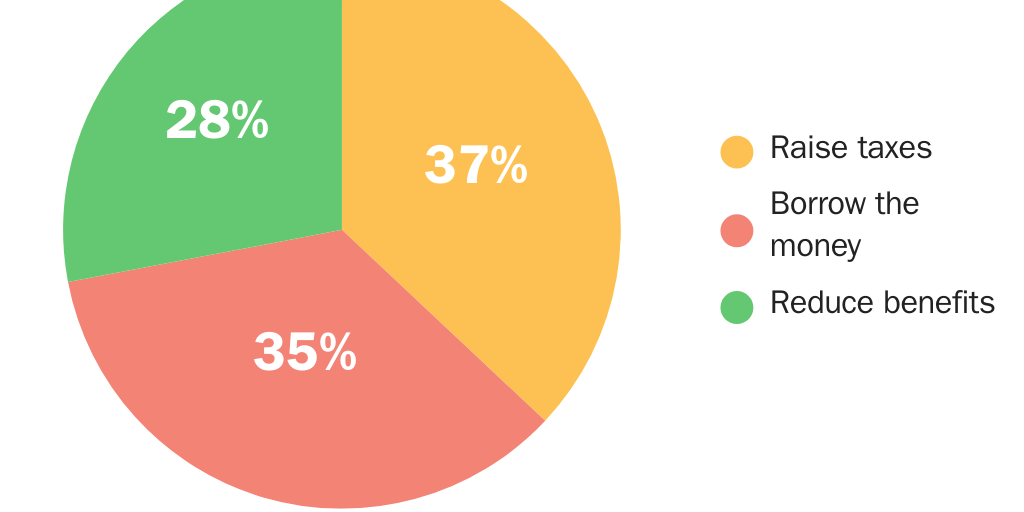

The newly released Social Security Trustees’ annual report shows that the Social Security Trust Fund’s finances have deteriorated further. The trust fund is now projected to be depleted sooner than previously expected, meaning Congress will face an even larger financing gap. Closing that gap will require larger tax increases, deeper benefit cuts, or some combination of both.

Recent polling on Social Security from the Cato Institute in collaboration with YouGov offers some clues about how Americans are likely to respond to this news.

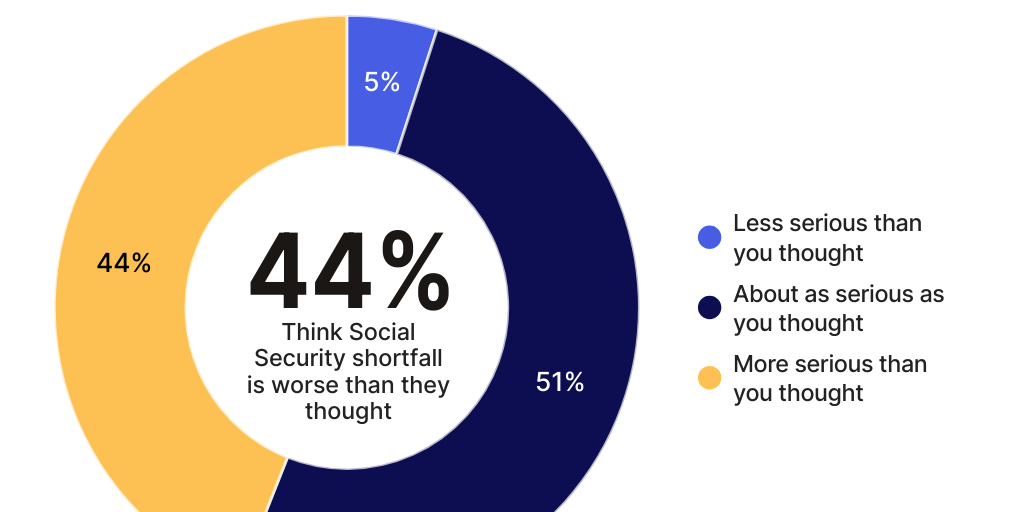

Americans are aware that Social Security is underfunded, but many do not understand the severity of the problem. For instance, 7 in 10 workers expect to experience some sort of Social Security benefit cut. However, when told that the Social Security budget shortfall would require benefit cuts of nearly 23 percent starting in the early 2030s, close to half (44 percent) conceded the situation was more serious than they previously thought. And the true share may be even higher, since some respondents may be reluctant to admit they did not already understand the problem. These results suggest many Americans will be surprised to learn that the trust fund is now projected to be depleted even sooner than expected.

Without Americans understanding Social Security’s dire fiscal situation, polls show they are highly resistant to meaningful reforms to close the shortfall. For instance, 77 percent oppose reducing Social Security benefits for current and future retirees, and 67 percent oppose reducing Social Security benefits for only future retirees.

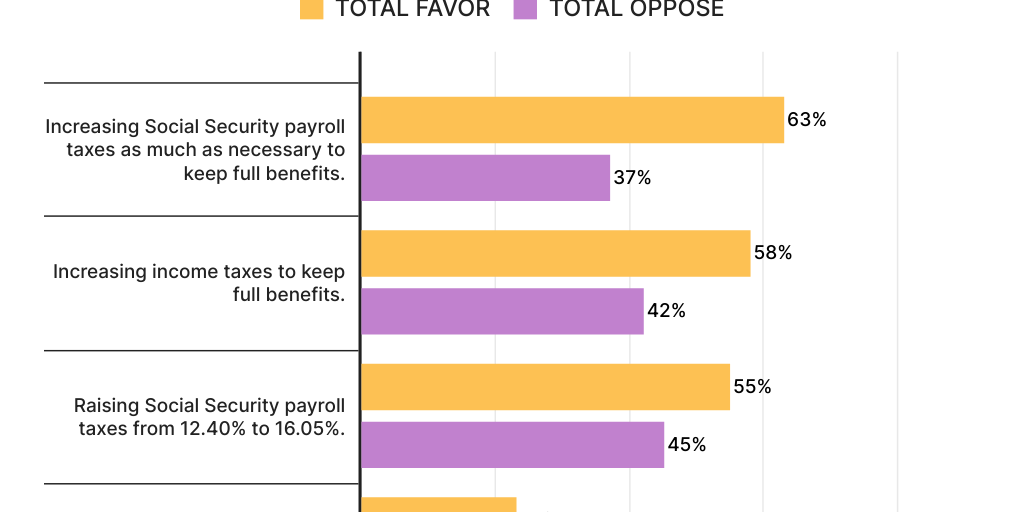

At first glance, most say they would support increasing taxes to avoid benefit cuts for seniors. For example, majorities at first said they favor raising income taxes (58 percent) or payroll taxes “as much as necessary” (63 percent) to keep full benefits for retirees.

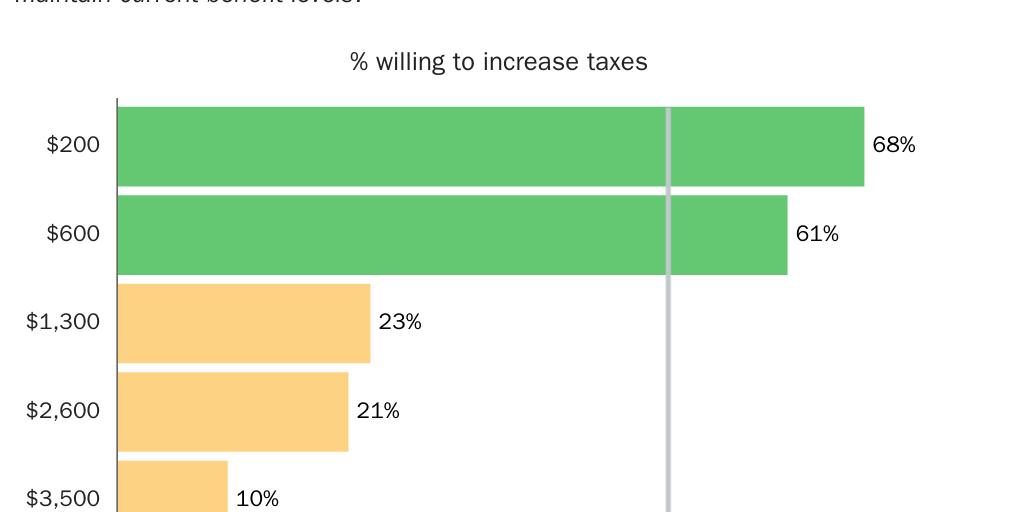

Yet attitudes shift dramatically when discussing tax increases in concrete dollars and cents. More than three-fourths—77 percent—would oppose raising their own taxes even $1,300 per year, which is below what would be necessary for the average person to close the budget shortfall.

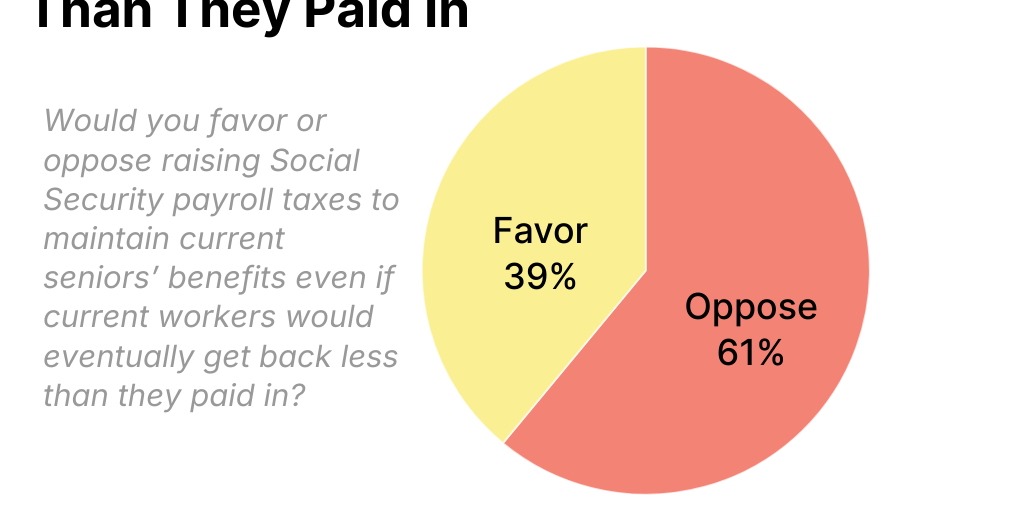

Americans are also reluctant to raise taxes if doing so means current workers would not eventually get back what they paid into the system. Sixty-one percent (61 percent) would oppose raising taxes to maintain current seniors’ benefits if current workers would ultimately receive less than they paid in. Because Social Security is a pay-as-you-go system, higher taxes on current workers do not guarantee their own future benefits; instead, those taxes help finance benefits for current seniors.

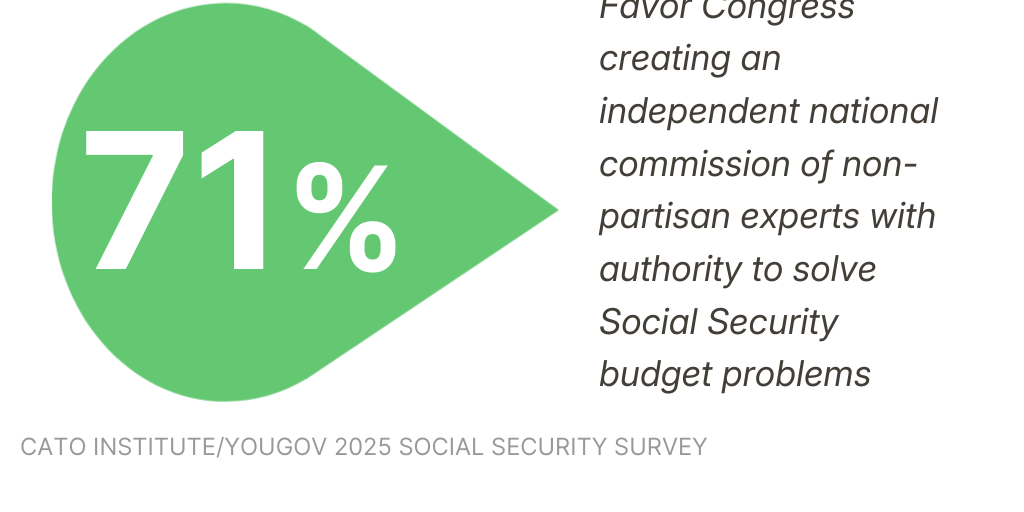

The strongest public opening for breaking this political deadlock is an independent commission. Seventy-one percent (71 percent) of Americans favor Congress creating an independent National Commission composed of nonpartisan experts on Social Security reform and giving them the authority to solve Social Security’s budget problems.

The public also supports several smaller changes that could improve Social Security’s finances, even if they would not actually solve the problem. For instance, 58 percent favor raising Social Security benefits at a slower rate in the future, and 57 percent would support holding benefits level for one year without any raise in benefits to build up funds, and 61 percent favor cutting benefits for higher earners to protect benefits for lower-income seniors.

Personal Accounts

The Cato Institute survey found broad initial support (60 percent) for allowing younger workers to invest some of their Social Security taxes into personal investment accounts.

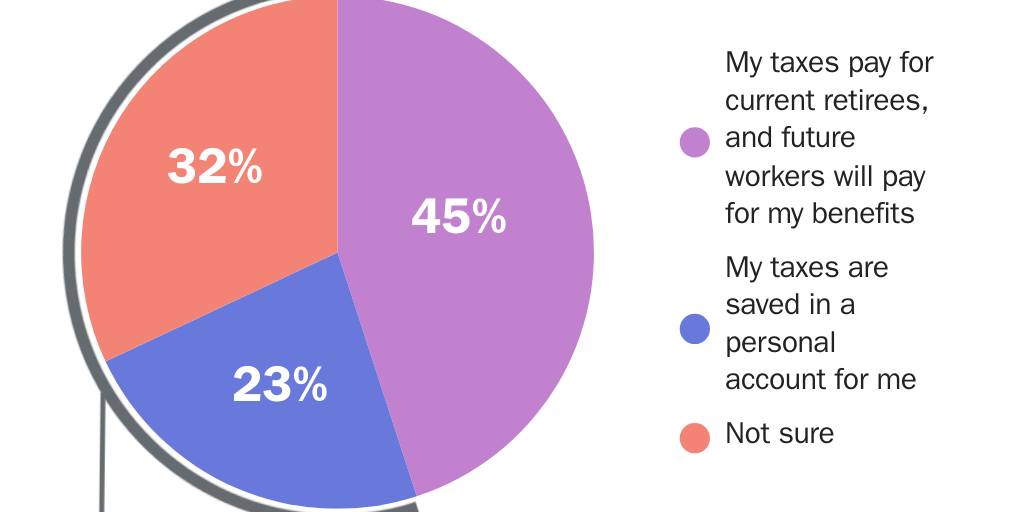

But much of that support appears to depend on not fully recognizing Social Security’s pay-as-you-go structure. Social Security did not begin as a system in which each generation paid for its own benefits. The earliest beneficiaries paid little or nothing into the program compared with the benefits they received, creating a permanent financing obligation that later workers have been asked to cover ever since. That is why current workers’ payroll taxes fund current retirees, rather than being saved for workers’ own future benefits.

As a result, allowing younger workers to opt out would leave fewer payroll tax dollars available to pay benefits for today’s seniors. Once respondents learn that allowing younger workers to opt out would require larger benefit cuts for current seniors, 69 percent oppose the proposal.

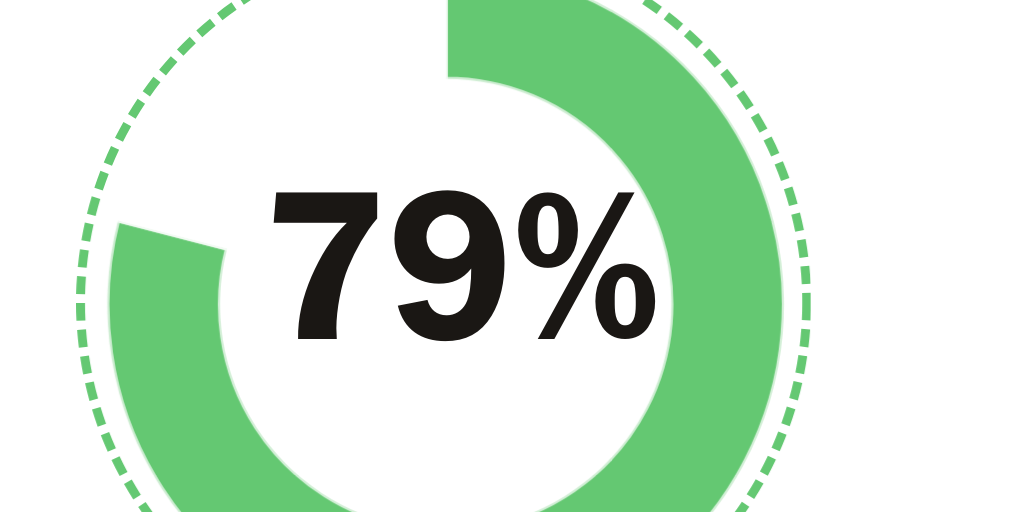

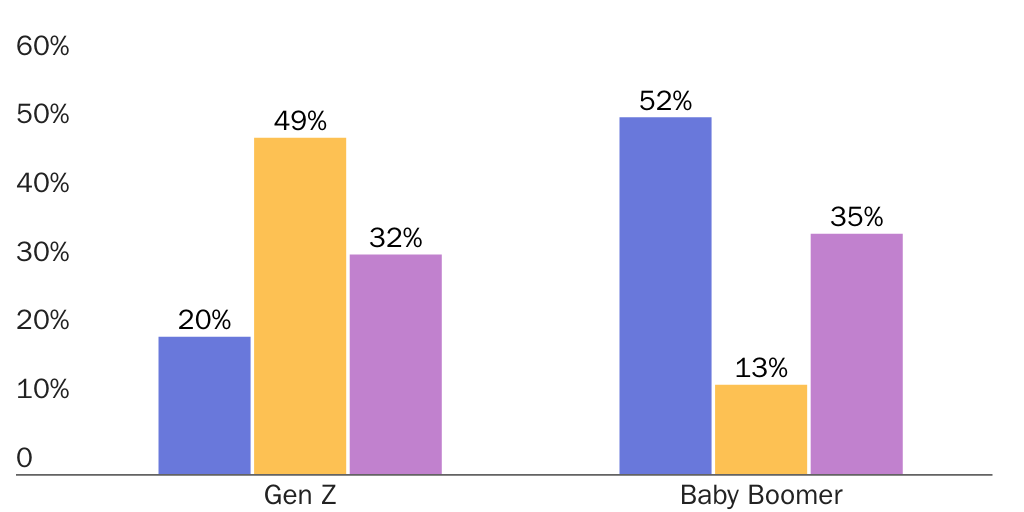

Members of Gen Z are the notable exception. Americans under 30 are the only age cohort in which a majority (55 percent) support allowing younger workers to opt out of Social Security even if doing so means benefit cuts for current seniors. This may be due to a plurality (48 percent) of younger respondents believing they get a worse deal than today’s retirees, or 79 percent who are expecting some sort of cut to their own future Social Security benefits.

Generational Conflict

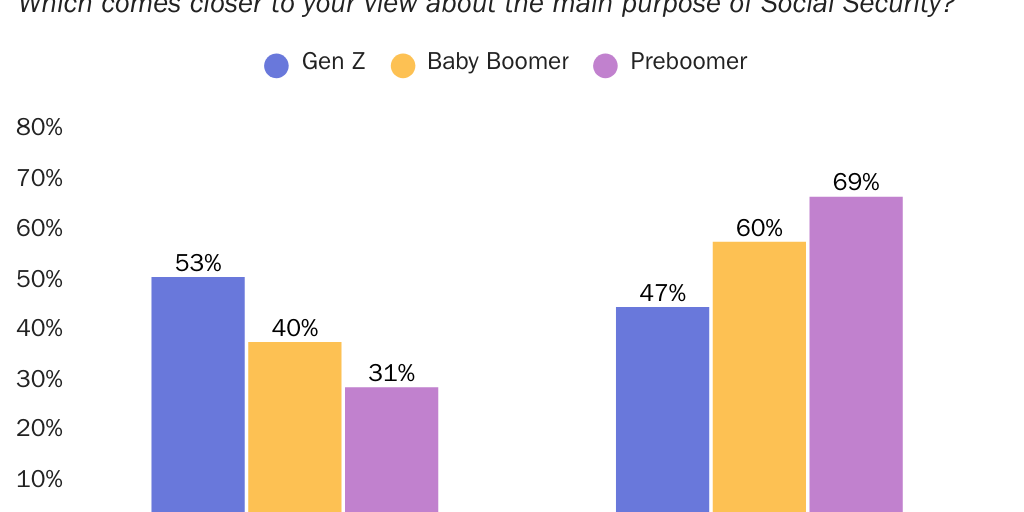

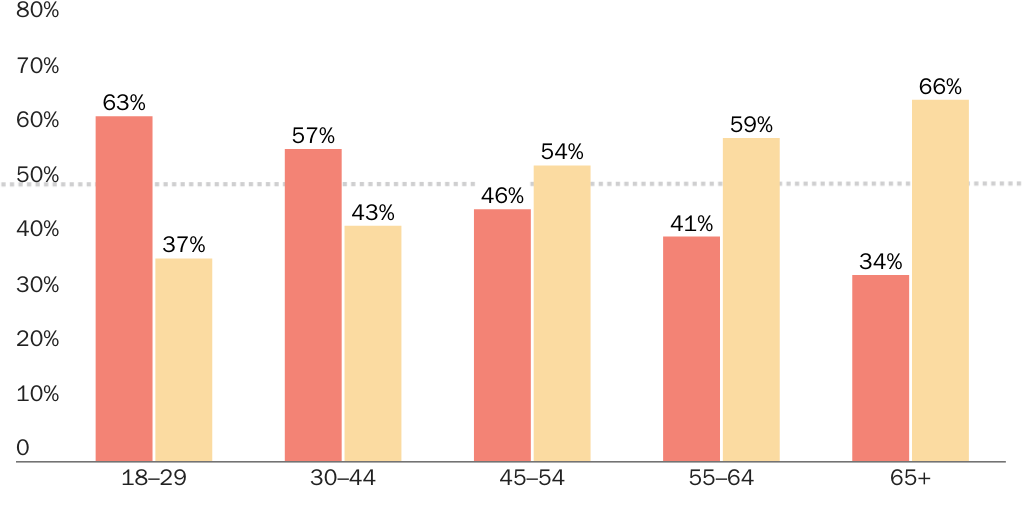

When Americans are confronted with the generational conflict inherent in Social Security’s pay-as-you-go structure, younger Americans are more open to reform. Overall, 69 percent of Americans say “Social Security benefits should be protected for current retirees, even if that means higher taxes on younger workers,” while 31 percent say “younger workers should be protected from higher taxes, even if that means reducing benefits for current retirees.”

Gen Z Americans are the only age cohort that rejects higher taxes to maintain seniors’ current benefit levels. Instead, a majority, 53 percent, say current retirees should accept benefit cuts to protect younger workers from tax hikes.

Implications

The message from the Trustees’ report and the Cato survey points to the same conclusion: Social Security’s fiscal problems are serious, but the political problem may be even harder. The program’s financing gap is growing, yet Americans remain resistant to reforms necessary to close it. Americans know something is wrong, but many do not yet understand the scale of the trade-offs. Until they do, Congress will continue to face strong public resistance to serious reform.

Full topline results and methodology for the December Cato Institute 2025 Social Security National Survey can be found HERE and crosstabs found HERE. The full report can be found HERE.

![Copy: Figure 2 [print]: Boccia_Nachkebia_Reimagining SocSec](https://infogram-thumbs-1024.s3-eu-west-1.amazonaws.com/7f16ba42-95e8-4626-943f-35aaab8f9e19.jpg)