. While the official Soviet estimates implied a Gini coefficient in the low .20s, scholars found that these were largely based on urban estimates. Searching through internal writings by Soviet academics, scholars have discovered that rural and low-income regions had a much wider income distribution.

Table 3. Trends in the Gini Coefficient by Country Group

Source: The first three columns come from Oleh Havrylyshyn, Divergent Paths in Post-Communist Transformation: Capitalism for All or Capitalism for the Few? (Houndmills, UK: Palgrave MacMillan, 2006), p. 106, Table 3.9. All 2010 values come from the World Bank, "World Development Indicators,"

http://databank.worldbank.org/data/reports.aspx?source=world-development-indicators.Note: CE = Central European; SEE = Southeast European; FSUREF = Former Soviet Union, gradual reforms; FSULAG = Former Soviet Union, lagged reforms; OECD = Organisation for Economic Co-operation and Development; DEVPG = Developing Countries.

Table 3 includes adjusted figures for the FSU. Clearly, all transition countries saw a widening of income distribution. That was to be expected, given the earlier artificial suppression of different outcomes and the lack of capital-based income for individuals. However, the extent of the widening was by far greater in the gradual and lagging reformers. That is consistent with the early finding of Branko Milanovic, who showed in 1999 that the "worst" deterioration of income distribution was not in the Central European countries, but in the FSU.28 Moreover, the Gini coefficient has started to shrink in recent years, but less so in the gradual or non-reforming countries.

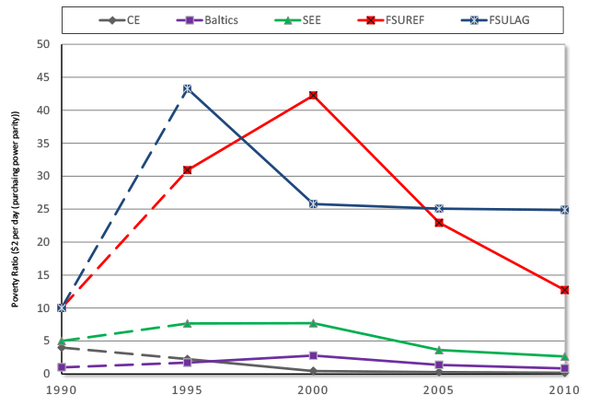

A similar story can be told by looking at an alternative indicator of distribution of income: the poverty ratio (i.e., the share of the population living on less than $2.00 a day adjusted for inflation and purchasing power parity) (see Figure 9). The differences between rapid reformers on the one hand, and gradualists and laggards on the other hand, are dramatic. All ex-communist countries saw some worsening at the outset of the post-communist recession that lasted from about 1990 to about 1995. All experienced a return to lower poverty ratios. But the gap between country groups is far greater than was the case with the Gini coefficient. The Central European and Baltic countries, and even the countries in Southeast Europe, saw their poverty ratios remain at very low levels, while both FSU groups peaked at more than 40 percent before falling back again, although gradualists and laggards have yet to match the other groups by this measure. This evidence strongly confirms the view that rapid reforms caused less — not more — transitional poverty than gradual reforms.

Figure 9. Poverty Ratio at Two Dollars per Capita per Day by Country Group

Source: World Bank, "World Development Indicators,"

http://databank.worldbank.org/data/reports.aspx?source=world-development-indicators. The 1990 estimates (dashed lines) are from Oleh Havrylyshyn, Divergent Paths in Post-Communist Transformation: Capitalism for All or Capitalism for the Few? (Houndmills, UK: Palgrave MacMillan, 2006), p. 105, Table 3.8.Note: CE = Central European; SEE = Southeast European; FSUREF = Former Soviet Union, gradual reforms; FSULAG = Former Soviet Union, lagged reforms.

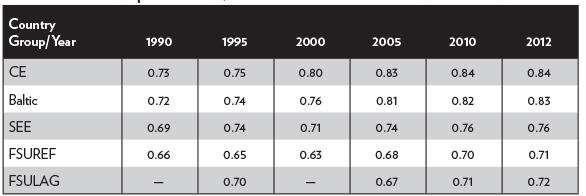

An even more compelling piece of evidence for the last conclusion comes from the UNDP's Human Development Index. Like all subjective or composite indices that have become common over time, the HDI has its problems. Still, the HDI provides a fuller picture of human well-being than GDP per capita alone. Thus, in addition to GDP per capita, the HDI includes measures of life expectancy and education.

When it comes to social conditions, all transition countries suffered some initial deterioration as incomes fell and unemployment rose. But this deterioration was quite minimal in Central Europe. By the mid 1990s, HDI was on the rise again. Once again, the Baltic countries performed better than other ex-Soviet countries. By 2000, reforming countries reached their pre-transition levels. In contrast, the HDI in FSUREF countries only started to recover in 2000, while HDI in FSULAG countries continued to fall until at least 2005 (see Table 4).

To sum up, different measures of "outputs," covering many dimensions of economic, political, and social life, consistently point in the same direction — early and rapid reformers outperformed those countries that moved more gradually.

Table 4. The Human Development Index, 1990–2012

Source: UNDP's Human Development Index at http://hdr.undp.org/en/data, accessed September 12, 2014. Values of the Index range from 0 to 1. The higher values denote a higher level of well-being.

Note: CE = Central European; SEE = Southeast European; FSUREF = Former Soviet Union, gradual reforms; FSULAG = Former Soviet Union, lagged reforms.

The only significant anomaly concerns the relative performance of the three FSULAG countries compared to the FSUREF countries. A literal interpretation of the positive correlation between reforms and performance would imply worse performance among the laggards than among gradual reformers. After all, FSULAG progress toward the market was even slower than that of FSUREF. The slightly better economic performance of the laggards remains one of the still-unresolved puzzles of the transition period. Many writers have suggested possible explanations. Turkmenistan, for example, has large gas reserves that can pay for the policy mistakes of the Turkmen government. Belarus receives direct and implicit subsidies from Russia amounting to between 10 percent and 20 percent of GDP. Even then, however, Russian subsidies do not fully resolve the Belarusian puzzle. Still, these very special cases are not enough to undermine the overall trend.

Seven Key Findings after a Quarter Century of Transition

Let us now sum up our main findings. The first key finding is that, with the exception of Belarus, all the non-Asian post-communist transition economies have moved a long way from centrally planned socialist regimes towards market-based capitalist systems. Indeed, the Czech Republic, Slovakia, Poland, Hungary, Estonia, Latvia, and Lithuania can be said to have completed their transitions. Gérard Roland and the EBRD differ from the above assessment by pointing to lagging institutional development in Central Europe and the Baltic countries.29 We will tum to this issue below.

Second, the EBRD data shows sharp divergence between the most advanced countries and the slower reformers. While all ex-communist countries started from about the same position (that is, very far from a market economy), by the mid-1990s the differences among them were huge and kept growing. It is important to note that the gap grew because countries that led from the start continued to move resolutely forward, while the gradualists moved less quickly.

Third, the basic pattern — of who led the reform process and who lagged behind — was set within the first four to five years. It has stayed that way ever since, with, perhaps, one significant exception: Georgia has been steadily catching up after its 2003 Rose Revolution.30 Because of their late start due to the Yugoslav wars, several of the former Yugoslavia states, despite their more market-oriented status at the beginning of the 1990s, were surpassed by the gradual reformers of the FSU. But once the wars stopped, the ex-Yugoslav countries moved faster in an effort to catch up to the transition leaders in Central Europe and the Baltics.

Fourth, institutional development in ex-communist countries did, in fact, lag behind economic liberalization. However, no country has followed the recommendation of the advocates of gradualism and put in place good institutions before liberalizing (although many leaders in the gradual and lagging countries explained the delays by saying that they must first develop good institutions). Thus, the leaders of both Belarus and Uzbekistan have frequently stated that their aim was a so-called "social market economy" and that the first stage of this process involved development of conditions in which markets can function properly. From the late 1990s, some countries started to move a little faster in terms of institutional development, but those countries were not gradualist. In fact, countries that moved the fastest and farthest in terms of institutional development turned out to be the very same countries that had moved earliest and most forcefully in terms of market liberalization.

Fifth, the CEB countries that led in market liberalization have also followed a consistent path to democratization. This is important because democratization and economic transformation are linked. In sharp contrast to the CEB countries, the FSUREF countries implemented only partial democratization. Most of the FSUREF members started to revert to authoritarianism. In the FSULAG, this lack of democratization was fairly explicit and extreme. For the FSUREF, it was more subtle, with a formal electoral process legally permitting many parties. In practice, democracy was so restricted by the incumbent government that it came to be labelled by political scientists as "managed democracy." This failure to democratize and the excesses of the oligarchs led in many countries to popular resentment, demonstrations, and the so-called "color revolutions." A number of these color revolutions initially succeeded — at least to the extent of overthrowing the existing governments in Serbia (2000), Georgia (2003), Ukraine (2004), and the Kyrgyz Republic (2005). However, only in Georgia did the color revolution lead to real changes in the economic direction of the country.

Sixth, transition in some countries has led to the rise of an oligarchic class, which uses nontransparent means to influence policy, protects its monopoly-like status, and impedes a truly open and competitive market economy. The use of money in market economies for lobbying in order to obtain special treatment with regard to taxes, licenses, and exemptions is well-known historically and internationally. Oligarchic support for favored political parties or entities is also not unique to ex-communist countries. What troubles a lot of observers of transition is that oligarchs in ex-communist countries go far beyond the usual rent-seeking activities and use their influence to determine the general philosophical direction of government, reform policies, and geostrategic decisions.31

There is some evidence that oligarchies are stronger in countries that followed gradual and slow reforms. For example, the Baltic countries and CEE have 0.11 and 0.255 billionaires per million inhabitants, respectively. The FSUREF region, in contrast, has 0.485 billionaires per million inhabitants, or twice as many as those in CEE. Delays in liberalization, in other words, seemed to have allowed for stronger oligarchy formation and entrenchment.32

Seventh,"inputs and output" are positively correlated. Countries that did the most to liberalize achieved the highest GDP per capita increases, experienced the least widening income distribution, suffered the lowest poverty ratio increase, and achieved the best scores in the HDI. It should also be noted that non-GDP performance more or less mirrored GDP performance. That is to say, all countries that saw a decline in output in their first years experienced a worsening of welfare and a widening of the income gap between rich and poor. Yet as soon as GDP recovery began, social deterioration stopped. Since the early reformers were the first to experience a recovery of economic output, they also experienced the least social costs. They were additionally the first to enjoy the benefits of transition — higher income, an end to shortages, access to a wide variety of goods, and improved quality of goods.

Why Transition Happened the Way It Did

The most important question facing ex-communist nations was whether to opt for gradual or rapid reforms. If economic performance is the main measure of success, the data speaks loudly. Countries that moved early and rapidly on reforms have performed far better. Why?

As Anders Åslund of the Atlantic Council, Peter Boone of the London School of Economics, and Simon Johnson of Duke University noted in 1996, notwithstanding the mathematical sophistication and elegance of gradualist models, big-bang reforms worked better because of the political economy in ex-communist countries.33As these authors correctly understood, the former communist elites in gradualist countries generally accepted that a new capitalist regime was inevitable, but they wanted to retain their privileged or ruling status. Soon, they enriched themselves through corrupt privatization schemes. In a word, the gradualist model was too easily abused.

Moreover, rapid reforms, including price liberalization, trade liberalization, and business deregulation, quickly induced resource reallocation from inefficient communist dinosaurs to new firms, and that led to an early recovery of output. Even in Poland and Slovenia, where the privatization of large state enterprises was long delayed, economic recovery came between 1993 and 1994.34 The huge social pain of much longer recessions in the gradualist countries should not be underestimated. Certainly the continued decline of HDI values in the FSU suggests that the social pain was considerable.35

As mentioned, institutional development in big-bang countries lags behind market liberalization, although it trends upward. The extensive literature on the New Institutional Economics (NIE) clearly shows that institutions matter. But they matter more for sustaining growth over the long term than for jumpstarting growth after a recession. So a complete establishment of good institutional structure was not initially needed. That it took centuries, not years, to build institutions in today's advanced market economies is one of the key lessons from the pioneer of the NIE school, the Nobel laureate economist Douglass North.36 Just how much institutional development is needed to restart growth remains an unanswered question, but it is clear that the progress achieved by the mid-1990s in the CEB group was sufficient to sustain a comparatively higher rate of growth (see Figure 5).

The evidence on sequencing also points to the fact that political leaders in gradualist countries may have been less than sincere. In spite of their frequent protestations that going slowly was necessary to allow time to build proper market institutions, nothing of the sort has happened (see Figure 5). There is not a single case of a country where improved institutional quality preceded liberalization.

Critics of rapid reforms contended that the stress on economic fundamentals caused international financial institutions to ignore institutional development. Again, Figure 5 contradicts that contention. The countries that took care of fundamentals early (that is, countries that achieved financial stabilization and market liberalization), also moved earlier and more resolutely in terms of institutional development.

In 2013, Christopher Hartwell of the Center for Social and Economic Research in Warsaw offered a detailed history of the actual sequence of reforms that were followed in ex-communist countries, as well as the nature of the IMF, World Bank, and EBRD advice to the transition countries.37 He made a powerful counterargument against the contention that institutions were ignored. His conclusions support our view that it was not the international financial institutions or big-bang reformers who ignored institutional development, rather, it was the political leadership of the slow-reforming countries that did so.

While the promoters of the so-called Washington Consensus may or may not have had the ability to effectively push institutional development, institutional development was always recognized as an integral part of any reform program.38 Comparing the structure and the timing of the Washington Consensus recommendations with the actual path of reforms that was followed by the big-bang countries suggests that the Washington Consensus was, by and large, applied by the successful top performers.

The concern about lagging institutional development in ex-communist countries has not entirely disappeared. Many recent analyses focus on cases of advanced countries, especially the new EU member states. These analyses suggest that after their accession to the EU, the reformist drive in ex-communist countries waned — especially with regard to institutional development. Figure 5 seemingly justifies such an assessment. While economic liberalization in big-bang countries has almost reached its maximum, institutional development continues to lag behind. Thus in 2013 the EBRD argued that the pace of reforms has sharply declined. A year later, Gérard Roland warned that "reforms to improve institutions literally stopped in transition countries."39 That institutional development is not yet complete is an undeniable fact, but the above interpretations of institutional reforms overstate the problem by using the wrong benchmark.

It has been generally recognized by advocates of both gradual and rapid reforms that institutional changes cannot be done as quickly as changes in laws that allow for a more liberal market. North, as mentioned, long ago emphasized that institutional development in advanced countries took a very long time.40 By the late 1990s, EBRD reports explicitly distinguished liberalization components as the "first generation of reforms" and institutional development as the "second generation of reforms." The second, the EBRD recognized, were more complex legally and politically, and necessarily took more time.41

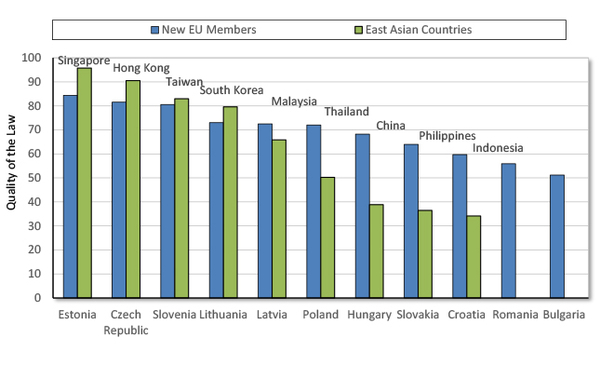

A better approach to assess the speed and status of institutional developments in big-bang countries is to compare those countries with an appropriate group of non-transition countries. East Asian Tiger economies are relevant for two reasons. First, they are market economies at about the same level of development as CEB countries. Second, they are considered very successful economies that have been among the world's leading export performers. The comparison between the two is presented in Figure 10.

Figure 10. Comparison of the Rule of Law in the New EU Member States and East Asian Countries

Source: World Bank, "World Governance Indicators,"

http://databank.worldbank.org/data/reports.aspx?source=world-development-indicators.Note: The higher values denote a higher level of well-being.

As Figure 10 shows, no matter how fast the CEB countries have moved on institutional development since the EU accession, today the CEB countries are very much in the same range of institutional development as the East Asian Tigers. Only the very mature economies of Singapore and Hong Kong rank higher.

Two additional issues about transition merit a brief consideration — privatization and the role of the EU in sustaining reforms in ex-communist countries. The share of private sector GDP is easy to measure. The CEB countries top the list with over 70 percent, and the SEE countries are not far behind. In the FSUREF countries, private sectors account for between 50 percent and 70 percent of GDP. The FSULAG are far behind, with between 25 percent and 30 percent.

The literature on privatization is large, but as Simeon Djankov of the Peterson Institute for International Economics and Peter Murrell noted in 2002, not easy to interpret.42 There is, for example, no consensus on how precisely to measure the results of privatization. Is it higher profit ratios, greater revenues, or larger productivity increases? Even so, there appears to be a consensus on some very broad and tentative conclusions.43 First, privatization by outsiders outperformed privatization by insiders. Some degree of foreign investment led to greater improvements no matter how they are measured. Second, as we have argued elsewhere, what mattered most was the transparency of privatization and avoidance of insider privileges. Third, much of the literature largely ignores the role of private sector development. How much of the increase in the private sector share of the economy was due to the creation of new enterprises as opposed to the privatization of previously state-owned enterprises? A meaningful assessment of the role played by private sector development, both new and denationalized, cannot be done without answers to this question.

The EU played an important role in promoting reforms in accession candidates, but there remains some dispute on the degree to which the prospect of EU membership worked as an external pressure toward reforms on governments in ex-communist countries. That internal commitment to reform was important is exemplified by the Baltic countries, which were not accepted into the EU accession process until 1995 — some three or four years later than the Central European countries. Yet, even without the EU membership incentive, the Baltic countries embraced far-reaching reforms. In contrast, external pressure was very effective in the case of Slovakia in 1998. Under Prime Minister Vladimir Mečiar few reforms took place and Slovakia was warned that it could be dropped from the first group of EU entrants. Partly as a result of the EU snub, Mečiar was voted out of office in the fall of 1998 and replaced by a reformist prime minister, Mikuláš Dzurinda.

Finally, let us propose a way of tying together the various aspects of transition that we have discussed in this paper and explain how they provide support for the central hypothesis — that early and speedy reforms delivered much better results, while delayed and hesitant reforms created conditions for poor performance and barriers to completion of reforms.44

Reforms may be delayed or be gradual for different reasons, but in most cases delays or gradualism happened because the preceding communist ruling class remained in power and sought to become the new capitalist class. To achieve that aim, the former communists needed time. With private ownership allowed, but market liberalization delayed or partial, arbitrage and rent-seeking opportunities were created that were most favorable to insiders. As the new capitalists developed and gradually became rich enough to acquire oligarch power, they continued to prefer a partially reformed economy, nontransparency, a privileged insider position, a monopoly-like status, and protection against new entrants based on onerous regulations for small- and medium-sized businesses. This process was also abetted by the retention of government subsidies, poor rule of law, and other institutional deficiencies. Also, EU membership requirements run exactly counter to the interests of the new oligarchy. The EU insists on competitive markets, transparency, the rule of law, and so on.

Many economists recognized the trap of this rent-seeking model, and some have argued that more privatization would eventually lead the new capitalists to demand protection of property rights and rule of law. That was an important part of the rationale for rapid privatization in Russia in the mid-nineties.45 In retrospect, it is not clear that this process evolved quite as predicted. The oligarchs discovered that their informal power provided all the protection that they needed, and that liberalization threatened their position.46 Hence they continued to influence government policy to remain within the vicious circle.

Conclusion

Twenty-five years of evidence resolves most, but not all, of the major questions concerning transition from communist dictatorship to capitalism and democracy. The main debate between rapid and gradual reformers seems to be settled in favor of the former. The empirical correlation between the speed of reforms and relevant measures of economic and social results shows that rapid reformers far outperformed gradual reformers. The argument of the big-bang proponents that delaying reforms would permit rent-seeking and state capture by the economic elite has been largely confirmed in the rise of the oligarchs. Rich capitalists have, of course, arisen in all transition economies, but their concentration and degree of political influence appears to be far higher in slowly reforming countries, in particular the large economies of the former USSR.

Moreover, trends held strongly over the past 25 years. Early reform leaders still lead, and most of the laggards still lag. Breaking out of the gradualist mold is not easy, although that was precisely what some people tried to accomplish through the various "color revolutions." Alas, only one true success story can be found. That success story is Georgia, and even the Georgian example is not a complete success.47

As to the timing of institutional development, the arguments that it should precede liberalization are not supported by the historical facts. Neither the rapid reformers, nor the international financial institutions, ignored institutional development. The fastest progress on institutions was made by the very same countries that undertook rapid liberalization.

The above does not, of course, rule out the logic of a counterfactual argument that some scholars still make today — that is, had the rapid reformers moved even earlier and faster on institutional development, things would have turned out even better. Unfortunately, no basis exists for testing this hypothesis. There has not been a single case of a country that reformed its institutions in advance of market liberalization.48

While the transition is largely over in the most advanced ex-communist countries, legal and regulatory reforms remain unfinished. The lessons from the most advanced countries are not complicated. Countries need to ensure financial stability, and to continue to deregulate and simplify their regulations in order to eliminate corruption and rent-seeking.

The countries of the former USSR are much farther behind. State capture and rent-seeking by oligarchs is high, and vested interests have a lot to lose from liberalization.49 In a few instances, where popular democratic movements created a new window of opportunity for reform (Serbia, 2000; Georgia, 2003; Ukraine, 2004; Kyrgyz Republic, 2005; and Ukraine again, 2014), governments became more amenable to reform, although the new efforts may not have always succeeded.50

Notes

This monograph is dedicated to the millions of Ukrainians who, in the cold winter of 2004, and then again in the winter of 2013, came out on the streets of Kyiv to demand their freedom and a release from the grip of abusive and self-serving politicians. In particular, may this monograph help to preserve the memory of those who gave their lives in the noble fight for freedom. We want to thank Raluca Stan, a PhD student at West Virginia University, for her early and speedy assistance with the initial data analysis.

1. For details regarding the Transition Progress Index methodology see European Bank for Reconstruction and Development, "Transition Indicators Methodology," http://www.ebrd.com/cs/Satellite?c=Content&cid=1395237866249&pagename=EBRD%2FContent%2FContentLayout.

2. Joseph Stiglitz, "Whither Reform? Ten Years of Transition," World Bank Economic Review (Washington: World Bank, 1999).

3. Anders Åslund and Simeon Djankov (eds.), The Great Rebirth: Lessons from the Victory of Capitalism over Communism (Washington: Peterson Institute of International Economics, 2014).

4. The European Bank for Reconstruction and Development, which was helpful in quantifying the process of transition progress, has nonetheless unintentionally perpetrated the myth of a huge decline in well-being in ex-communist countries after the fall of communism. The bank did so by providing in its annual Transition Reports GDP values indexed to official, but faulty, 1989 GDP figures. For a more realistic assessment of the state of Soviet bloc economies at the time of the fall of communism, see Anders Åslund, The Myth of Output Collapse after Communism (Washington: Carnegie Endowment for International Peace, 2001); and Oleh Havrylyshyn, Divergent Paths in Post-Communist Transformation: Capitalism for All or Capitalism for the Few? (Houndmills, UK: Palgrave MacMillan, 2006).

5. Janos Kornai, "The Transformational Recession: The Main Causes," Journal of Comparative Economics 19, no. 1 (1994): 34–63.

6. Thomas Piketty, Capital in the Twenty-First Century (Cambridge, MA: Harvard University Press, 2014), p. 835.

7. Peter Murrell, "How Far Has the Transition Progressed?" Journal of Economic Perspectives 10, no. 2 (1996): 25–44.

8. Mathias Dewatripont and Gérard Roland, "Transition as a Process of Large-Scale Institutional Change," Economics of Transition 4, no. 1 (1996): 1–30.

9. Branko Milanovic, Income Inequality and Poverty during the Transition from Planned to Market Economy (Washington: World Bank, 1998).

10. United Nations Development Programme, Human Development Report 1998 (UK: Oxford University Press, 1998).

11. The "Washington Consensus" by no means represents a complete set of market-oriented policy prescriptions, nor were the policies advocated by the proponents of the "Washington Consensus" all necessarily consistent with market reforms. See Ian Vásquez, "What Changes Should Be Made to the Washington Consensus?" Latin America Advisor, November 12, 2002, role="underline">http://www.cato.org/publications/commentary/what-changes-should-be-made-washington-consensus.

12. Stiglitz, "Whither Reform?"

13. Jan Svejnar, "Transition Economies' Performance and Challenges," Economic Perspectives 16, no. 1 (2002): 3–28.

14. It was common for critics to argue that this improved performance was due to the EU accession process, but foreign direct investment flows and export reorientation began very early — more than a decade before EU accession in 2004.

15. One of the biggest myths, common in Ukraine to the present day, is that some Central Europeans were invited to the EU, while others were not. Formally, there is no such thing as an "invitation" in EU law. Informally, Central Europeans were made to understand that their "association agreements" with the EU were not automatic pathways to membership. See Leszek Balcerowicz, "Post-Communist Transition Some Lessons," Institute of Economic Affairs, Occasional Working Paper no. 127, September 16, 2002.

16. Václav Klaus, "The Economic Transformation of the Czech Republic: Challenges Faced and Lessons Learned," Cato Institute, Economic Development Bulletin no. 6, February 14, 2006.

17. Oleh Havrylyshyn, "Fifteen Years of Transformation in the Post-Communist World: Rapid Reformers Outperformed Gradualists," Cato Institute, Development Policy Analysis no. 4, November 7, 2007.

18. For detailed methodology, see European Bank for Reconstruction and Development, "Transition Indicators Methodology," http://www.ebrd.com/cs/Satellite?c=Content&cid=1395237866249&pagename=EBRD%2FContent%2FContentLayout.

19. Note that values for the Czech Republic stop in 2007, when the Czech Republic left the European Bank for Reconstruction and Development. It is likely that the Czech Republic continued to improve in terms of its institutions at about the same pace as other leading reformers. Unfortunately, this expectation cannot be verified.

20. See Gerard Roland, "Transition in Historical Perspective," and Daniel Treisman, "Economic Reform after Communism: The Role of Politics," in Aslund and Djankov, eds., The Great Rebirth.

21. In econometric analyses of transition progress it is consistently found that level of corruption has a negative effect on growth, and is negatively correlated with institutional quality. See also World Bank, "Indicators of Governance and Institutional Quality," http://siteresources.worldbank.org/INTLAWJUSTINST/Resources/IndicatorsGovernanceandInstitutionalQuality.pdf.

22. Until 2004, Transparency International did not have enough information to properly evaluate Turkmenistan. Instead, the country's value was based on an average of two Former Soviet Union, lagged reforms countries.

23. In recent years the European Bank for Reconstruction and Development has sometimes added, retroactively, information on Mongolia and Kosovo, as well as, for its new mandate, several Arab Spring countries. This paper generally does not look at these.

24. Stanley Fischer, Ratna Sahay, and Carlos Vegh, "Stabilization and Growth in Transition," Journal of Economic Perspectives 10, no. 2 (1996): 45–66.

25. Treisman, "Economic Reform after Communism."

26. Harry G. Broadman, From Disintegration to Reintegration: Eastern Europe and the Former Soviet Union in International Trade (Washington: World Bank, 2005).

27. Adam Przeworski, Democracy and the Market: Political and Economic Reforms in Eastern Europe and Latin America (Cambridge: Cambridge University Press, 1991).

28. Milanovic, Income Inequality and Poverty during the Transition.

29. See Roland, Transition in Historical Perspective; and European Bank for Reconstruction and Development, European Bank for Reconstruction and Development 2013 Transition Report (London: EBRD, 2013).

30. The catch-up is less evident in the Transition Progress Index value than in other indicators. By 2012, Georgia had risen to the 19th position in the rankings of the Doing Business Report, higher than any of the Central Europe and the Baltics country. That year, Georgia ranked 19th out of 152 countries surveyed by the Fraser Institute's Economic Freedom of the World report. See James Gwartney, Robert Lawson, and Joshua Hall, Economic Freedom of the World: 2014 Annual Report (Vancouver: Fraser Institute, 2014).

31. See Havrylyshyn, Divergent Paths in Post-Communist Transformation, pp. 199–202. Havrylyshyn discusses in detail the differences between Western billionaires and post-Soviet oligarchs.

32. Authors' calculations. Also see Havrylyshyn, Divergent Paths in Post-Communist Transformation, ch. 6.

33. Anders Åslund, Peter Boone, and Simon Johnson, "How to Stabilize: Lessons from Post-Communist Countries," Brookings Institution Papers on Economic Activity 1 (1996): 217–313.

34. This process is not complete in Slovenia.

35. True, unemployment rates were much lower in the former Soviet Union, which had an unemployment rate of between 5 percent and 8 percent. Poland, in contrast, had an unemployment rate in the high teens. However, early recovery in Poland allowed unemployment benefits to be paid. In the former Soviet Union employment did not ensure wage payments (as the state sometimes did not have enough revenue to pay the workers). This is shown in Eswar Prasad and Michael Keane, "Consumption and Income Inequality in Poland during the Economic Transition," IMF Working Paper no. 14 (1999). Also, it is important to bear in mind that official figures, which claimed that unemployment was low (or in the case of Turkmenistan, "zero"), were often false.

36. Douglass C. North, Institutions, Institutional Change and Economic Performance (New York: Cambridge University Press, 1990).

37. Christopher Hartwell, Institutional Barriers in the Transition to Market (Houndmills, UK: Palgrave MacMillan, 2013).

38. Stanley Fischer and Alan Gelb, "The Process of Socialist Economic Transformation," Journal of Economic Perspectives 5, no. 4 (1991): 91–101.

39. Gérard Roland, Transition in Historical Perspective, p. 252.

40. North, Institutions, Institutional Change and Economic Performance.

41. There is a purely mechanical question of how to measure the speed of institutional reforms. For a more thorough discussion, see Andrzej Rzońca and Piotr Ciżkowicz, "A Comment on the Relationship between Policies and Growth in Transition Countries," Economics of Transition 11, no. 4 (2003): 743–48.

42. Simeon Djankov and Peter Murrell, "Enterprise Restructuring in Transition: A Quantitative Survey," Journal of Economic Literature 40, no. 3 (2002): 739–92.

43. After Djankov and Murrell many other articles appeared, but withlittle modification of their tentative conclusions. See Simeon Djankov, "The Microeconomics of Post-Communist Transformation," in Åslund and Djankov, eds., The Great Rebirth.

44. This is based on the detailed analysis in chapter 4 of Havrylyshyn, Divergent Paths in Post-Communist Transformation.

45. A representative study of this position is Maxim Boycko, Andrei Shleifer, and Robert Vishny, Privatizing Russia (Cambridge, MA: MIT Press, 1995).

46. See, for example, Oleh Havrylyshyn, Divergent Paths in Post-Communist Transformation; Willem Buiter, "From Production to Accumulation," Economics of Transition 8, no. 3 (2000): 603–22; and Leonid Polishchuk and Alexei Savvateev, "Spontaneous (Non) Emergence of Property Rights," Economics of Transition 12, no. 1 (2004): 103–27.

47. See Mikheil Sakashvili and Kakha Bendukidze, "Georgia: The Most Radical Catch-up Reforms," in Aslund and Djankov, eds., The Great Rebirth.

48. Another unresolved debate, even if not central to the overall transition story, is that of Belarus's relatively good performance, despite its virtually unreformed economic system. One reason for ignoring the Belarusian example is that it is only one exception that counters evidence from 28 other countries. Another reason is to note that as "the last dictatorship in Europe," Belarus is hardly a desirable model of post-communist transformation. Moreover, many skeptics doubt the veracity of Belarusian statistics or suggest that much of the Belarusian success is thanks to huge subsidies from Russia. However, attempts to estimate a more realistic GDP or to measure the value of Russian subsidies are not enough to label Belarus as an economic failure. This paper has not attempted to resolve the Belarusian puzzle and leaves it for future research.

49. A brief history of the color revolutions is a cautionary tale. Once the oligarchic and bureaucratic vested interests are in place, a mere change of government does not ensure success. The failures of Ukraine's Orange Revolution and Kyrgyz's Tulip Revolution attest to the difficulty of sustaining reforms. In contrast, Georgia's Rose Revolution has met with success, albeit limited, and showed that reform is possible with enough forcefulness and resoluteness by both the street activists and a new, committed government.

50. Moldova's political establishment, while formally communist, has reacted to the population's desire to move closer toward the European Union. As such, the regime undertook reforms that went against some of the new vested interests.