The $7 trillion federal budget includes 2,623 benefit and subsidy programs, according to a newly updated federal website. Most budget discussions focus on the huge size of federal spending, but the Federal Program Inventory (FPI) website also reveals the government’s vast scope. Did you know, for example, that the Department of Commerce will hand out $195 million this year in something called State Digital Equity Planning and Capacity Grants?

Demian Brady and other analysts have pushed for the creation of such an inventory for years, and the White House budget office has delivered with the FPI. The public can use it to drill down and find spending amounts and descriptions for each program within each federal agency. With appropriations spending currently in front of Congress, members should be using the website to find programs to cut.

The FPI is based on “assistance listings,” which have been around in hard copy since the 1960s. Assistance basically means federal handouts. The listings include benefit payments, grants, loans, and subsidies to state and local governments, individuals, businesses, and nonprofit groups. Everything from Social Security benefits to farm subsidies is included. But the listings do not include federal contracting payments or programs that involve solely in-house federal activities.

In this post, I showed that the number of federal handout programs increased from 1,019 in 1970 to 1,425 in 2000 to 2,418 by 2023. The FPI count of 2,623 is higher because it includes 174 tax expenditure programs.

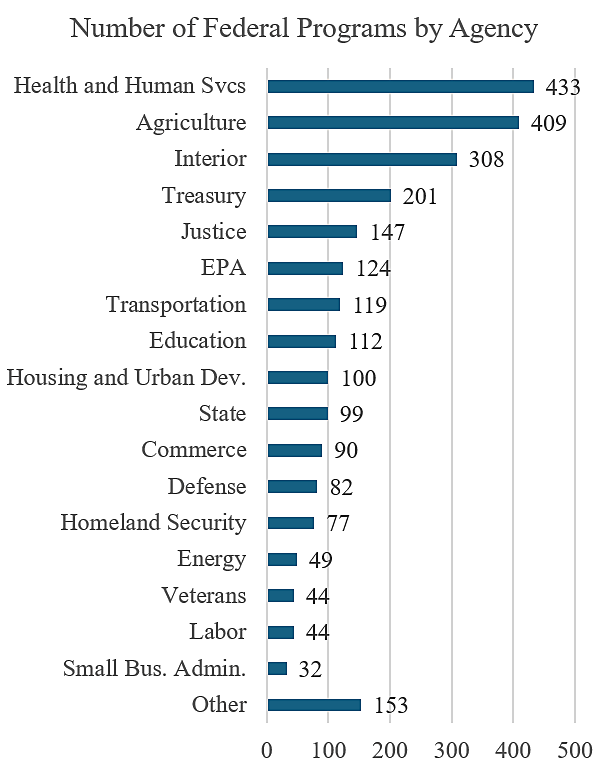

The chart shows the number of programs by department and major agency. The Department of Health and Human Services runs not only Medicare and Medicaid but also an armada of welfare programs. The Department of Agriculture runs not only farm subsidy programs but also rural subsidy programs and food subsidy programs, such as food stamps and school lunches.

With today’s massive budget deficits, Congress should downsize every department and agency. The main priority is to slash the big entitlement programs. But policymakers should also use the FPI to find hundreds more obscure and low-value programs to eliminate.

Beyond the budget savings, eliminating hundreds of smaller programs would reduce wasteful regulations, paperwork, and bureaucracy that smother the economy. The community development programs that I profiled last week are good examples of such waste.

Milton Friedman said, “The tragedy is that because government is doing so many things it ought not to be doing, it performs the functions it ought to be performing badly.” The government is like a restaurant with so many items on its menu that most are prepared badly. The government’s 2,623 programs are mainly unappetizing, and most should be slashed from the menu.

![Table 1 [print]: Emergency spending reform bills introduced in Congress](https://infogram-thumbs-1024.s3-eu-west-1.amazonaws.com/372281aa-785e-47f5-8d09-98f190e06003.jpg)