The underlying rationale of joint-stock companies is that equity holders bear the largest proportional risk of an enterprise, and are rewarded with the most control over the firm and all of its upside risk. Equity owners are lowest in the debt hierarchy: their claims come after all other legitimate claimants of a defaulted enterprise. However, they are the highest in the hierarchy of control: in principle they select the directors of the enterprise who in turn select its management. This article argues that the rationale behind equity owner control should be extended in the debt and control hierarchies at least one more level. The unsecured debt of a firm should have a junior-most tranche, and control of the firm should devolve on the owners of that debt automatically and immediately upon the failure of the firm. Although the reorganization proposal described in this article would function effectively for any failing enterprise, this article considers the important and challenging problem of restructuring a failing systemically important financial institution (SIFI).

Legal Aspects of Existing and Proposed Legislation

Currently, there are two approaches to the reorganization of a SIFI in the United States—both mandated under the Dodd-Frank Wall Street Reform and Consumer Protection Act—and a proposed modification to these approaches in the Financial CHOICE Act of 2017, passed by the House of Representative in June 2017.1

Title I of the Dodd-Frank Act requires each systemically important bank to develop detailed plans—“living wills”—that specify procedures for its own resolution if it is about to collapse. The resolution strategies submitted to the Federal Reserve and the Federal Deposit Insurance Corporation (FDIC) to date rely primarily on either (1) a holding company that will spin off its subsidiaries while the holding company itself files for bankruptcy protection or (2) a “bridge bank” that will receive the high-quality assets of the failing firm and many of its liabilities, leaving most impaired assets and the remainder of its liabilities behind with the parent firm that enters bankruptcy. These two approaches are known jointly as the single-point-of-entry (SPOE) approach.2

The more complex banks, with numerous subsidiaries, will be structured with a bank holding company that would enter bankruptcy in the event of a failure. The resolution plans specify that subsidiaries should be well-capitalized, with sufficient liquid assets and with strong balance sheets, prior to a bankruptcy filing by the parent holding company. During bankruptcy proceedings the bank’s major subsidiaries would continue operations until they are sold off and the proceeds of the sales are returned to the estate of the bankrupt holding company. The second approach would be to form a bridge bank that would receive most of the high-quality assets of the failing bank and a portion of its liabilities. The impaired assets of a failing bank and the remainder of its liabilities would be left behind in the bankrupt firm. Both of these approaches are at odds with a fundamental precept of American bankruptcy law: similarly situated creditors should be treated similarly in the settlement of the bankrupt firm’s affairs.

Under the holding company structure, the creditors of the subsidiaries that are sold off will have claims on going concerns with positive net values, so their claims will unimpaired. On the other hand, the holding company will be bankrupt, and it will absorb all of the losses of the institution. Similarly, creditors of a bridge bank would have claims against a going concern, while the creditors whose claims are assigned to the parent firm will have claims against a bankrupt firm. The creditors of the bankrupt parent company, unlike the creditors of subsidiaries or a bridge bank, will be required to absorb all of the losses. Unequal treatment of similarly situated creditors is likely. The only way to avoid it would be to place all of the unsecured debt of the firm in the bankruptcy estate. Nothing in the Dodd-Frank Act requires or suggests that this will be done, and nothing would prevent the firm from distributing its unsecured debt to subsidiaries or a bridge company according to its own preferences. This opens the door to both unequal treatment of similarly situated creditors and to favoritism toward some creditors by the management of the firm in the lead-up to its collapse.

If the resolution process devised by the company in compliance with Title I, Section 165(d) of the Dodd-Frank Act is not implemented successfully and in a timely manner, Title II requires the FDIC to take control of the firm in receivership.3 Title II vests almost unlimited authority in a receiver appointed by the FDIC.4 Criticism has been leveled at the Dodd-Frank Act for its harshness5 and for its subversion of constitutionally guaranteed protections.6 Other legal arguments could be mounted against Dodd-Frank, such as those developed in Hamburger (2014) and in Lawson (2015), to address the expansive authority of administrative agencies. Hamburger (2014) argues that agencies frequently combine legislative functions in their rulemaking, executive functions in their oversight and enforcement, and judicial functions with their administrative law judges. One of Hamburger’s primary arguments is that agencies violate the separation of powers, remove legislative functions from elective bodies, and eliminate review by an independent judiciary. For example, Hamburger (2014: 257) argues that

administrative procedure … is justified on the ground that the courts are the real target of constitutional guarantees of due process and other procedural rights. It is not plausible, however, to suggest that administrative tribunals are less confined by procedural guarantees than the courts, or that administrative process satisfies the due process of law. Procedural rights developed … precisely to bar extralegal adjudication. And the growth of administrative adjudication only confirms the importance of procedural rights as limits on extralegal power. Rather than satisfy the due process of law, administrative process is exactly what the guarantee of due process forbids.

These arguments clearly have relevance to agency authority in Dodd-Frank, which is extensive and operates explicitly without even the administrative law review provided by other agencies, such as the SEC, the FDIC, the NLRB, the FAA, the EEOC, and dozens of other federal agencies. Recent cases, such as Bandimere v. SEC in the 10th Circuit Court of Appeals and Burgess v. FDIC in the 5th Circuit Court of Appeals, indicate a growing discomfort within the judiciary toward quasi-judicial review within an administrative agency of that agency’s own proceedings. Although the Bandimere and Burgess decisions are confined to the question of how administrative law judges are appointed, it would hardly seem to solve the problem of the irregularity of those proceedings by eliminating even agency review.

The legal arguments against Dodd-Frank are worth pursuing in their own right, but the argument put forth and emphasized in this article is that the procedures in Dodd-Frank’s Title II impose unnecessary administrative oversight and authority in the resolution of distressed financial firms: a simpler, less disruptive, more transparent market-oriented process can be implemented that defines and respects rights of the firms’ creditors.

The challenge of a reorganization regime for SIFIs is to balance the need to maintain their core functions without interfering with the goal of giving equal treatment to similarly situated creditors. Dodd-Frank’s Title II fails explicitly in that regard. For example, in Title II, Section 210(h)(1)(B): “Upon the creation of a bridge financial company . . . such bridge financial company may . . . assume such liabilities . . . as the Corporation may, in its discretion, determine to be appropriate.” This places the FDIC squarely in the role of partitioning creditors into one group that will experience no loss and another group that will bear all of the losses of the bankrupt firm.

Title I of the Dodd-Frank Act is no better: the management of the failing firm will determine the partition. The possibility of favoritism or even coercion and retribution is apparent. Creditors of a firm that demand payments due from a faltering bank could be asked to back off or even lend more to the failing bank. If the creditors refuse, the management of the failing firm could put all of the debts of that creditor into the bankruptcy estate rather than the bridge bank. The possibilities for manipulation open to a failing bank are limited only by the imagination of the management and board of directors. One of the purposes of bankruptcy is to explicitly close avenues for fraudulent conveyance. By avoiding bankruptcy proceedings, Title I opens endless avenues for mischief by desperate or even vengeful management of failing firms.

The CHOICE Act places the reorganization process back in the hands of bankruptcy courts, but it falls back on the same device of a bridge bank that continues as a going concern, and a parent bank that enters bankruptcy. The apparent motive of this legislation is to regularize the legal framework for SIFI reorganization. While the CHOICE Act restores the role of the courts, as with both Title I and Title II reorganization procedures, some creditors would be favored by becoming creditors of the bridge bank, and others would be in the unfortunate position of being creditors of the bankruptcy estate.

The proposal offered in this article, based on research conducted with Vernon Smith, would maintain the core functions of the firm through reorganization yet avoid the different treatment of similarly situated creditors by creating a class of creditors who know ex ante that they would be called upon to absorb losses.7 The challenge of the reorganization of a SIFI is that it must take place quickly—and for the stability of the financial system, core functions of the failing firms should be placed in a solvent entity that operates without interruption. That is the rationale for creating a bridge bank or assuring that major operations continue within key subsidiaries of the parent firm. That necessity implies that some creditors will absorb losses. Our proposal simultaneously assures the solvency of the firm by assigning losses to one predesignated tranche of creditors, but it compensates those creditors with ownership of the firm after reorganization. Notably, under both Dodd-Frank reorganization approaches, as well as under the CHOICE Act proposal, the creditors who absorb the losses are not compensated in any way for their loss, while control devolves onto parties selected by the management of the failing firm under Title I and it devolves onto the FDIC-appointed receivers under Title II.

After a brief review of the balance sheet consequences of an asset collapse, I provide a summary of reorganization bonds, which are a market-oriented alternative resolution process that respects the property rights of creditors, preserves as much of the value of a failing firm as possible, and minimizes disruption to credit markets, asset markets, and the economy.

Asset Collapse and Insolvency

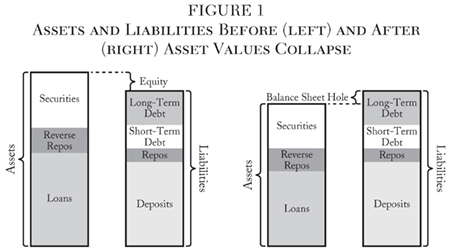

The left side of Figure 1 shows a stylized balance sheet with key asset and liability items for a bank with positive equity. The right side shows the same bank’s balance sheet if the value of its assets collapses—that is, the bank’s equity position disappears and the bank becomes insolvent. A bailout would add cash to the asset side of the balance sheet and more debt to the liability side of the balance sheet, leaving the balance sheet hole the same size. A bailed-out bank typically takes earnings from the healthy portion of its asset portfolio as they come in over the course of many years and moves them to loss reserves so that impaired assets can be removed from the books. During this long period the bank has suppressed earnings to dedicate to dividends, stock buybacks, or organic growth. One consequence of this is that the bank has difficulty finding capital investment, and it will typically deleverage as the only avenue available to it to raise its capital to asset ratio. A method is needed to remove some of the liabilities from the bank’s balance sheet. Bankruptcy does that, but at the cost of major disruption to the firm, to financial markets, and to the wider economy. Our proposal achieves the same goal with far less trauma.

Reorganization Bonds

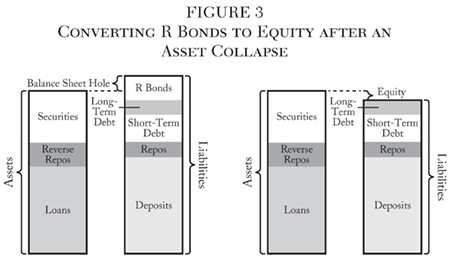

Gjerstad and Smith (2014) propose the creation of a class of bonds that sits between equity and all other creditors in the hierarchy of firm obligations. These bonds, which we called “reorganization bonds” (or “R bonds”), would be converted to equity immediately upon failure of a firm.8 I want to emphasize that R bonds differ in a crucial respect from contingent convertible bonds, because we propose that ownership and control of the corporation would pass to the bondholders with conversion of the bonds to equity. This is crucial because contingent convertible bonds simply provide the managers who have failed with a new pool of capital, and profits that the firm accrues after conversion would be shared by the owners of the contingent convertible bonds with incumbent shareholders.9 Under our proposal, if an asset value collapse causes a firm to run out of equity capital—that is, the firm becomes insolvent—the incumbent equity holders’ shares are eliminated, the R bonds are converted to equity, and the holders of the equity that was created by conversion of the R bonds become the sole owners of the firm.

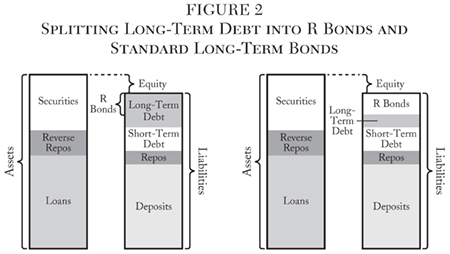

Figure 2 shows how R bonds are created from standard long-term debt. Figure 3 shows the effect of eliminating the claims of the original equity holders and converting the R bonds to a new equity pool. After the R bonds are converted, the board of directors selected by the bondholders’ committee and the new management team will take control of the bank. Contingent convertible bonds would reward mismanagement and failure with new capital; our proposal circumvents that incentive flaw.

With this structure, R bonds should trade at almost the same price as the bank’s standard corporate bonds when the likelihood of failure is near zero, so that a sound bank will face no additional cost of funding with this arrangement. If the bank does become insolvent, then prior equity holder claims are eliminated when R bonds convert to equity. If losses on assets are less than the sum of the precrisis book value of equity and the amount of R bonds, then the bank’s solvency is restored under our procedure and the reorganization will produce a new equity cushion owned exclusively by the investors whose R bonds were converted. With established criteria that trigger conversion, the ad hoc nature of bailouts, the public funds that support them, and their severe incentive distortions can all be eliminated.

Conversion of long-term bonds to equity is a key element of our proposal. We propose that, if equity capital is depleted and the bank is on the brink of default, 12 percent of the bank’s liabilities could be converted from debt into equity capital. Some of the R bond debt so converted will absorb the balance sheet hole that preceded the bank’s collapse, but if that hole is less than 12 percent of the bank’s liabilities, then the bank will have a positive equity capital position after conversion.

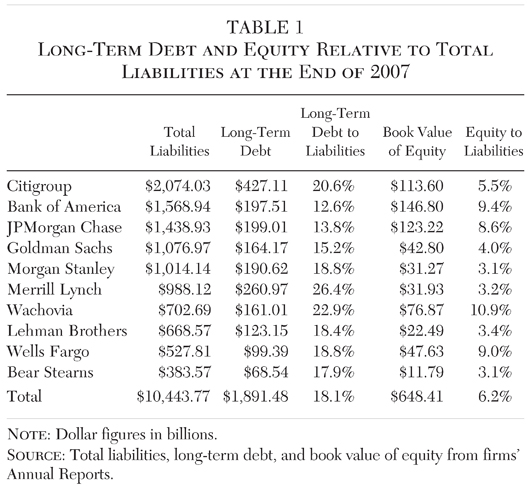

Table 1 shows the liabilities of the ten largest banks in the United States at the end of 2007; it also shows the amount of long-term debt that each one had outstanding. Each of these firms had between 12.6 percent and 26.4 percent of its liabilities in the form of long-term bonds, so that each would have been able to meet the threshold for R bond issuance without a substantial change to its financing costs.

At the end of 2007, the book value of equity capital at Bear Stearns, Lehman Brothers, Merrill Lynch, and Morgan Stanley had fallen to levels just above 3 percent of liabilities. (See Table 1, columns 4 and 5.) The Federal Reserve carried out a back-door bailout of Bear Stearns by lending $28.82 billion to Maiden Lane LLC to purchase impaired Bear Stearns assets in March 2008. Lehman Brothers failed in September 2008. Merrill Lynch was sold to Bank of America with loss guarantees on $118 billion of its assets from the Federal Reserve. All three of these firms had inadequate book value of equity capital by the end of 2007, and it is quite likely that the asset sides of their balance sheets were overstated due to overvalued mortgage securities on their books.10 By January 8, 2008, the market capitalization of Bear Stearns was only $8.4 billion, or about 2.2 percent of its liabilities. This is a threshold that clearly requires a contingency plan for reorganization. By July 14, 2008, Lehman Brothers’ market capitalization had fallen as low as $8.6 billion. With $613 billion in liabilities, equity capital had fallen to 1.4 percent of liabilities. On the same day, market capitalization of Washington Mutual fell to $5.5 billion, or 1.9 percent of its liabilities. With these firms in such dire condition, under our proposal bondholders’ committees would begin final preparations for a takeover.

Challenges for Resolution Plans and Orderly Liquidation

The Title I Resolution plans submitted to the Federal Reserve and the FDIC have a number of common features. Some of the banks have implemented a holding company structure. Others would utilize a bridge bank in the event of failure. When a holding company is utilized, it would commit substantial resources to its subsidiaries before it enters bankruptcy. The subsidiaries would continue as going concerns until they are sold and the proceeds are returned to the estate of the holding company. A bridge bank would operate similarly, but may be preferred for a firm that has few subsidiaries.

Despite the limitations of the Title I resolution procedures, assessments of the banks’ plans by the FDIC and the Federal Reserve Board have led to progress on several important problems. Resolution planning has required firms to better align their business operations with their material legal entities, insure that the constituent parts of the firm have access to financial market utilities (especially payment systems and trading and settlement operations), and the banks have implemented service agreements that would provide continued access to information technology support and other critical services to subsidiaries upon a breakup of the firm. Significant progress has also been made to extend the automatic stay in bankruptcies on contracts to include derivatives, futures, and swaps. This makes less likely a repeat of the severe losses precipitated by collateral seizures and sales that followed the Lehman bankruptcy. But the banks’ resolution plans depend almost entirely on the optimistic assumption that Global Systemically Important Financial Institutions (G-SIFIs) can resolve themselves and avoid disruption to the U. S. and global financial system by breaking themselves apart and selling the pieces—presumably to other G-SIFIs. Of course, financial distress is highly correlated, so many of the largest financial firms will be turning to one another to raise capital. Even if that were possible, the sale of Lehman Brothers investment banking and capital market accounts to Barclays in a Section 363 sale in September 2008 provides insight into the limited capital raised by such sales, and the potential for serious harm to the interests of the seller—in this case the Lehman Brothers estate. According to the Trustee of the estate, James Giddens, Lehman Brothers transferred assets worth approximately $11,869 million to Barclays. In addition, Barclays gained over 72,000 customer accounts with assets of $43,000 million (about $600,000 per account).11 Barclays in return paid $2,438 million on behalf of Lehman Brothers to third parties.

Title II of the Dodd-Frank Act would transfer control over a faltering financial institution to the FDIC as the receiver, charged with liquidation of the firms’ assets and payment of claims against the firm. The draconian elements of Title II are well-known,12 but Title II is also set up to wreak economic havoc, since it relies solely on sales of major business lines and liquidation of the firm. The Lehman Brothers liquidation had catastrophic results for the firms’ creditors. In the case of Lehman Brothers, senior bondholders received their first payment in April 2012, three and a half years after the bankruptcy filing. Unsecured creditors received their first distribution in September 2014, six years after the bankruptcy filing.13 Fleming and Sarkur (2014) found that, as of March 27, 2014, allowed claims to creditors stood at $303.6 billion dollars. With its Thirteenth Plan Distribution to Senior Note-holders on October 5, 2017, Wilmington Trust reached a payout of approximately 42.7 percent to senior bondholders.14 Unsecured creditors have had a comparable payout percentage. Since the estate resolution is nearly complete, losses should end up at approximately 57 percent of the $303.6 billion in allowed claims, or a loss of approximately $173 billion to Lehman Brothers creditors. The time frame for payments to creditors, the scale of the losses, and the ex ante lack of clarity regarding how losses would be allocated to creditors could be disastrous for financial markets in future liquidations as they were with Lehman Brothers.

Conclusion

In this article, I have described a procedure that is capable of addressing the principle challenge of reorganizing failing financial institutions: maintaining the core intermediation and payment functions of the firm, avoiding a fire sale of its assets to cover liabilities, and allocating losses in a manner that is transparent and understood by a firm’s creditors ex ante. Many of the challenges facing resolution regimes are obviated by our procedure. The firm remains as a going concern, maintaining both the core functions of the firm and all contractual obligations other than its long-term debt obligations to the holders of the reorganization bonds (which are replaced with equity). Concerns that have been raised by the FDIC regarding availability of debtor-in-possession financing are avoided, as are the incentives of foreign regulators and governments to ring-fence the assets of subsidiaries in their jurisdiction. Other concerns with resolution and liquidation regimes are also mitigated. Calabria (2015) points out that “the Treasury . . . may have felt that allowing a default on GSE debt would be viewed internationally as the equivalent of a default by the U.S. government.” Concerns of this sort may lead regulators and politicians to ignore the law altogether and proceed with a bailout, as they did with the resolution procedures for Fannie Mae and Freddie Mac in 2008, or it may lead to pressures to include some favored creditors of a failing bank in the debts of the bridge bank and less fortunate or less favored creditors in the bankruptcy. The ambiguous status of creditors under both the Title I resolution plans and the Title II liquidation procedures leaves either of these possibilities open. Our procedure, by specifying particular long-term debt for conversion, lessens the pressure for a bailout and eliminates the possibility of favored treatment by government receivers for particular creditors of a failing financial institution.

The procedures could be developed in a new Chapter 14 of the bankruptcy code or in modifications to Chapter 11 for systemically important financial institutions. A great deal of work has been done to plan for the contingency that an important financial firm must enter bankruptcy or be liquidated. It would be good though to avoid those paths with a process that maintains all of the functions of a major financial institution without interruption, and prepositions liabilities that can be dedicated to recapitalize a failing financial firm in a manner that is known ex ante to regulators, to the firm’s creditors, and to other market participants.

References

Calabria, M. (2015) “The Resolution of Systemically Important Financial Institutions: Lessons from Fannie and Freddie.” Cato Working Paper No. 25 (January 13). Available at https://object.cato.org/sites/cato.org/files/pubs/pdf/working-paper-25_1.pdf.

Fleming, M. J., and Sarkur, A. (2014) “The Failure Resolution of Lehman Brothers.” Federal Reserve Bank of New York Economic Policy Review (December): 175–205.

Gjerstad, S., and Smith, V. L. (2014) “Bonds, Not Bailouts, for Too Big to Fail Banks.” Wall Street Journal (August 12).

Hamburger, P. (2014) Is Administrative Law Unlawful? Chicago: University of Chicago Press.

Hughes Hubbard & Reed (2016) “State of the Estate” (August 16). In re Lehman Brothers Inc., Case No. 08–01420 (SCC) SIPA.

Lawson, G. (2015) “The Return of the King: The Unsavory Origins of Administrative Law.” Texas Law Review 93 (6): 1521–45.

Lee, P. L. (2015) “Bankruptcy Alternatives to Title II of the Dodd-Frank Act–Part I.” Banking Law Journal (October): 437–87.

McDermott, M. A. (2010) “Analysis of the Orderly Liquidation Authority, Title II of the Dodd-Frank Wall Street Reform and Consumer Protection Act.” Available at www.skadden.com/sites/default/files/publications/FSR_A_Analysis_Orderly_Liquidation_Authority.pdf.

McDermott, M. A., and Turetsky, D. M. (2011) “Restructuring Large, Systemically-Important, Financial Companies: An Analysis of the Orderly Liquidation Authority: Title II of the Dodd-Frank Wall Street Reform and Consumer Protection Act.” American Bankruptcy Institute Law Review 19 (2): 401–51.

Merrill, T. W., and Merrill, M. L. (2014) “Dodd-Frank Orderly Liquidation Authority: Too Big for the Constitution?” University of Pennsylvania Law Review 164: 165–247.

1Throughout this article, the Dodd-Frank Wall Street Reform and Consumer Protection Act will be referred to as the “Dodd-Frank Act” (see www.gpo.gov/fdsys/pkg/BILLS-111hr4173enr/pdf/BILLS-111hr4173enr.pdf). The Financial CHOICE Act of 2017 will be referred to as the “CHOICE Act.” The parts of the CHOICE Act that repeal and replace Title II of the Dodd-Frank Act are Title I, Subtitle A (repeal) and Title I, Subtitle B (replace). See https://financialservices.house.gov/uploadedfiles/hr_10_the_financial_choice_act.pdf.

2See Title I, Section 165 (d) of the Dodd-Frank Act and the public submissions by banks and the responses from the Federal Reserve and the FDIC at www.federalreserve.gov/bankinforeg/resolution-plans.htm. See Lee (2015) for analysis of the banks’ resolution plans, especially pp. 464–86, which describe the adoption of the holding company and bridge bank approaches.

3Even the FDIC has sought to avoid the path of liquidation, with most of its efforts directed toward review and assessment of the banks’ Title I resolution plans. See Lee (2015: 476–78) for discussion of the pivot by the FDIC from Title II liquidation toward Title I resolution planning.

4McDermott and Turetsky (2011: 412) describe the extent of the receiver’s control. “Once the FDIC is appointed receiver of a covered financial company, it assumes virtually complete control over the company and the receivership process. The perfunctory role of the courts in the core receivership process ends, and there are limited avenues for challenging the various ancillary decisions that the FDIC may make in pursuing the liquidation.”

5McDermott and Turetsky (2011: 404) argue that “the provisions of the Act and the powers delegated to the FDIC and other government authorities may be draconian when implemented. The right to decide whether to initiate receivership proceedings is vested in government authorities, not in financial companies’ boards, management, or stakeholders, and is subject only to very limited judicial review that is highly deferential to such authorities.”

6Merrill and Merrill (2014) argue that Dodd-Frank Title II violates the due process clause in the Fifth Amendment and subverts judicial review in Article III of the Constitution, among other issues.

7For a summary of our proposal, see Gjerstad and Smith (2014).

8By a failure, I mean events like those that precipitated government interventions on behalf of Bear Stearns between March 14 and March 16, 2008, the collapse of Lehman Brothers six months later, and the intervention on behalf of AIG on September 16, 2008.

9Many authors suggest that these bonds could convert to equity if the market capitalization of the firms passes below some threshold, such as 2 percent of the firm’s liabilities. When the threshold is crossed, some amount of the bonds would be converted to equity at the market price of equity shares when the threshold was passed. There are at least three significant problems with this approach. One issue is that if the equity price crosses the threshold on its way lower, bond conversion bails out the incumbent shareholders before their shares lose more or all of their value. The second consideration is that these procedures also leave the incumbent management and board in control of the firm. A third problem is that, with the management and board in control of the firm, the new equity holders have minimal protection against the incumbent management and board enriching themselves at the expense of the new equity holders before the new equity holders can wage a fight for control of the firm. For all of these reasons I argue that it would be better to allow the firm to enter a prepackaged bankruptcy where the bondholders are rewarded with control of the firm.

10Washington Mutual provides a good example of this. In its 10-Q filing on June 30, 2008, Washington Mutual had book value of equity capital of $26.09 billion (about 9.2 percent of its liabilities), but at that time the market value of its equity capital was only $8.24 billion (about 2.9 percent of equity capital). A closer examination of its balance sheet reveals an extraordinary level of exposure to residential real estate, with $230.2 billion in real estate loans and $19.2 billion in mortgage-backed securities. Real estate lending amounted to 79 percent of assets.

11See the “State of the Estate,” pp. 24–25, August 16, 2016, from Hughes Hubbard & Reed (the law firm of the trustee).

12McDermott (2010: 2), in an analysis from Skadden, Arps, Slate, Meagher & Flom LLP argues that “the potential harshness of the Act ultimately may mean that its most salutary effect will be to minimize the circumstances under which it will, in fact, be used.” Lee (2015: 453) points out,“Various critics of Title II maintained that . . . Title II would be a non-transparent process and would not be administered according to a clear set of rules and settled precedents in sharp contrast to the Bankruptcy Code. These critics maintained that the [Senate] changes did not alter the fact that the federal government would be choosing which entities to resolve under Title II and which creditors to protect.”

13See Hughes Hubbard & Reed (2016: 27).

14See Wilmington Trust notices to senior noteholders (www.wilmingtontrust.com/lehman/notices.html).

About the Author

Steven Gjerstad is a Presidential Fellow at Chapman University’s Economic Science Institute.