Last week, the Business Roundtable joined the ever-present Donald J. Trump in creating unwanted regime uncertainty. President Trump displayed his mercantilist machismo by threatening to go to the mat with China and America’s businesses. He promised more tariffs on China if Beijing did not comply with his demands. Then, the President turned his fury on America’s businesses; he ordered them to stop doing business with the Chinese. But, that wasn’t all. Trump also lashed out at the Chairman of the U.S. Federal Reserve Jerome Powell, labeling him an “enemy” and comparing him to Trump’s trade nemesis President Xi Jinping of China. Not surprisingly, the markets plunged.

If that wasn’t enough, the Business Roundtable launched a major attack on property rights, the bedrock of the capitalist system. In a stunning new mission statement, the Roundtable, which represents almost 200 of America’s blue-chip companies, downgraded shareholders. According to the Roundtable, the purpose of a corporation will no longer be to conduct business with the sole objective of generating profits for shareholders. Owners of corporations (read: shareholders) will now just be one of five stakeholders, alongside customers, workers, suppliers, and communities that will call the tune for corporations.

Just what do President Trump and members of the Business Roundtable have in common? Well, they are all businessmen. And, when it comes to economics and economic policy, businessmen are notorious for talking nonsense. While businessmen readily accept the expertise of lawyers, engineers, and those from other professions, they often reject professional opinion offered by professional economists. And why not? After all, as they say, every man is an economist. So, when it comes to economics, businessmen have and express their own ideas and theories—often fallacious ideas and theories. That’s why solid training in economics is not simply to acquire a set of readymade answers to economic questions, but to learn how to avoid being deceived and bamboozled by businessmen.

When it comes to the Business Roundtable’s most recent manifesto, it appears that the authors simply suffer from a case of economic illiteracy, which is not uncommon in the business world. Indeed, the great Austrian economist Joseph Schumpeter concluded in his 1942 classicCapitalism, Socialism, and Democracythat businessmen would “never put up a fight under the flag of their own ideals and interest.” Schumpeter saw clearly that businessmen would not be the ones to defend capitalism. Indeed, he concluded that they, through their ignorance and cowardice, would assist those who wished to destroy capitalism. In 1947, when Schumpeter’sCan Capitalism Survive?was published, he took businessmen to the cleaners once again. He also continued to harbor gloomy prospects for capitalism’s survival.

And as for President Trump—as well as many businessmen, from Secretary of Commerce Wilbur Ross to those who man main street America—he has a view about international trade, particularly the U.S. trade balance. Their wrongheaded view of international trade and the trade balance has its roots in how individual businesses operate. A healthy business generates positive free cash flows—revenues exceed outlays. If a business cannot generate positive free cash flows on a sustained basis and cannot take on more debt or issue more equity to finance itself, then it will eventually be forced to declare bankruptcy.

Businessmen naturally employ this general free cash-flow template when they think about the economy and its external balance. For them, a negative trade balance for the nation is equivalent to a negative cash flow. In both cases, more cash is going out than is coming in.

But, this line of thinking is fallacious. Indeed, it represents a classic fallacy of composition. This fallacy is the belief that what is true of a part (a business) is true for the whole (the economy). Alas, economics is littered with fallacies. These cause businessmen to confuse their own arguments about international trade and trade balances, as well as other people’s minds, almost beyond reason.

In reality, the negative trade balance in the United States is not a “problem” caused by nefarious activities by foreigners. No. The U.S. negative trade balance, which the U.S. has recorded every year since 1975, is not a problem. Moreover, it is made in the U.S.A., caused by a savings deficiency (read: the U.S. fiscal deficit).

So, where did the Trump trade tirades and the Business Roundtable’s new anti-capitalist mission statement leave us? Well, it left us with plenty of unwanted regime uncertainty. Just what is regime uncertainty? Robert Higgs inTaking a Stand: Reflections on Life, Liberty, and the Economy(2015) answers this question. In 1997, Higgs first introduced the concept of “regime uncertainty” to explain the extraordinary duration of the Great Depression. Higgs’ regime uncertainty is, in short, uncertainty about the course of economic policy — the rules of the game concerning taxes and regulations, for example. These rules of the game affect the net benefits and free cash flows investors derive from their property; the rules affect the security of their property rights. So, when the degree of regime uncertainty increases, investors’ risk-adjusted discount rates increase, and their appetites for making investments diminish.

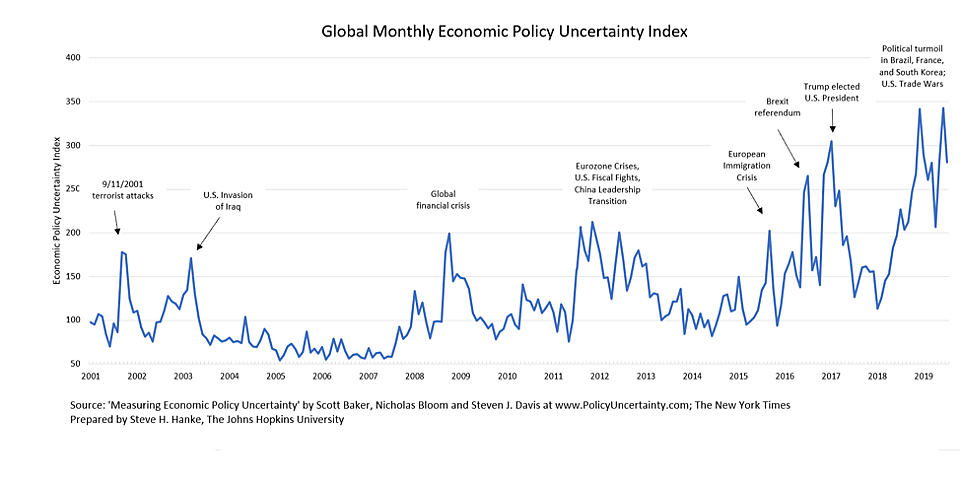

As it turns out, Scott R. Baker of Northwestern University, Nicholas Bloom of Stanford University and Steven J. Davis of the University of Chicago have developed a measure that serves as a proxy for regime uncertainty: the “Global Economic Policy Uncertainty Index.” The chart below shows the course of this index.

It’s clear that the Global Economic Policy Uncertainty Index is elevated. While the gold bugs love it, most others do not.

About the Author