A streamlined mandate from Congress, instructing the Federal Reserve to focus on stabilizing inflation around its self-declared 2 percent target, would provide the strongest foundation for effective monetary policymaking by satisfying both these requirements. An inflation-targeting mandate would help preserve, de jure, the increased independence won by the Federal Reserve, de facto, only after the United States economy suffered through a damaging phase of high inflation and high unemployment during the 1970s. Without such a mandate, the Fed’s independence—already under attack—may erode still further as memories of that historical episode continue to fade.

The same inflation-targeting mandate would make the Federal Reserve more accountable, by specifying a quantitative goal for monetary policy against which the central bank can and should be judged. The new mandate could be reinforced by further legislation, requiring the Fed to make its policy decisions with reference to preannounced rules, not only for targeting interest rates during normal times but also for conducting large-scale asset purchases during severe deflationary recessions. These rules would help protect the Fed against political pressures to allocate credit and engage in inflationary public finance.

Securing Independence

Article I, Section 8 of the United States Constitution gives to Congress the power to “coin money” and “regulate the value thereof.” Modern economic theory provides a rationale for this. In general equilibrium, utility-maximizing households and profit-maximizing firms care only about relative prices. Thus, market-clearing conditions for goods and services work only to pin down those relative prices. An actor from outside the system is needed to solve the coordination problem that determines the aggregate nominal price level. Consistent with its constitutional powers, Congress gives the Federal Reserve monopoly rights over the issuance of base money (currency plus bank reserves). By exercising its monopoly control over the monetary base, the Federal Reserve regulates on behalf of Congress the value of money or, equivalently, its reciprocal: the nominal price level. Congress retains the right to set the Fed’s mandate, specifying the goals it wishes monetary policy to achieve. In this way, Congress ensures that the Fed remains accountable to the American people.

Congress has also put in place a number of institutional features—including 14-year terms for Federal Reserve Board Governors and a decentralized structure consisting of the 12 Federal Reserve Banks in addition to the Board itself—that potentially allow Fed officials to take a longer-run view. Much of post–World War II monetary history, however, suggests that these features, by themselves, have been insufficiently strong. This history points to a lack of independence, rather than an absence of accountability, as the bigger practical obstacle to effective monetary policymaking.

The historical problem is illustrated best by an example presented by Finn Kydland and Edward Prescott (1977) in their article, “Rules Rather than Discretion: The Inconsistency of Optimal Plans.” This paper formed an important part of the work for which the two economists were awarded the Nobel Prize in 2004.

In Kydland and Prescott’s example, a central banker operating under discretion—making optimal choices period-by-period based on prevailing economic conditions—is always tempted to generate surprise inflation to lower the rate of unemployment. Agents in the private sector, however, correctly anticipate that the central bank will succumb to this temptation, and rationally build their expectations of inflation into price and wage-setting decisions. In equilibrium under discretion, therefore, inflation is suboptimally high, but unemployment is no lower than it would otherwise be.

If, on the other hand, the central banker in Kydland and Prescott’s example is insulated from short-run political pressures, and thereby allowed to adopt and adhere to an intermediate-term policy rule that is fixed independently of current economic conditions, he or she will successfully eschew the temptation to exploit the expectational Phillips curve and aim to keep inflation low instead. Quite strikingly, by striving to do less, the central bank accomplishes more: it succeeds, at least, in creating and maintaining an environment of stable prices, leaving unemployment to fluctuate, as it would anyway, in response to ever-evolving conditions in the labor markets.

Kydland and Prescott’s model is not just an intellectual curiosity, for it successfully explains why, despite the occasional appearance of a statistical Phillips curve relationship between inflation and unemployment in the United States data, the Federal Reserve’s efforts to exploit that Phillips curve led, during the 1970s, not to lower unemployment at the cost of higher inflation but instead to the worst of both worlds: higher unemployment and higher inflation (i.e., stagflation). In fact, Barro and Gordon (1983) later used essentially the same model as the foundation for what they called “A Positive Theory of Monetary Policy,” meaning a theory that accounts for the historical facts.

Also quite strikingly, both the discretionary and committed central bankers in the Kydland-Prescott model share the same preferences as society as a whole. The model’s success at explaining stagflation during the 1970s, therefore, points not to a lack of accountability but instead to a lack of independence as the main flaw in the design of monetary policymaking arrangements during those years. Indeed, a major theme running through the second volume of Allan Meltzer’s authoritative History of the Federal Reserve is how William McChesney Martin and Arthur Burns were consistently pressured by Presidents Johnson and Nixon to adopt and maintain policies that were systematically too accommodative, fueling inflation’s rise. Meltzer (2009a: 676) quotes Burns on this point:

Viewed in the abstract, the Federal Reserve System had the power to abort the inflation at its incipient stage fifteen years ago [1964] or at any later point, and it has the power to end it today [1979]. At any time within that period, it could have restricted the money supply … to terminate inflation with little delay. It did not do so because the Federal Reserve was itself caught up in the philosophical and political currents that were transforming American life and culture.

Finally recognizing that high inflation had become a major economic and political problem, President Carter appointed Paul Volcker, known for his willingness to pursue anti-inflationary policies, as Fed chairman in August 1979, after William Miller’s brief term as Burns’ initial successor. Even then, however, congressional and presidential pressures on the Fed continued, as Meltzer (2009b: 1049–50) explains:

Prodded by the congressional Democrats, labor unions, and others, on March 14 [1980], the president [Carter] addressed the public on television … and he told the Federal Reserve to impose credit controls on borrowing.… The Federal Reserve opposed but did not resist.… The Board’s vote was five to one to adopt controls. Most of the members disliked the proposal, but only Henry Wallich voted no.

Only after credit controls failed, economically and politically, and were finally lifted in June 1982, was the Volcker Fed left free to fight inflation using the only method that has ever been shown to work: by reducing the growth rate of money. Meltzer (2009b: 1128) concludes:

The anti-inflation program became possible because President Reagan and, with the exception of credit controls, President Carter, did not interfere. Leading members of Congress supported the policy, and those affected most—the homebuilders—reluctantly accepted the importance of reducing inflation.

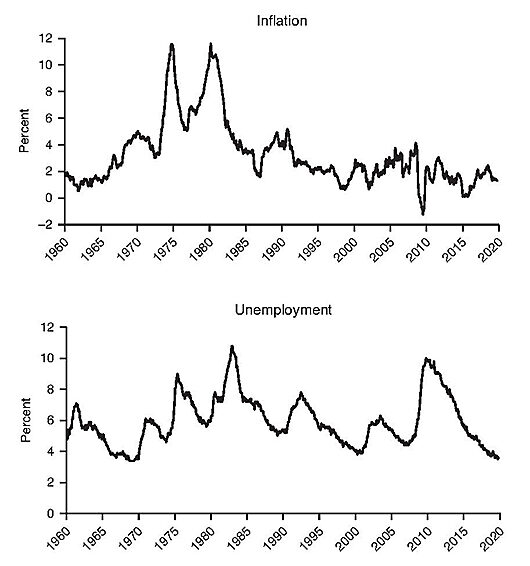

Subsequent presidents and members of Congress generally followed suit and refrained from commenting on or criticizing publicly specific policy actions taken by the Fed under Alan Greenspan. The fact that low inflation during the Greenspan years was accompanied by low unemployment speaks, once again, to the usefulness of the Kydland-Prescott model and, more generally, to the important role played by central bank independence. By focusing first on keeping inflation low, a more independent Fed also creates an environment of monetary stability within which the free market works best to create economic opportunities for all Americans. In contrast to graphs that struggle to show the statistical Phillips curve, the two panels of Figure 1 reveal much more easily the choices that are available to designers of monetary policymaking institutions. Inflation can be low or high; it can be stable or volatile. Unemployment fluctuates no matter what, but keeping inflation low and stable can promote the Fed’s full employment objective.

FIGURE 1: INFLATION AND UNEMPLOYMENT IN THE UNITED STATES

NOTES: The top panel plots year-over-year percentage changes in the price index for personal consumption expenditures; the bottom panel plots the civilian unemployment rate. Both monthly series run from January 1960 through October 2019.

SOURCE: Federal Reserve Bank of St. Louis FRED database.

Successful institutional arrangements for monetary policymaking must resolve the tension that can arise between central bank independence and accountability. Because monetary policy actions that appear to promise short-run benefits can often impose even larger long-run costs, outcomes that are preferable to everyone can be achieved by insulating the central bank from day-to-day economic and political pressures. At the same time, however, an independent central bank’s objectives should stay aligned with those of society at large.

Establishing Accountability

Very much to its credit, the Federal Reserve, especially under Greenspan’s successors, Ben Bernanke, Janet Yellen, and Jerome Powell, has taken a series of important steps to make the monetary policymaking process more transparent. These actions, summarized by the Federal Reserve Bank of Philadelphia’s “Timeline to Transparency,”1 help ensure that the central bank, despite its enhanced independence, remains accountable to Congress and, by extension, the American public.

Starting in 2000, the Federal Open Market Committee (FOMC) began releasing after each of its meetings a policy statement, explaining the rationale for its policy actions and providing a brief assessment of its outlook for the balance of risks going forward. Since 2007, the Summary of Economic Projections has added even more detail, by collecting numerical forecasts for inflation, unemployment, and output growth as well as intermediate and longer-term projections for the federal funds rate target made by each governor and reserve bank president. Press conferences led by the chair have been held after every other FOMC meeting since 2011; beginning in 2019, these press conferences have followed every meeting.

Most important of all, however, in 2012, the FOMC began releasing an annual “Statement on Longer-Run Goals and Monetary Policy Strategy.” With it, the Fed accepted direct responsibility for controlling inflation in the long run. The January 2019 statement indicates specifically that:

The inflation rate over the longer run is primarily determined by monetary policy, and hence the Committee has the ability to specify a longer-run goal for inflation. The Committee reaffirms its judgment that inflation at the rate of 2 percent, as measured by the annual change in the price index for personal consumption expenditures, is most consistent over the longer run with the Federal Reserve’s statutory mandate [FOMC 2019].

The FOMC could not be any clearer on how it wishes to be held accountable. So long as the preferred measure of inflation, based on year-over-year changes in the PCE (personal consumption expenditure) price index, remains close to the 2 percent target, the Fed should be congratulated for doing its job well. But if inflation deviates persistently in either direction from that target, members of Congress should ask Federal Reserve officials to explain why.

The FOMC’s strategy statement also explicitly recognizes that, as suggested by Kydland and Prescott’s model and as confirmed by the data shown in Figure 1, unemployment, though it may be influenced by monetary policy in the short run, lies well beyond the Fed’s ability to control over longer horizons:

The maximum level of employment is largely determined by nonmonetary factors that affect the structure and dynamics of the labor market. These factors may change over time and may not be directly measurable. Consequently, it would not be appropriate to specify a fixed goal for employment [ibid.].

Thus, despite its current statutory dual mandate, prescribed by the Federal Reserve Reform Act of 1977, to pursue both “stable prices” and “maximum employment,” the Fed acknowledges that it cannot take credit or accept blame for fluctuations in the rate of unemployment as it surely can in the case of inflation. Congress should stop pretending that it can do so.

Finally, the FOMC’s strategy statement emphasizes, again as suggested by the Kydland-Prescott model and as confirmed by the data, that any appearance of a statistical Phillips curve relationship between inflation and unemployment in the data does not translate into a tradeoff between those two variables that can be exploited systematically by monetary policy. To the contrary, the best way the Fed can promote low unemployment is to aim for stable inflation first:

In setting monetary policy, the Committee seeks to mitigate deviations of inflation from its longer-run goal and deviations of employment from the Committee’s assessments of its maximum level. These objectives are generally complementary [ibid.].

Constrained in its language by the statutory dual mandate, this is about as close as the FOMC can get to asking Congress for a more streamlined, and sensible, single mandate to target inflation.

Renewed Challenges

Could the Federal Reserve continue to conduct monetary policy successfully, with reference only to its own Statement on Longer-Run Goals and without a new mandate from Congress? Perhaps. But renewed challenges confront the Fed today, threatening to erode the de facto independence gained under Volcker and Greenspan and thereby enhancing the value of more formal, legislative support.

During the 1990s, as Fed policymaking improved even under the dual mandate, many economists questioned the continued relevance of the Kydland-Prescott model. After returning to academia following his term as vice chairman of the Federal Reserve Board, for instance, Alan Blinder (1997: 13) wrote:

Starting with Kydland and Prescott’s (1977) seminal paper, many theorists have fretted over the following time-inconsistency problem that allegedly bedevils monetary policy. Because the Phillips curve embodies a tradeoff between unemployment and unanticipated inflation, well-meaning central bankers are constantly tempted to reach for short-term employment gains by engineering inflation surprises.… Let me begin with a nonconfession: during my brief career as a central banker, I never once witnessed nor experienced this temptation.

Blinder (1997: 14) went on to suggest that, in practice, monetary policymakers not only understand the time-inconsistency problem but can solve it on their own:

I can assure you that my central banker friends would not be surprised to learn that academic theories that assume that they seek to push unemployment below the natural rate then deduce that monetary policy will be too inflationary. They would doubtless reply, “Of course. That’s why we don’t do it.”

Similarly, McCallum (1995: 208–9) argues:

All that is needed for avoidance of the inflationary bias … is for the central bank to recognize the futility of continually exploiting expectations that are given … and to recognize that its objectives would be more fully achieved on average if it were to abstain from attempts to exploit these temporarily given expectations.

Later, however, McCallum (1997: 100) clarified his earlier argument in a very important way, by emphasizing that his critique applies only to an “independent” central bank. Independence remains the key. Frederic Mishkin (2000: 2), like Blinder a distinguished academic with experience on the Federal Reserve Board, elaborates further:

[E]ven if central bankers recognize the problem, there still will be pressures on the central bank to pursue overly expansionary monetary policy by politicians. Thus, overly expansionary monetary policy and inflation may result, so that the time-inconsistency problem remains. The time-inconsistency problem is just shifted back one step; its source is not in the central bank, but rather, resides in the political process.

Current and future Federal Reserve officials may continue to guard successfully against giving in to their own temptation to stimulate the economy through inflation. But their resolve will be tested more severely if—like William McChesney Martin and Arthur Burns from the past—they face overwhelming pressures from the American political system.

These pressures have already started to build. As memories of 1970s stagflation have faded and frustration over subpar economic performance following the financial crisis and Great Recession of 2007–2009 grown, politics have returned to the monetary policy arena. The chair’s semi-annual delivery of Monetary Policy Reports has become a recurring opportunity for members of Congress to publicly air their dissatisfactions with the Fed. The confirmation process for nominees to the Federal Reserve Board has grown more contentious. And speculation has even arisen as to whether the president can replace the Federal Reserve chair over differences of opinion on appropriate monetary policy strategies and actions.

Meltzer (2005: 172) summarizes the dilemma concisely, noting that “The Federal Reserve was better able to control inflation when the President was named Eisenhower or Reagan instead of Johnson, Carter, or Nixon.”

A new mandate that clarifies the Fed’s role in stabilizing inflation would serve as an institutional safeguard, independent of the personalities of future presidents, members of Congress, and Federal Reserve Board chairs, against a return to the poor practices of the 1970s. It would help all policymakers, both inside and outside the Fed, resist their own temptations to argue for higher inflation. It would help solve the time-inconsistency problem that applies at all levels of government.

Indeed, the risks associated with eroding de facto Federal Reserve independence may loom even larger today that they did during the 1960s and 1970s. The added risks stem from the Fed’s ability, secured during the financial crisis in 2008, to pay interest on bank reserves. In theory, Tolley (1957) and Friedman (1960) first proposed paying interest on reserves, as a way of removing incentives for banks to economize inefficiently on their holdings of reserves. In practice, however, Plosser (2018) and Ireland (2019a) argue that the Fed used its ability to pay interest on reserves to support policies that directed credit to specific sectors of the economy during and after the financial crisis. By using interest on reserves in this way, the Fed ceased to act like a central bank, responsible for using its role as supplier of base money to stabilize the aggregate nominal price level. Instead, the Fed began acting more like a nationalized commercial bank, issuing short-term liabilities in the form of reserves and using the proceeds to acquire securities backed by mortgage loans.

The additional problem is that nothing prevents Congress from exploiting the Fed’s new power for its own ends, by pressuring the Fed to channel credit to support politically favored projects, public or private. And nothing prevents Congress from using the profits generated from the Fed’s risky intermediation activity to fund specific fiscal initiatives. In fact, Congress has already done so twice: once with the Fixing America’s Surface Transportation Act of 2015 and again with the Bipartisan Budget Act of 2018.

Previous legislative efforts, both the Fed Oversight Reform and Modernization Act of 2015 and the Financial Choice Act of 2017, asked that the Fed announce an interest rate rule, similar to the one proposed by Taylor (1993), to guide the setting of its federal funds rate target. With the additional risks associated with the Fed’s ability to pay interest on reserves and thereby support an extremely large balance sheet in mind, future legislation should go further, and ask the Fed to identify a similar rule for quantitative easing. This rule, similar in spirit to a Taylor rule, would allow the Federal Reserve to specify in advance how the size and duration of future large-scale asset purchase programs would depend on a limited number of variables, like inflation and unemployment, relating directly to its monetary policy stabilization objectives during a severe economic downturn. This provision would incorporate into Federal Reserve strategy the proposition, emphasized by Hess and Orphanides (2018), Ireland (2019b), and Orphanides (2019) that in both good times and in bad, monetary policy works best when guided by simple, preannounced rules. More importantly, however, it would protect the Fed from political pressures to use its balance sheet to support fiscal initiatives.

Concluaion

Since 1980, the Federal Reserve has made good use of its enhanced independence by keeping inflation in the United States low and stable. Under Volcker, Greenspan, Bernanke, Yellen, and Powell, the Fed has also unilaterally adopted practices and procedures that have made its policy actions easier to anticipate, understand, and evaluate.

The focus should now shift back to Congress, to finally dismiss its discredited dreams of an exploitable Phillips curve, left over from the late 1960s and 1970s, and to respect, instead, the lessons learned from economic theory and history since then. A streamlined statutory mandate that accepts the Fed’s self-imposed 2 percent inflation target as the principal goal for monetary policy would both secure the central bank’s independence and bolster its accountability.

The current dual mandate, by contrast, works mainly to the political benefit of Congress and the president. Drawing on research by Kane (1980, 1988) and Woolley (1984), Hetzel (1986) describes how the vagueness and incoherence of their previous legislative instructions to the Fed allow members of Congress to influence monetary policy decisions for the short-run benefit of their key constituents even as they retain the ability to blame the Fed for the longer-run costs those same decisions impose on the economy. Whatever the motivating force may be, however, backsliding to the ways of the 1970s, by pressuring Federal Reserve officials to exploit an illusory Phillips curve will lead again, as it did before, to both higher inflation and higher unemployment. By contrast, a congressional commitment that leaves the Fed free to pursue price stability first will not only guarantee that the era of low inflation enjoyed since the 1980s will continue, but will also help recreate the backdrop of monetary stability that allowed the private economy, throughout the 1990s, to create robust growth in incomes and jobs.

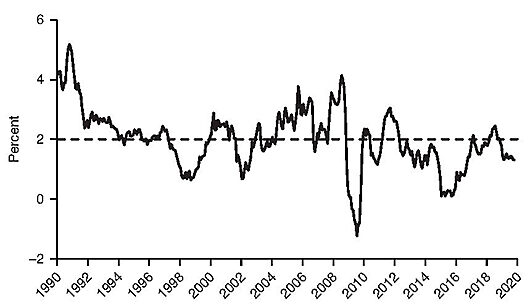

In addition, by accepting the Fed’s 2 percent inflation target as its own, Congress can establish a benchmark against which the Fed can be judged more fairly. Figure 2 reveals that, through most of the period since 2010, the Fed’s preferred measure of inflation has run modestly, but persistently, below the 2 percent target. In response, perhaps the FOMC only needs to clarify its objectives, acknowledging that there are limits on its ability to control month-to-month or even year-to-year fluctuations in measured inflation. It could do so by placing bounds above and below its current target to identify a range within which measured inflation may fluctuate.

FIGURE 2: INFLATION COMPARED TO THE FED’S 2 PERCENT TARGET

NOTES: The solid line shows the behavior of the actual U.S. inflation rate, as measured by year-over-year percentage changes in the price index for personal consumption expenditures. The dashed line marks the 2 percent target identified in the Federal Open Market Committee’s “Statement on Longer-Run Goals and Monetary Policy Strategy.” Monthly inflation data run from January 1990 through October 2019.

SOURCE: Federal Reserve Bank of St. Louis FRED database.

On the other hand, the persistent undershoot of inflation below target could reflect more fundamental problems with the workings of the Fed’s postcrisis policy implementation framework. Ireland’s (2019a, 2019b) analysis shows, for example, that paying interest on bank reserves interferes with the Fed’s ability to deliver monetary accommodation in the face of deflationary shocks. It does so by increasing the demand for reserves instead of the supply of reserves, perversely reinforcing rather than offsetting the effects of those impulses on the aggregate price level.

Could the Fed hit its inflation target more reliably without interest on reserves? This is the kind of question that more focused debate and discussion, organized around the Fed’s success or failure to achieve a streamlined, single mandate, can help answer. Inflation targeting, the key to success in the past, remains the key to success in the future.

References

Barro, R. J., and Gordon, D. B. (1983) “A Positive Theory of Monetary Policy in a Natural Rate Model.” Journal of Political Economy 91 (August): 589–610.

Blinder, A. S. (1997) “Distinguished Lecture on Economics in Government: What Central Bankers Could Learn from Academics—and Vice Versa.” Journal of Economic Perspectives 11 (Spring): 3–19.

Federal Open Market Committee [FOMC] (2019) “Statement on Longer-Run Goals and Monetary Policy Strategy.” Available at www.federalreserve.gov/monetarypolicy/files/FOMC_LongerRunGoals.pdf.

Friedman, M. (1960) A Program for Monetary Stability. New York: Fordham University Press.

Hess, G. D., and Orphanides, A. (2018) “Monetary Policy Normalization Should Be More Systematic and Less Wobbly.” Position Paper. New York: Shadow Open Market Committee (March 9).

Hetzel, R. L. (1986) “A Congressional Mandate for Monetary Policy.” Cato Journal 5 (Winter): 797–820.

Ireland, P. N. (2019a) “Interest on Reserves: History and Rationale, Complications and Risks.” Cato Journal 39 (Spring/Summer): 327–37.

___________ (2019b) “Monetary Policy Implementation: Making Better and More Consistent Use of the Federal Reserve’s Balance Sheet.” Journal of Applied Corporate Finance 31 (Fall): 68–76.

Kane, E. J. (1980) “Politics and Fed Policymaking: The More Things Change, the More They Remain the Same.” Journal of Monetary Economics 6 (April): 199–211.

___________ (1988) “Fedbashing and the Role of Monetary Arrangements in Managing Political Stress.” In T. D. Willett (ed.), Political Business Cycles: The Political Economy of Money, Inflation, and Unemployment, 479–89. Durham, N. C.: Duke University Press.

Kydland, F. E., and Prescott, E. C. (1977) “Rules Rather than Discretion: The Inconsistency of Optimal Plans.” Journal of Political Economy 85 (1977): 473–92.

McCallum, B. T. (1995) “Two Fallacies Concerning Central-Bank Independence. American Economic Review 85 (May): 207–11.

___________ (1997) “Crucial Issues Concerning Central Bank Independence.” Journal of Monetary Economics 39 (June): 99–112.

Meltzer, A. H. (2005) “Origins of the Great Inflation.” Federal Reserve Bank of St. Louis Review 87 (March/April): 145–75.

___________ (2009a) A History of the Federal Reserve: Volume 2, Book 1, 1951–1969. Chicago: University of Chicago Press.

___________ (2009b) A History of the Federal Reserve: Volume 2, Book 2, 1970–1986. Chicago: University of Chicago Press.

Mishkin, F. S. (2000) “What Should Central Banks Do?” Federal Reserve Bank of St. Louis Review 82 (November/December): 1–13.

Orphanides, A. (2019) “Monetary Policy Strategy and its Communication.” Paper presented at the Federal Reserve Bank of Kansas City Economic Policy Symposium, Challenges for Monetary Policy, Jackson Hole, August 23. Available at www.kansascityfed.org/~/media/files/publicat/sympos/2019/20190819orphanides.pdf.

Plosser, C. I. (2018) “The Risks of a Fed Balance Sheet Unconstrained by Monetary Policy.” In M. D. Bordo, J. H. Cochrane, and A. Seru (eds.), The Structural Foundations of Monetary Policy, 1–16. Stanford, Calif.: Hoover Institution Press.

Taylor, J. B. (1993) “Discretion versus Policy Rules in Practice.” Carnegie-Rochester Conference Series of Public Policy 39 (December): 195–214.

Tolley, G. S. (1957) “Providing for Growth of the Money Supply.” Journal of Political Economy 65 (December): 465–85.

Woolley, J. T. (1984) Monetary Politics: The Federal Reserve and the Politics of Monetary Policy. New York: Cambridge University Press.

About the Author

Peter N. Ireland is the Murray and Monti Professor of Economics at Boston College and a Member of the Shadow Open Market Committee.

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.